|

市場調査レポート

商品コード

1684704

基地局アンテナ市場の機会、成長促進要因、産業動向分析、2025年~2034年予測Base Station Antenna Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 基地局アンテナ市場の機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年01月16日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

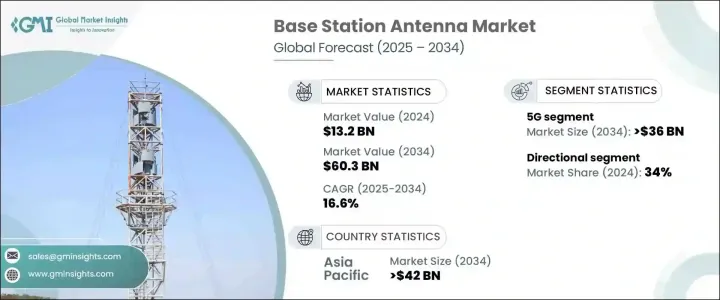

基地局アンテナの世界市場は2024年に132億米ドルに達し、2025年から2034年にかけてCAGR16.6%という予測もあり、大幅な成長が見込まれています。

5G技術の急速な拡大と成長し続けるモノのインターネット(IoT)エコシステムが、この市場成長の主な促進要因です。モバイルネットワークのトラフィックがかつてないペースで増加する中、高度な通信インフラに対する需要が急増しています。世界中のネットワーク・プロバイダーは、効率改善、ネットワーク性能の向上、データ消費量の急激な増加に対応するため、MIMO(Multiple Input Multiple Output)やアクティブ・アンテナなどの最先端技術に多額の投資を行っています。

政府や民間企業はデジタルトランスフォーメーションを優先しており、通信プロジェクトに巨額の投資を促しています。スマートシティ構想、農村部の接続プログラム、都市部のブロードバンドネットワークの拡大はすべて、高性能基地局アンテナの採用拡大に寄与しています。シームレスな高速接続に対する世界の信頼が高まる中、ネットワーク事業者は、人工知能主導型ネットワークやリアルタイム・データ・トランスミッションなどの新技術に対応するため、インフラのアップグレードに注力しています。5Gネットワークの広範な展開により、より高度でコンパクトなアンテナソリューションが求められ、より高い周波数伝送と広いカバレッジが可能になります。通信の近代化へのシフトは都心部に限ったことではなく、遠隔地や農村部でもインフラの大幅なアップグレードが行われており、信頼性の高い高速インターネットサービスへの幅広いアクセスが確保されています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 132億米ドル |

| 予測金額 | 603億米ドル |

| CAGR | 16.6% |

同市場は、5G、4G/LTE、3Gを主要カテゴリーとして技術別に区分されます。2024年には、5Gセグメントが市場の57%を占め、2034年までに360億米ドルの売上が見込まれています。Massive MIMOやビームフォーミングなどの高度な無線技術の導入は、特に人口密度の高い都市部におけるネットワーク容量とカバレッジに革命をもたらしました。これらの技術革新はデータ・トランスミッションを最適化し、高速化と信頼性の向上を実現しています。5Gネットワークが進化を続ける中、コンパクトでモバイルフレンドリーなアンテナソリューションのニーズも高まっており、交通量の多いゾーンでもシームレスな接続性を提供しています。

基地局アンテナ市場において、アンテナセグメントは無指向性、指向性、マルチビーム、スモールセル、ダイポール、その他のタイプに分類されます。2024年には、指向性アンテナのシェアが34%を占め、放射パターンを集中させることでカバレージと容量を強化できることから、好ましい選択肢として浮上しています。これらのアンテナは、ネットワークの干渉を減らしパフォーマンスを最適化することが重要な都市環境において、非常に有用であることが証明されています。5Gネットワークの広範な展開は、指向性アンテナの需要をさらに加速させています。指向性アンテナは、データ集約的な場所での高速・大容量接続をサポートする上で重要な役割を果たすからです。

2024年の世界の基地局アンテナ市場はアジア太平洋地域が67%のシェアを占め、2034年には420億米ドルに達すると予測されています。同地域では5Gインフラが積極的に展開されているため、Massive MIMOやビームフォーミングなどの最先端技術の採用が推進され、優れたネットワーク性能が確保されています。アジア太平洋諸国は、大都市圏と農村部の両方で広範なブロードバンドアクセスを提供するために、費用対効果の高いソリューションに投資しています。急速な都市化とスマートシティ構想は、基地局アンテナ技術への大規模な投資を促進し、この地域を世界の通信事情における重要なプレーヤーにしています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- 原材料サプライヤー

- アンテナメーカー

- OEMメーカー

- 販売業者およびシステム・インテグレーター

- 電気通信事業者

- エンドユーザー

- 利益率分析

- 技術とイノベーションの展望

- 特許分析

- コスト内訳分析

- 主要ニュースと取り組み

- 規制状況

- 技術の差別化要因

- MIMOとSISO

- アクティブアンテナとパッシブアンテナ

- シングルバンドとデュアルバンドアンテナ

- 影響要因

- 促進要因

- 世界の5Gネットワークの急速な展開

- 高速モバイル接続への需要の高まり

- IoTおよびスマートシティプロジェクトの拡大

- Massive MIMO技術の採用増加

- 業界の潜在的リスク&課題

- 高い設置費用とメンテナンス費用

- ネットワーク拡張に利用可能な周波数帯が限定的

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:アンテナ別、2021年~2034年

- 主要動向

- 無指向性

- 指向性

- マルチビーム

- スモールセル

- ダイポール

- その他

第6章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 5G

- 4G/LTE

- 3G

第7章 市場推計・予測:プロビジョン別、2021年~2034年

- 主要動向

- 都市部

- 郊外

- 農村部

第8章 市場推計・予測:設置数別、2021年~2034年

- 主要動向

- ルーフトップ

- タワー型

- 地上型

- 屋内型

- その他

第9章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 通信

- IoTとスマートシティ

- 防衛、公共安全

- 放送

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- ACE Technologies

- Alpha Wireless

- Amphenol

- Cobham Antenna Systems

- Comba Telecom Systems

- CommScope

- Ericsson

- Hengxin Technology

- Huawei

- Kaelus

- Laird Connectivity

- Mingxin Communication Technology

- Mobi Antenna

- Nokia

- Procom A/S

- Radio Frequency Systems

- Shenglu Communication

- Shenzhen Sunway Communication

- Shenzhen Tatfook Technology

- ZTE

The Global Base Station Antenna Market reached USD 13.2 billion in 2024 and is poised for substantial growth, with projections indicating a CAGR of 16.6% between 2025 and 2034. The rapid expansion of 5G technology and the ever-growing Internet of Things (IoT) ecosystem are the primary drivers of this market's growth. With mobile network traffic increasing at an unprecedented pace, the demand for advanced telecommunications infrastructure has surged. Network providers worldwide are investing heavily in cutting-edge technologies such as Multiple Input Multiple Output (MIMO) and active antennas to improve efficiency, enhance network performance, and manage the exponential rise in data consumption.

Governments and private enterprises are prioritizing digital transformation, fueling massive investments in telecommunication projects. Smart city initiatives, rural connectivity programs, and the expansion of urban broadband networks are all contributing to the increased adoption of high-performance base station antennas. As global reliance on seamless, high-speed connectivity grows, network operators are focusing on upgrading their infrastructure to accommodate emerging technologies such as artificial intelligence-driven networks and real-time data transmission. The widespread rollout of 5G networks is pushing for more sophisticated, compact antenna solutions, enabling higher frequency transmission and greater coverage. The shift toward modernized telecommunications is not limited to urban centers; even remote and rural areas are witnessing significant infrastructure upgrades, ensuring broader access to reliable, high-speed internet services.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $13.2 Billion |

| Forecast Value | $60.3 Billion |

| CAGR | 16.6% |

The market is segmented based on technology, with 5G, 4G/LTE, and 3G as the primary categories. In 2024, the 5G segment accounted for 57% of the market and is expected to generate USD 36 billion by 2034. The introduction of advanced wireless technologies such as Massive MIMO and beamforming has revolutionized network capacity and coverage, particularly in densely populated urban areas. These innovations are optimizing data transmission, ensuring faster speeds and improved reliability. As 5G networks continue to evolve, the need for compact, mobile-friendly antenna solutions is also growing, providing seamless connectivity even in high-traffic zones.

Within the base station antenna market, the antenna segment is categorized into omni-directional, directional, multi-beam, small cell, dipole, and other types. In 2024, directional antennas held a 34% share, emerging as the preferred choice due to their ability to enhance coverage and capacity by focusing radiation patterns. These antennas are proving to be invaluable in urban environments, where reducing network interference and optimizing performance is critical. The widespread deployment of 5G networks is further accelerating demand for directional antennas, as they play a key role in supporting high-speed, high-capacity connectivity in data-intensive locations.

Asia Pacific dominated the global base station antenna market in 2024, holding a 67% share, and is projected to generate USD 42 billion by 2034. The region's aggressive rollout of 5G infrastructure is driving the adoption of cutting-edge technologies such as Massive MIMO and beamforming, ensuring superior network performance. Countries across the Asia Pacific are investing in cost-effective solutions to provide widespread broadband access, both in metropolitan and rural areas. Rapid urbanization and smart city initiatives are fueling substantial investments in base station antenna technology, making the region a key player in the global telecommunications landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 360º synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material suppliers

- 3.2.2 Antenna manufacturers

- 3.2.3 OEMs

- 3.2.4 Distributors and system integrators

- 3.2.5 Telecom operators

- 3.2.6 End users

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Cost breakdown analysis

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Technology differentiators

- 3.9.1 MIMO vs SISO

- 3.9.2 Active vs passive antennas

- 3.9.3 Single band vs dual band antennas

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Rapid 5G network deployment worldwide

- 3.10.1.2 Increasing demand for high-speed mobile connectivity

- 3.10.1.3 Expansion of IoT and smart city projects

- 3.10.1.4 Rising adoption of Massive MIMO technology

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High installation and maintenance costs

- 3.10.2.2 Limited spectrum availability for network expansion

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Antenna, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Omni-directional

- 5.3 Directional

- 5.4 Multibeam

- 5.5 Small cell

- 5.6 Dipole

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 5G

- 6.3 4G/LTE

- 6.4 3G

Chapter 7 Market Estimates & Forecast, By Provision, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Urban

- 7.3 Suburban

- 7.4 Rural

Chapter 8 Market Estimates & Forecast, By Installation, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Rooftop

- 8.3 Tower-mounted

- 8.4 Ground-based

- 8.5 Indoor

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Telecommunications

- 9.3 IoT and smart cities

- 9.4 Defense and public safety

- 9.5 Broadcasting

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Number of base stations)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 ACE Technologies

- 11.2 Alpha Wireless

- 11.3 Amphenol

- 11.4 Cobham Antenna Systems

- 11.5 Comba Telecom Systems

- 11.6 CommScope

- 11.7 Ericsson

- 11.8 Hengxin Technology

- 11.9 Huawei

- 11.10 Kaelus

- 11.11 Laird Connectivity

- 11.12 Mingxin Communication Technology

- 11.13 Mobi Antenna

- 11.14 Nokia

- 11.15 Procom A/S

- 11.16 Radio Frequency Systems

- 11.17 Shenglu Communication

- 11.18 Shenzhen Sunway Communication

- 11.19 Shenzhen Tatfook Technology

- 11.20 ZTE