|

市場調査レポート

商品コード

1684723

列車通信ゲートウェイシステムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Train Communication Gateways System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 列車通信ゲートウェイシステムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年01月17日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

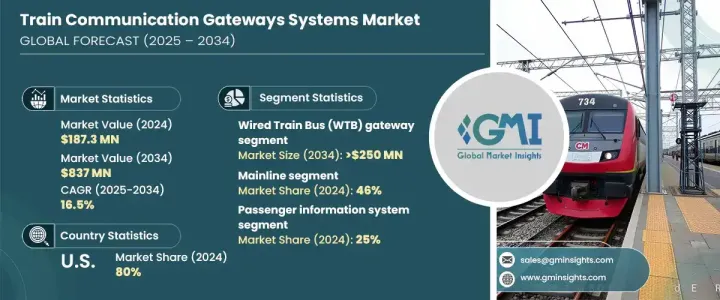

世界の列車通信ゲートウェイシステム市場は、2024年に1億8,730万米ドルと評価され、2025~2034年にかけてCAGR 16.5%で大きく成長すると予測されています。

より効率的で快適な移動手段に対する需要の高まりが、各国政府による鉄道インフラへの大規模な投資を促進しています。列車通信ゲートウェイシステムなどの最新技術の採用が進むにつれ、輸送効率の向上、安全性の改善、列車と管制センター間のより良い通信の促進が目標となっています。このようなシームレスな統合の必要性は、スムーズな運行を維持し、遅延を最小限に抑え、性能を最適化するためにリアルタイムのデータ交換に大きく依存する都市鉄道システムや高速鉄道の人気が高まるにつれて高まっています。技術主導の鉄道ネットワークが加速していることも、現代の交通システムの複雑で高速な要求に対応できる先進的通信ソリューションに対する需要の高まりにつながっています。

列車通信システムは、さまざまな種類の鉄道システムを効果的に管理する上で極めて重要です。これらのシステムは、列車、信号装置、制御センター間の継続的な通信を可能にし、安全でタイムリーな運行を保証します。この市場は、より高速で信頼性の高いデータ転送を可能にする技術の進歩が大きな原動力となっています。貨物輸送と旅客輸送の両方で効率化の必要性が高まっているため、最先端の通信ソリューションに対する需要が高まっています。さらに、鉄道部門では二酸化炭素排出量の削減とエネルギー効率の向上への関心が高まっており、電化された列車ネットワークをサポートする通信システムの急速な拡大に寄与しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 1億8,730万米ドル |

| 予測金額 | 8億3,700万米ドル |

| CAGR | 16.5% |

市場は、WTB(有線鉄道バス)ゲートウェイ、MVB(多機能車両バス)ゲートウェイ、ECN(イーサネット通信ネットワーク)ゲートウェイなど、オファリングに基づいてセグメント化されます。2024年には、WTBゲートウェイは市場シェアの40%を占め、2034年までに2億5,000万米ドルの売上が見込まれています。WTBゲートウェイは、列車と制御センター間の信頼性の高い継続的な通信を確保する上で重要であり、都市鉄道や高速鉄道システムで重要な役割を果たしています。堅牢な設計、低遅延、高接続性は、WTBゲートウェイが選ばれる主要理由です。リアルタイムモニタリングを提供し、列車の性能を最適化し、より良いスケジューリング、安全性、運行管理に貢献します。

列車タイプに関しては、市場は幹線、都市、貨物システムに分類されます。2024年には、都市と周辺地域を結ぶ幹線列車が市場シェアの46%を占めました。これらの列車は長距離輸送や貨物輸送に不可欠であり、安全性、定時性、運行効率を確保するために信頼性の高い通信システムが必要とされます。旅客・貨物両方の需要が増加していることから、シームレスな運行にはリアルタイム通信が不可欠な長距離高速鉄道の運行には、堅牢な通信システムが不可欠です。

米国では、列車通信ゲートウェイシステム市場が2024年の世界シェアの80%を占めています。米国の鉄道産業が二酸化炭素排出量の削減と効率向上のために電化へと移行するにつれ、先進的通信システムへの需要が急増しています。列車通信ゲートウェイは、新しい電力システムと既存の列車ネットワーク間の効果的な通信を可能にし、すべてのコンポーネントのシームレスな統合を保証します。この統合は、米国の鉄道インフラにおける革新的な鉄道技術の継続的開発にとって不可欠です。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推定の主要動向

- 予測モデル

- 一次調査と検証

- 一次情報

- データマイニングソース

- 市場スコープと定義

第2章 エグゼクティブサマリー

第3章 産業洞察

- エコシステム分析

- コンポーネントプロバイダー

- サービスプロバイダー

- メーカー

- 技術プロバイダー

- エンドユーザー

- サプライヤーの状況

- 利益率分析

- 技術革新の状況

- 特許分析

- 主要ニュース&イニシアチブ

- 規制状況

- 使用事例

- 影響要因

- 促進要因

- 安全性と運行効率に対する需要の高まり

- スマート鉄道の採用

- 鉄道インフラへの政府投資

- 通信システムの技術進歩

- 産業の潜在的リスク・課題

- 高い導入コスト

- レガシーシステムとの統合課題

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推定・予測:オファリング別、2021~2034年

- 主要動向

- WTBゲートウェイ

- MVBゲートウェイ

- ECNゲートウェイ

第6章 市場推定・予測:プロトコル別、2021~2034年

- 主要動向

- TCP/IP

- IEC 61375

- Profinet

- その他

第7章 市場推定・予測:用途別、2021~2034年

- 主要動向

- 旅客情報システム

- セキュリティモニタリングシステム

- 列車制御システム

- データ転送・通信システム

- その他

第8章 市場推定・予測:列車別、2021~2034年

- 主要動向

- 幹線

- 都市

- 貨物

第9章 市場推定・予測:地域別、2021~2034年

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Advantech

- Alstom

- AMiT Transportation

- Belden

- Duagon

- EKE-Electronics

- ELTEC Elektronik

- Ericsson

- GE

- HaslerRail

- HollySys

- Ingeteam

- Moxa

- Quester Tangent

- Rockwell

- SYS TEC Electronic

- TTTech

- UniControls

The Global Train Communication Gateways System Market was valued at USD 187.3 million in 2024 and is expected to grow significantly at a CAGR of 16.5% from 2025 to 2034. The rising demand for more efficient and comfortable travel options is driving substantial investments by governments in rail infrastructure. With the growing adoption of modern technologies, such as train communication gateway systems, the goal is to enhance transportation efficiency, improve safety, and facilitate better communication between trains and control centers. This need for seamless integration is amplified by the increasing popularity of urban rail systems and high-speed trains, which depend heavily on real-time data exchange to maintain smooth operations, minimize delays, and optimize performance. The acceleration of technology-driven rail networks is also contributing to the rising demand for sophisticated communication solutions that can accommodate the complex, high-speed demands of contemporary transit systems.

Train communication systems are crucial for the effective management of various types of rail systems. These systems allow for continuous communication between trains, signaling equipment, and control centers, ensuring safe and timely operations. This market is largely driven by advancements in technology that allow faster, more reliable data transfer. The increasing need for efficiency in both freight and passenger transportation is creating a greater demand for state-of-the-art communication solutions. Additionally, there is a rising focus on reducing carbon emissions and boosting energy efficiency within the rail sector, contributing to the rapid expansion of communication systems that support electrified train networks.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $187.3 Million |

| Forecast Value | $837 Million |

| CAGR | 16.5% |

The market is segmented based on offerings, including WTB (wired train bus) gateways, MVB (multifunction vehicle bus) gateways, and ECN (Ethernet communication network) gateways. In 2024, WTB gateways represented 40% of the market share and are expected to generate USD 250 million by 2034. WTB gateways are critical in ensuring reliable and continuous communication between trains and control centers, playing a vital role in urban and high-speed rail systems. Their robust design, low latency, and high connectivity are key benefits that make them a preferred choice. They provide real-time monitoring, optimize train performance, and contribute to better scheduling, safety, and operational management, driving their adoption across global rail networks.

When it comes to train types, the market is categorized into mainline, urban, and freight systems. In 2024, mainline trains, which connect cities and surrounding areas, accounted for 46% of the market share. These trains are essential for long-distance and freight transportation, requiring communication systems that are highly reliable to ensure safety, punctuality, and operational efficiency. The increasing demand for both passenger and freight services means that robust communication systems are indispensable for long-distance, high-speed rail operations, where real-time communication is crucial for seamless operations.

In the U.S., the train communication gateways system market commanded 80% of the global share in 2024. As the U.S. railway industry transitions toward electrification to reduce carbon emissions and increase efficiency, the demand for advanced communication systems has surged. Train communication gateways enable effective communication between new electric power systems and the existing train networks, ensuring seamless integration of all components. This integration is vital for the continued development of innovative rail technologies in the U.S. rail infrastructure.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Component providers

- 3.1.2 Service providers

- 3.1.3 Manufacturers

- 3.1.4 Technology providers

- 3.1.5 End customers

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Case study

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing demand for safety and operational efficiency

- 3.9.1.2 Adoption of smart and connected railways

- 3.9.1.3 Government investments in railway infrastructure

- 3.9.1.4 Technological advancements in communication systems

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High implementation costs

- 3.9.2.2 Integration challenges with legacy systems

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Offering, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 WTB gateways

- 5.3 MVB gateways

- 5.4 ECN gateways

Chapter 6 Market Estimates & Forecast, By Protocol, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 TCP/IP

- 6.3 IEC 61375

- 6.4 Profinet

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Passenger information systems

- 7.3 Security & surveillance systems

- 7.4 Train control systems

- 7.5 Data transfer and communication systems

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Train, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Mainline

- 8.3 Urban

- 8.4 Freight

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 North America

- 9.1.1 U.S.

- 9.1.2 Canada

- 9.2 Europe

- 9.2.1 UK

- 9.2.2 Germany

- 9.2.3 France

- 9.2.4 Italy

- 9.2.5 Spain

- 9.2.6 Russia

- 9.2.7 Nordics

- 9.3 Asia Pacific

- 9.3.1 China

- 9.3.2 India

- 9.3.3 Japan

- 9.3.4 Australia

- 9.3.5 South Korea

- 9.3.6 Southeast Asia

- 9.4 Latin America

- 9.4.1 Brazil

- 9.4.2 Mexico

- 9.4.3 Argentina

- 9.5 MEA

- 9.5.1 UAE

- 9.5.2 South Africa

- 9.5.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Advantech

- 10.2 Alstom

- 10.3 AMiT Transportation

- 10.4 Belden

- 10.5 Duagon

- 10.6 EKE-Electronics

- 10.7 ELTEC Elektronik

- 10.8 Ericsson

- 10.9 GE

- 10.10 HaslerRail

- 10.11 HollySys

- 10.12 Ingeteam

- 10.13 Moxa

- 10.14 Quester Tangent

- 10.15 Rockwell

- 10.16 SYS TEC Electronic

- 10.17 TTTech

- 10.18 UniControls