ワイヤレスアンテナ市場の機会、成長促進要因、産業動向分析、2025~2034年予測

Wireless Antenna Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 175 Pages

- 納期

- 2~3営業日

- 商品コード

- 1684722

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

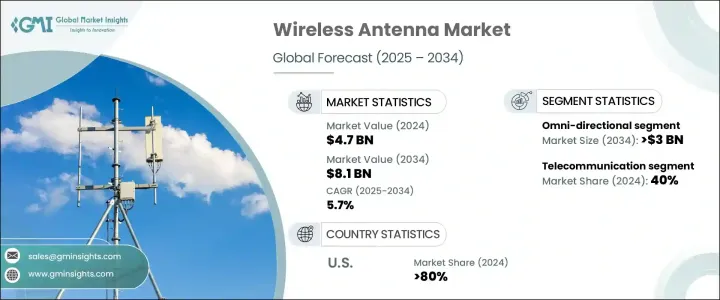

世界のワイヤレスアンテナ市場は、2024年に47億米ドルと評価され、2025年から2034年にかけてCAGR 5.7%で拡大する見通しです。

高速で信頼性の高い接続に対する需要の急増がこの成長を後押ししており、5G技術が技術革新の最前線にあります。通信事業者がネットワーク機能の強化を競う中、高度なワイヤレスアンテナのニーズは高まり続けています。スマートデバイス、産業オートメーション、IoTソリューションの採用が増加し、シームレスな通信に対する需要が高まっているため、高性能アンテナは現代の接続性に不可欠な要素となっています。

高周波、広帯域のワイヤレスネットワークへのシフトは、世界中の産業に変革をもたらしつつあります。世界の5G加入者数が急速に増加する中、通信事業者は中断のない接続性を確保するため、最先端のアンテナシステムの導入を競っています。この進化は、信頼性の高い無線通信が業務効率に不可欠な都市インフラ、スマートシティ、産業用アプリケーションにおいて特に重要です。さらに、自律走行車、遠隔ヘルスケアソリューション、次世代コンシューマーエレクトロニクスの拡大により、優れた信号伝送とネットワーク効率を実現するアンテナへの需要が高まっています。企業がデジタルトランスフォーメーションを優先する中、ワイヤレスアンテナ市場は大幅な成長を遂げ、企業、家庭、ミッションクリティカルなアプリケーションに不可欠な接続性を提供します。

| 市場規模 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 47億米ドル |

| 予測金額 | 81億米ドル |

| CAGR | 5.7% |

市場は無指向性アンテナ、半指向性アンテナ、高指向性アンテナに区分されます。全指向性アンテナは2024年に44%の市場シェアを占め、このセグメントを支配しています。360度のカバレッジを提供できるため、通信、Wi-Fiネットワーク、IoTアプリケーションに不可欠です。費用対効果、設置の容易さ、多様な環境への適応性により、業界を問わず好まれる選択肢となっています。接続性の要求が高まる中、これらのアンテナは、家庭、商業スペース、遠隔地でシームレスな通信ネットワークを維持する上で極めて重要な役割を果たしています。企業やサービスプロバイダーが堅牢なワイヤレスインフラを優先する中、全方向性アンテナは包括的なカバレッジを実現する信頼性の高いソリューションとして支持され続けています。

ワイヤレスアンテナは、通信、家電、自動車、航空宇宙・防衛、ヘルスケア、産業分野など、さまざまなアプリケーションをサポートしています。通信分野は、5Gネットワークの急速な拡大に牽引され、2024年の市場シェアの40%を占めています。これらのアンテナは、高速データ・トランスミッション、低遅延通信、最新のネットワーク・インフラで必要とされる広範なカバレッジを可能にするために不可欠です。これがなければ、次世代通信技術は、リアルタイム・アプリケーション、遠隔作業、産業オートメーションに必要な速度と信頼性を提供するのに苦労すると思われます。超高速接続に対する世界の需要が強まる中、ワイヤレスアンテナは次世代ネットワークのパフォーマンスを実現する重要な存在であり続けています。

米国のワイヤレスアンテナ市場は、研究開発および5Gインフラへの多額の投資に支えられ、2024年には80%のシェアを維持しました。主要通信企業やテクノロジー企業は、都市や産業環境でのシームレスな接続を促進するため、最先端のアンテナソリューションに積極的に投資しています。IoT、スマートシティ構想、自律システムの急速な普及が需要をさらに加速させ、米国を市場の支配的勢力として位置づけています。強力な技術エコシステムは、ワイヤレス通信の継続的な進歩と相まって、ワイヤレスアンテナ業界における米国のリーダーシップを強化し続けています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場範囲と定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 原材料サプライヤー

- 部品サプライヤー

- メーカー

- 技術プロバイダー

- エンドユーザー

- サプライヤーの状況

- 利益率分析

- 技術とイノベーションの展望

- 特許分析

- 規制状況

- 価格動向

- 影響要因

- 促進要因

- IoTとコネクテッドデバイスの需要拡大

- スマートテクノロジーとオートメーションの採用増加

- 通信と5Gネットワーク展開の成長

- 高速データ転送ソリューションへの需要の高まり

- 業界の潜在的リスク&課題

- 都市部および農村部の通信インフラにおける課題

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:アンテナ別、2021年~2034年

- 主要動向

- 無指向性

- テレビ

- ダイポール

- ホイップ

- GPS

- ラジオ

- 半指向性

- パッチ

- 対数周期

- 高指向性

- パラボラアンテナ

- グリッド

第6章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- LTE

- 5G

- Wi-Fi

- Zigbee

- Bluetooth

- GPS/GNSS

- その他

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 通信機器

- 家電

- 自動車

- 航空宇宙・防衛

- ヘルスケア

- 産業

- その他

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第9章 企業プロファイル

- Airgain

- Alpha Wireless

- Amphenol Antenna Solutions

- Antenova

- Broadcom

- Comba Telecom

- CommScope

- Ericsson

- Ezurio

- Huawei Technologies

- KATHREIN Solutions

- Molex

- Quintech Electronics &Communications

- RFS(Radio Frequency Systems)

- Rohde &Schwarz

- Shenzhen Sunway Communication

- Southwest Antenna

- Taoglas

- TE Connectivity

- ZTE

目次

The Global Wireless Antenna Market, valued at USD 4.7 billion in 2024, is on track to expand at a CAGR of 5.7% between 2025 and 2034. The surging demand for high-speed, reliable connectivity is driving this growth, with 5G technology at the forefront of innovation. As telecom providers compete to enhance network capabilities, the need for advanced wireless antennas continues to escalate. The rising adoption of smart devices, industrial automation, and IoT solutions is amplifying the demand for seamless communication, making high-performance antennas an integral component of modern connectivity.

The shift toward high-frequency, high-bandwidth wireless networks is transforming industries worldwide. With global 5G subscriptions increasing rapidly, telecom operators are racing to deploy cutting-edge antenna systems to ensure uninterrupted connectivity. This evolution is particularly critical in urban infrastructure, smart cities, and industrial applications, where reliable wireless communication is essential for operational efficiency. Additionally, the expansion of autonomous vehicles, remote healthcare solutions, and next-generation consumer electronics is fueling demand for antennas that deliver superior signal transmission and network efficiency. As enterprises prioritize digital transformation, the market for wireless antennas is poised for substantial growth, providing essential connectivity for businesses, households, and mission-critical applications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.7 Billion |

| Forecast Value | $8.1 Billion |

| CAGR | 5.7% |

The market is segmented into omni-directional, semi-directional, and highly directional antennas. Omni-directional antennas dominated the segment in 2024, holding a 44% market share. Their ability to provide 360-degree coverage makes them indispensable for telecommunications, Wi-Fi networks, and IoT applications. Their cost-effectiveness, ease of installation, and adaptability to diverse environments make them a preferred choice across industries. As connectivity demands rise, these antennas play a pivotal role in maintaining seamless communication networks in homes, commercial spaces, and remote locations. With enterprises and service providers prioritizing robust wireless infrastructure, omni-directional antennas continue to gain traction as a reliable solution for comprehensive coverage.

Wireless antennas support various applications, including telecommunications, consumer electronics, automotive, aerospace & defense, healthcare, and industrial sectors. The telecommunications segment accounted for 40% of the market share in 2024, driven by the rapid expansion of 5G networks. These antennas are vital for enabling high-speed data transmission, low-latency communication, and extensive coverage required by modern network infrastructures. Without them, next-generation communication technologies would struggle to deliver the speed and reliability necessary for real-time applications, remote work, and industrial automation. As global demand for ultra-fast connectivity intensifies, wireless antennas remain a crucial enabler of next-generation network performance.

The U.S. wireless antenna market maintained an 80% share in 2024, supported by substantial investments in research, development, and 5G infrastructure. Leading telecom companies and technology firms are actively investing in cutting-edge antenna solutions to facilitate seamless connectivity in urban and industrial settings. The rapid proliferation of IoT, smart city initiatives, and autonomous systems has further accelerated demand, positioning the U.S. as a dominant force in the market. A strong technological ecosystem, coupled with ongoing advancements in wireless communication, continues to reinforce the country's leadership in the wireless antenna industry.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material suppliers

- 3.1.2 Component suppliers

- 3.1.3 Manufacturers

- 3.1.4 Technology providers

- 3.1.5 End users

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Regulatory landscape

- 3.7 Price trends

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Expansion of IoT and connected devices demand

- 3.8.1.2 Rising adoption of smart technologies and automation

- 3.8.1.3 Growth in telecommunications and 5G network deployments

- 3.8.1.4 Increasing demand for high-speed data transfer solutions

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 Challenges in urban and rural coverage infrastructure

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Antenna, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Omni-directional

- 5.2.1 TV

- 5.2.2 Dipole

- 5.2.3 Whip

- 5.2.4 GPS

- 5.2.5 Radio

- 5.3 Semi-directional

- 5.3.1 Patch

- 5.3.2 Log-periodic

- 5.4 Highly directional

- 5.4.1 Parabolic dishes

- 5.4.2 Grid

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 LTE

- 6.3 5G

- 6.4 Wi-Fi

- 6.5 Zigbee

- 6.6 Bluetooth

- 6.7 GPS/GNSS

- 6.8 Others

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Telecommunications

- 7.3 Consumer electronics

- 7.4 Automotive

- 7.5 Aerospace and defense

- 7.6 Healthcare

- 7.7 Industrial

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.3.7 Nordics

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 South Africa

- 8.6.3 Saudi Arabia

Chapter 9 Company Profiles

- 9.1 Airgain

- 9.2 Alpha Wireless

- 9.3 Amphenol Antenna Solutions

- 9.4 Antenova

- 9.5 Broadcom

- 9.6 Comba Telecom

- 9.7 CommScope

- 9.8 Ericsson

- 9.9 Ezurio

- 9.10 Huawei Technologies

- 9.11 KATHREIN Solutions

- 9.12 Molex

- 9.13 Quintech Electronics & Communications

- 9.14 RFS (Radio Frequency Systems)

- 9.15 Rohde & Schwarz

- 9.16 Shenzhen Sunway Communication

- 9.17 Southwest Antenna

- 9.18 Taoglas

- 9.19 TE Connectivity

- 9.20 ZTE

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 175 Pages

- 納期

- 2~3営業日