|

市場調査レポート

商品コード

1684708

データセンター用自動転送スイッチとスイッチギヤ市場の機会、成長促進要因、産業動向分析、2025年~2034年予測Data Center Automatic Transfer Switches and Switchgears Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| データセンター用自動転送スイッチとスイッチギヤ市場の機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年01月16日

発行: Global Market Insights Inc.

ページ情報: 英文 160 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

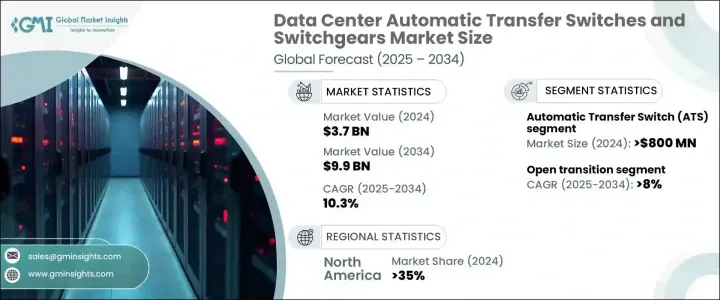

データセンター用自動転送スイッチとスイッチギヤの世界市場は、2024年に37億米ドルと評価され、2025年から2034年にかけて10.3%のCAGRで堅調に成長する見込みです。

データセンターのインフラ規模が急速に拡大するにつれ、信頼性の高い電源ソリューションに対するニーズが急増し、高度な電源管理技術に対する需要が高まっています。デジタル経済が拡大し続ける中、企業は業務を維持し、ダウンタイムを最小限に抑え、効率を高めるため、無停電電源への依存度を高めています。特に、クラウドコンピューティング、人工知能、ビッグデータなどの産業がデータ消費を飛躍的に増加させ続けているため、世界中の企業がシームレスなサービスの可用性を確保するため、バックアップ電源システムに多額の投資を行っています。

ハイパースケールデータセンターやコロケーションデータセンターの拡大により、信頼性の高い電源ソリューションへの注目が高まっています。同時に、業界規制の進化により、エネルギー効率、持続可能性、リスク軽減の重要性が強調され、高性能自動転送スイッチ(ATS)とスイッチギア・ソリューションの採用がさらに加速しています。いくつかの地域では送電網の安定性が依然として課題となっているため、データセンターは潜在的な停電に対処し、中断のない運用を確保するために、インテリジェントで自動化されたエネルギー管理技術への投資を優先しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 37億米ドル |

| 予測金額 | 99億米ドル |

| CAGR | 10.3% |

市場は2つの主要製品カテゴリーで構成される:自動転送スイッチ(ATS)とスイッチギアです。ATS分野は2024年に8億米ドル規模に達し、今後数年間で着実に拡大する見通しです。これらのシステムは、停電時にバックアップ電源にシームレスに切り替えることで、継続的な電力供給を維持する上で重要な役割を果たしています。ダウンタイムが莫大なコストに影響することを認識している企業では、ATSソリューションへの需要が急増し続けています。スマートATSユニットとデジタル監視機能の統合は、リアルタイムでの性能追跡と予知保全を可能にし、運用効率を高めています。

移行タイプ別の市場セグメンテーションには、オープン移行、クローズド移行、ソフト負荷移行、遅延移行が含まれます。オープン・トランジション分野は、影響を最小限に抑えながら電源間の切り替えが可能なことから、2025年から2034年にかけてCAGR 8%で成長すると予測されています。オープン・トランジション・スイッチは、代替電源に移行する前に一次電源から完全に切り離すことで機能し、移行プロセス中のシステム保護を保証します。エネルギー効率とコスト効率に優れたソリューションへの需要が高まっていることから、オープン・トランジションATSは、信頼性と運用の安定性を求める最新のデータセンターにとって好ましい選択肢となっています。

2024年のデータセンター用自動転送スイッチとスイッチギヤ市場では、北米が35%という大きなシェアを占めています。特に米国では、クラウドサービスやデータストレージソリューションが急成長しており、データセンター産業の急拡大につながっています。この急増は、高度な電力管理技術に対する需要の高まりに直接的に寄与しています。さらに、厳しい省エネルギー規制とバックアップ電源要件が、この地域の市場成長をさらに後押ししています。企業が次世代データセンターへの投資を続ける中、高性能の自動転送スイッチとスイッチギヤソリューションのニーズは加速し、北米市場の優位性はさらに高まると予想されます。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場範囲と定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- 部品メーカー

- メーカー

- 流通業者

- エンドユーザー

- 利益率分析

- 技術革新の状況

- 特許分析

- ATSの動作モード分析

- 規制状況

- 影響要因

- 促進要因

- データセンターにおける信頼性の高い電力供給に対する需要の増加

- より優れた性能と統合を可能にするスイッチギア技術の進歩

- データセンター運営におけるエネルギー効率と持続可能性の重視の高まり

- 安全性と信頼性のために自動転送スイッチの使用を促進する規制要件

- 業界の潜在的リスク&課題

- 先進的なトランスファースイッチ・スイッチギアの初期投資と設置コストが高い

- 既存の施設を最新の電力管理システムに改修する際の複雑さ

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- 自動転送スイッチ(ATS)

- スタティックトランスファースイッチ

- パワートランスファースイッチ

- ハイブリッドトランスファースイッチ

- スイッチギア

- 低電圧スイッチギア

- 中電圧スイッチギア

- 高電圧スイッチギア

第6章 市場推計・予測:変遷別、2021年~2034年

- 主要動向

- オープン移行

- クローズド移行

- ソフトロード移行

- 遅延移行

第7章 市場推計・予測:定格電流別、2021年~2034年

- 主要動向

- 300A未満

- 301-1000A

- 1001-2000A

- 2000A以上

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- クラウドサービスプロバイダー

- 企業

- 通信事業者

- 政府機関

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- ABB

- ASCO Power

- Caterpillar

- Cummins

- Eaton

- Emerson Electric

- Fuji Electric

- General Electric

- Kohler

- Legrand

- Mitsubishi Electric

- Myers Power Products

- Powell Industries

- Russelectric

- Schneider Electric

- Siemens

- Socomec

- Toshiba

- Vertiv

The Global Data Center Automatic Transfer Switches And Switchgears Market, valued at USD 3.7 billion in 2024, is set to grow at a robust CAGR of 10.3% between 2025 and 2034. As data center infrastructure rapidly scales, the need for reliable power supply solutions has surged, pushing demand for advanced power management technologies. With the ever-expanding digital economy, businesses are increasingly dependent on uninterrupted power to sustain operations, minimize downtime, and enhance efficiency. Companies worldwide are investing heavily in backup power systems to ensure seamless service availability, particularly as industries such as cloud computing, artificial intelligence, and big data continue to drive exponential growth in data consumption.

The expansion of hyperscale and colocation data centers has intensified the focus on dependable power solutions, as any disruptions can lead to significant financial losses and reputational damage. At the same time, evolving industry regulations emphasize the importance of energy efficiency, sustainability, and risk mitigation, further stimulating the adoption of high-performance automatic transfer switches (ATS) and switchgear solutions. As power grid stability remains a challenge in several regions, data centers are prioritizing investments in intelligent and automated energy management technologies to counteract potential outages and ensure uninterrupted operations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.7 Billion |

| Forecast Value | $9.9 Billion |

| CAGR | 10.3% |

The market comprises two primary product categories: Automatic Transfer Switches (ATS) and switchgear. The ATS segment, valued at USD 800 million in 2024, is poised for steady expansion over the coming years. These systems play a crucial role in maintaining continuous power supply by seamlessly switching to backup sources in the event of an outage. With businesses recognizing the immense cost implications of downtime, demand for ATS solutions continues to surge. The integration of smart ATS units with digital monitoring capabilities enhances operational efficiency, allowing for real-time performance tracking and predictive maintenance.

Market segmentation by transition type includes open transition, closed transition, soft load transition, and delayed transition. The open transition segment is projected to grow at a CAGR of 8% from 2025 to 2034 as it gains traction for its ability to switch between power sources with minimal impact. Open transition switches work by fully disconnecting from the primary power source before transitioning to an alternative, ensuring system protection during the process. The increasing demand for energy-efficient and cost-effective solutions makes open transition ATS a preferred choice for modern data centers seeking reliability and operational stability.

North America accounted for a substantial 35% share of the data center automatic transfer switches and switchgears market in 2024. The United States, in particular, has witnessed exponential growth in cloud services and data storage solutions, leading to rapid expansion of the data center industry. This surge has directly contributed to heightened demand for advanced power management technologies. Additionally, stringent energy conservation regulations and backup power requirements are further fueling market growth in the region. As enterprises continue to invest in next-generation data centers, the need for high-performance automatic transfer switches and switchgear solutions is expected to accelerate, reinforcing North America's dominance in the market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Component providers

- 3.2.2 Manufacturers

- 3.2.3 Distributors

- 3.2.4 End users

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Analysis of ATS modes of operation

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Increasing demand for reliable power supply in data centers

- 3.8.1.2 Advancements in switchgear technologies enabling better performance and integration

- 3.8.1.3 Growing emphasis on energy efficiency and sustainability in data center operations

- 3.8.1.4 Regulatory requirements promoting the use of automatic transfer switches for safety and reliability

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High initial investment and installation costs for advanced transfer switches and switchgears

- 3.8.2.2 Complexity in retrofitting existing facilities with modern power management systems

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Automatic Transfer Switches (ATS)

- 5.2.1 Static transfer switches

- 5.2.2 Power transfer switches

- 5.2.3 Hybrid transfer switches

- 5.3 Switchgears

- 5.3.1 Low voltage switchgear

- 5.3.2 Medium voltage switchgear

- 5.3.3 High voltage switchgear

Chapter 6 Market Estimates & Forecast, By Transition, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Open transition

- 6.3 Closed transition

- 6.4 Soft load transition

- 6.5 Delayed transition

Chapter 7 Market Estimates & Forecast, By Ampere Rating, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Below 300A

- 7.3 301-1000A

- 7.4 1001-2000A

- 7.5 Above 2000A

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Cloud service providers

- 8.3 Enterprises

- 8.4 Telecommunications

- 8.5 Government

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 ABB

- 10.2 ASCO Power

- 10.3 Caterpillar

- 10.4 Cummins

- 10.5 Eaton

- 10.6 Emerson Electric

- 10.7 Fuji Electric

- 10.8 General Electric

- 10.9 Kohler

- 10.10 Legrand

- 10.11 Mitsubishi Electric

- 10.12 Myers Power Products

- 10.13 Powell Industries

- 10.14 Russelectric

- 10.15 Schneider Electric

- 10.16 Siemens

- 10.17 Socomec

- 10.18 Toshiba

- 10.19 Vertiv