次世代コンピューティング市場の機会、成長促進要因、産業動向分析、2025~2034年予測

Next Generation Computing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 175 Pages

- 納期

- 2~3営業日

- 商品コード

- 1684716

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

世界の次世代コンピューティング市場は、2024年に1,133億米ドルに達し、2025年から2034年にかけてCAGR 21.7%で成長すると予測されています。

さまざまな分野の組織が、業務効率の向上、意思決定の最適化、競争力の維持のために、最先端のコンピューティング・ソリューションに積極的に投資しています。人工知能(AI)、機械学習(ML)、ビッグデータ分析が進化を続けるなか、企業は優れたスピード、効率性、拡張性を実現するコンピューティング技術を求めています。次世代コンピューティングの需要は、膨大なデータセットの処理、複雑なシミュレーションの実行、リアルタイムのアナリティクスをサポートする必要性にも後押しされており、企業はワークフローを合理化し、生産性を向上させる高度なソリューションの導入を迫られています。

クラウド・コンピューティング、エッジ・コンピューティング、量子コンピューティングへの依存の高まりは、ヘルスケアや金融から製造業や防衛に至るまで、業界に革命をもたらしています。企業は次世代コンピューティングを活用し、自律システムのパワーアップ、サプライチェーン・オペレーションの最適化、サイバーセキュリティ・フレームワークの強化を図っています。AI主導のアプリケーションや高頻度取引プラットフォームの急速な普及は、高速コンピューティング・インフラの必要性をさらに高めています。政府機関や研究機関も量子コンピューティングやエクサスケールシステムに多額の投資を行い、計算能力を再定義する技術的ブレークスルーを加速させています。コンピューティング・アーキテクチャの継続的な進歩に伴い、企業はAIアクセラレーション、超高速処理、セキュアなコンピューティング環境を統合したソリューションを優先する傾向が強まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 1,133億米ドル |

| 予測金額 | 7,598億米ドル |

| CAGR | 21.7% |

コンポーネント別に見ると、市場はハードウェア、ソフトウェア、サービスに区分され、2024年のシェアはハードウェアが40%と圧倒的です。このセグメントは、AI専用プロセッサ、高性能GPU、高度なメモリ・コンポーネントのニーズの高まりにより、2034年には3,358億米ドルに達すると予想されます。各組織は、AI推論、ディープラーニングモデル、量子コンピューティングアプリケーションに対する需要の高まりをサポートするため、専用ハードウェアへの投資を進めています。高速プロセッサーと次世代GPUは、コンピューティング・パフォーマンスの最適化、シームレスなスケーラビリティの確保、データ集約的なワークロードに対する比類ない処理能力の提供において、極めて重要な役割を果たしています。チップアーキテクチャの進化と半導体技術の飛躍的進歩が、次世代コンピューティングハードウェアソリューションの拡大を後押ししています。

また、同市場は導入形態によってオンプレミスとクラウドに分類され、2024年の市場シェアはオンプレミスが52.2%を占めています。機密データや独自技術を扱う企業は、より高いセキュリティ、規制遵守、運用管理のために、社内のコンピューティング・インフラを優先します。銀行、ヘルスケア、防衛などの業界では、データ主権を維持し、サイバーリスクを最小限に抑えるため、オンプレミスの導入が引き続き支持されています。ミッションクリティカルなワークロードを管理する組織は、自社のセキュリティポリシーに合わせてカスタマイズされたコンピューティング環境を必要とするため、オンプレミス・ソリューションへの需要がさらに高まっています。サイバーセキュリティの脅威が進化する中、企業はAIを活用したセキュリティフレームワークをコンピューティングインフラに統合し、耐障害性を高めてデータ侵害を防ごうとしています。

米国は、AI、クラウド・コンピューティング、半導体製造への多額の投資で次世代コンピューティング分野をリードしており、2024年の市場シェアは35%と圧倒的です。同国の確立された研究エコシステムは、技術主導型企業や最先端インフラと相まって、先端コンピューティング技術の採用を加速させています。AIモデル、量子研究イニシアティブ、次世代データセンターの急速な展開は、高性能コンピューティングにおける米国の世界リーダーとしての地位を強化しています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場範囲と定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- ソリューションプロバイダー

- サービスプロバイダー

- テクノロジープロバイダー

- インテグレーター

- エンドユーザー

- サプライヤーの状況

- 利益率分析

- 技術とイノベーションの展望

- 特許分析

- 規制状況

- 影響要因

- 促進要因

- 高性能コンピューティングへの需要の高まり

- AIと機械学習の進歩

- データ生成量の増加と高速処理の必要性

- 業界の潜在的リスク&課題

- 導入コストの高さ

- スケーラビリティの課題

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ハードウェア

- ソフトウェア

- サービス

第6章 市場推計・予測:展開別、2021年~2034年

- 主要動向

- クラウド

- オンプレミス

第7章 市場推計・予測:企業規模別、2021年~2034年

- 主要動向

- 中小企業

- 大企業

第8章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 量子コンピューティング

- HPC

- 近似・確率コンピューティング

- エネルギー効率コンピューティング

- 熱力学コンピューティング

- メモリベースコンピューティング

- 光コンピューティング

- その他

第9章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- BFSI

- ヘルスケア

- IT・通信

- 運輸・物流

- エネルギー&公益事業

- 教育

- 製造業

- 政府機関

- その他

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- Alibaba

- Atos

- Cambridge

- Cisco

- Dell

- D-Wave Systems

- Fujitsu

- Hewlett Packard Enterprise(HPE)

- Honeywell International

- IBM

- Intel

- IonQ

- Microsoft

- NVIDIA

- PsiQuantum

- Rigetti Computing

- Samsung

- TSMC

- Xanadu Quantum

目次

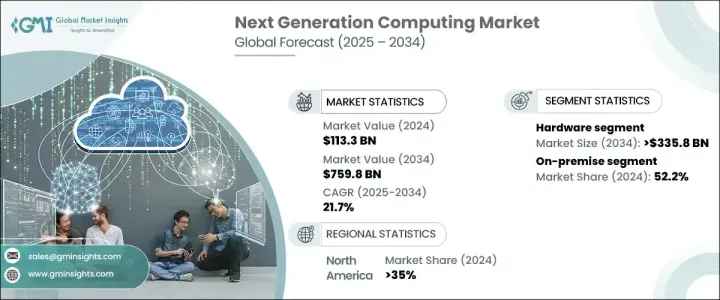

The Global Next Generation Computing Market reached USD 113.3 billion in 2024 and is estimated to grow at a CAGR of 21.7% from 2025 to 2034, fueled by the rising demand for high-performance computing solutions that can tackle complex computational challenges across industries. Organizations across multiple sectors are actively investing in cutting-edge computing solutions to drive operational efficiency, optimize decision-making, and maintain a competitive edge. As artificial intelligence (AI), machine learning (ML), and big data analytics continue to evolve, businesses seek computing technologies that deliver superior speed, efficiency, and scalability. The demand for next-generation computing is also driven by the need to process massive datasets, run intricate simulations, and support real-time analytics, pushing enterprises to adopt advanced solutions that streamline workflows and enhance productivity.

The growing reliance on cloud computing, edge computing, and quantum computing is revolutionizing industries, from healthcare and finance to manufacturing and defense. Enterprises are harnessing next-gen computing to power autonomous systems, optimize supply chain operations, and enhance cybersecurity frameworks. The rapid proliferation of AI-driven applications and high-frequency trading platforms further amplifies the need for high-speed computing infrastructures. Government agencies and research institutions are also making significant investments in quantum computing and exascale systems, accelerating technological breakthroughs that redefine computational capabilities. With continuous advancements in computing architectures, businesses are increasingly prioritizing solutions that integrate AI acceleration, ultra-fast processing, and secure computing environments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $113.3 Billion |

| Forecast Value | $759.8 Billion |

| CAGR | 21.7% |

By component, the market is segmented into hardware, software, and services, with hardware dominating at a 40% share in 2024. This segment is expected to reach USD 335.8 billion by 2034, driven by the increasing need for AI-specific processors, high-performance GPUs, and advanced memory components. Organizations are investing in specialized hardware to support the growing demand for AI inference, deep learning models, and quantum computing applications. High-speed processors and next-gen GPUs play a crucial role in optimizing computing performance, ensuring seamless scalability, and delivering unmatched processing power for data-intensive workloads. The evolution of chip architectures, coupled with breakthroughs in semiconductor technology, is propelling the expansion of next-gen computing hardware solutions.

The market is also classified by deployment into on-premise and cloud, with on-premise solutions holding a 52.2% market share in 2024. Enterprises handling sensitive data and proprietary technologies prioritize in-house computing infrastructure for greater security, regulatory compliance, and operational control. Industries such as banking, healthcare, and defense continue to favor on-premise deployments to maintain data sovereignty and minimize cyber risks. Organizations managing mission-critical workloads require customized computing environments tailored to their security policies, further driving demand for on-premise solutions. As cybersecurity threats evolve, businesses are integrating AI-powered security frameworks into their computing infrastructures to enhance resilience and prevent data breaches.

The United States accounted for a dominant 35% market share in 2024, leading the next-generation computing sector with substantial investments in AI, cloud computing, and semiconductor production. The country's well-established research ecosystem, combined with tech-driven enterprises and cutting-edge infrastructure, accelerates the adoption of advanced computing technologies. The rapid deployment of AI models, quantum research initiatives, and next-gen data centers reinforces the US's position as a global leader in high-performance computing.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Solution provider

- 3.1.2 Services provider

- 3.1.3 Technology provider

- 3.1.4 Integrators

- 3.1.5 End user

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Growing demand for high-performance computing

- 3.7.1.2 Advancements in AI and machine learning

- 3.7.1.3 Increasing data generation and the need for faster processing

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High costs of implementation

- 3.7.2.2 Scalability challenges

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Hardware

- 5.3 Software

- 5.4 Services

Chapter 6 Market Estimates & Forecast, By Deployment, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Cloud

- 6.3 On-premise

Chapter 7 Market Estimates & Forecast, By Enterprise Size, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 SME

- 7.3 Large enterprises

Chapter 8 Market Estimates & Forecast, By Type, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Quantum computing

- 8.3 HPC

- 8.4 Approximate and probabilistic computing

- 8.5 Energy efficiency computing

- 8.6 Thermodynamic computing

- 8.7 Memory based computing

- 8.8 Optical computing

- 8.9 Others

Chapter 9 Market Estimates & Forecast, By End Use Industry, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 BFSI

- 9.3 Healthcare

- 9.4 IT & telecom

- 9.5 Transportation & logistics

- 9.6 Energy & utility

- 9.7 Education

- 9.8 Manufacturing

- 9.9 Government

- 9.10 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Alibaba

- 11.2 Atos

- 11.3 Cambridge

- 11.4 Cisco

- 11.5 Dell

- 11.6 D-Wave Systems

- 11.7 Fujitsu

- 11.8 Google

- 11.9 Hewlett Packard Enterprise (HPE)

- 11.10 Honeywell International

- 11.11 IBM

- 11.12 Intel

- 11.13 IonQ

- 11.14 Microsoft

- 11.15 NVIDIA

- 11.16 PsiQuantum

- 11.17 Rigetti Computing

- 11.18 Samsung

- 11.19 TSMC

- 11.20 Xanadu Quantum

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 175 Pages

- 納期

- 2~3営業日