自動車用電力分配モジュール市場の機会、成長要因、業界動向分析、および2026年~2035年の予測

Automotive Power Distribution Modules Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035- 発行日

- ページ情報

- 英文 295 Pages

- 納期

- 2~3営業日

- 商品コード

- 2019240

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

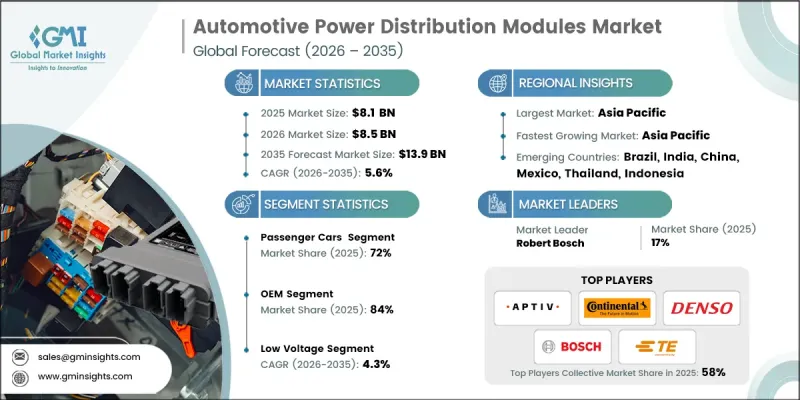

世界の自動車用電力分配モジュール市場は、2025年に81億米ドルと評価され、CAGR 5.6%で成長し、2035年までに139億米ドルに達すると推定されています。

この市場の成長を後押ししているのは、自動車の電気システムの複雑化が進んでいること、および乗用車と商用車の双方において電動パワートレインの採用が増加していることです。PDM(電力分配モジュール)は、バッテリー、オルタネーター、および複数の電気部品間の電力の流れを管理し、負荷が変動する状況下でも安定的かつ効率的な動作を確保する上で重要な役割を果たしています。従来のリレー・ヒューズボックスから、診断機能、通信プロトコル、熱管理機能を統合したスマートで軽量なモジュールへの移行が、インテリジェントなソリューションへの需要を牽引しています。車両の安全性、排出ガス、電動化に関する規制基準に加え、コネクテッドカー技術、ADAS、インフォテインメントシステムの成長が、市場の拡大を加速させています。特にハイブリッド車やバッテリー式電気自動車の生産台数の増加、およびアフターマーケットでの交換やアップグレードが、自動車用PDMセクターの持続的な成長にさらに寄与しています。

| 市場の範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測期間 | 2026年~2035年 |

| 開始時の市場規模 | 81億米ドル |

| 予測額 | 139億米ドル |

| CAGR | 5.6% |

乗用車セグメントは2025年に72%のシェアを占め、2026年から2035年にかけてCAGR5.1%で成長すると予想されています。乗用車が主導的な地位を占めているのは、世界の生産台数の多さに加え、効率的な電力管理を必要とするハイブリッド車や電気自動車の普及が進んでいるためです。現代の乗用車には、高度な電子機器、ADAS、コネクティビティシステム、インフォテインメントプラットフォームをサポートし、最適なエネルギー分配とシステム信頼性の向上を保証するインテリジェントなPDMが求められています。技術的に洗練された車両に対する消費者の嗜好の高まりが、このセグメントにおける先進的な電力分配モジュールの採用を後押しし続けています。

OEMチャネルは2025年に84%のシェアを占め、2026年から2035年にかけてCAGR5.8%が見込まれています。自動車メーカーは、特定の電気アーキテクチャ、性能基準、安全要件に合わせてカスタマイズされたOEM供給のモジュールに依存しています。これらのモジュールは、生産段階で乗用車、商用車、および電気自動車に組み込まれます。OEMチャネルでは、長期契約、IATF 16949認証への準拠、および厳格な品質検証が重視されており、これにより自動車用電子機器の信頼性と安全性が確保されています。ハイブリッド車およびバッテリー式電気自動車の普及が進むにつれ、複雑な電気システムや高電圧システムをサポートするための高度なPDMソリューションに対するOEMの需要がさらに高まっています。

中国の自動車用電力分配モジュール市場は、2026年から2035年にかけてCAGR5.1%で成長すると予測されています。同国の広大な自動車生産拠点と強固な電子部品サプライチェーンが相まって、高度な電力分配システムに対する堅調な需要を後押ししています。中国では、乗用車、商用車、電気自動車を含め、年間3,000万台以上の車両が生産されており、電子システム、デジタルコックピット、ADAS、コネクテッドカー技術を支えるインテリジェントPDMに対する大きな需要が生まれています。この優位性により、中国はアジア太平洋地域の自動車用PDM分野におけるイノベーションと普及の主要な推進力としての地位を確立しています。

よくあるご質問

目次

第1章 調査手法

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 車両フリートの急速な電動化およびEV/HEVへの移行

- 現代の自動車における電子機器の搭載増加(ADAS、インフォテインメント、コネクティビティ)

- ゾーンアーキテクチャおよびスマート電力配電ソリューションの導入

- 厳格な排出規制が高電圧システムの統合を促進

- 高度な安全性および快適性機能に対する消費者の需要

- 業界の潜在的リスク&課題

- 高度な電力分配モジュールの高コスト

- 多電圧システムの設計および統合における複雑性

- 半導体サプライチェーンの混乱および部品不足

- コンパクトな車内空間における熱管理の課題

- 市場機会

- 乗用車における48Vマイルドハイブリッドシステムの普及

- アフターマーケット向けスマートPDMソリューションの導入

- 新興市場における自動車生産の成長

- V2G(Vehicle-to-Grid)インフラとの連携

- モジュール式かつ拡張可能なPDMプラットフォームの開発

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 米国環境保護庁(EPA)の温室効果ガス規制第3段階およびCAFE基準

- カナダ- 排出量に基づく規制枠組み

- 欧州

- ドイツ- ユーロ7排出ガス基準

- 英国- ブレグジット後の車両型式認定

- フランス- 脱炭素化ロードマップ

- イタリア- 低排出ゾーンの遵守状況

- アジア太平洋地域

- 中国- 中国VI-bおよび新興中国VII基準

- インド-BS-VIステージIIおよびBharat Stage VIIへの移行

- 日本- 燃費基準(2030年目標)

- オーストラリア- 燃料品質およびADR 79/05規格

- ラテンアメリカ

- メキシコ-NOM-194-SE-2021およびUSMCA原産地規則

- アルゼンチン- 法律第24.449号および環境関連改正

- 中東・アフリカ(MEA)

- 南アフリカ- 道路交通法(1996年)

- サウジアラビア- 交通法規およびビジョン2030の交通イニシアチブ

- 北米

- ポーター分析

- PESTEL分析

- 技術およびイノベーションの動向

- 現在の技術動向

- 新興技術

- 特許動向(1次調査に基づく)

- 価格分析(1次調査に基づく)

- 過去の価格動向分析

- 事業者タイプ別の価格戦略(プレミアム/バリュー/コストプラス)

- 総所有コスト(TCO)分析

- 貿易データ分析(有料データベースに基づく)

- 輸出入量および金額の動向

- 主要な貿易回廊および関税の影響

- 使用事例と成功事例

- AIおよび生成AIが市場に与える影響

- AIによる既存ビジネスモデルの変革

- セグメント別のGenAI使用事例および導入ロードマップ

- リスク、制限事項および規制上の考慮事項

- 生産能力および生産動向(1次調査に基づく)

- 地域別および主要生産者別の設備容量

- 稼働率および拡張計画

- サステナビリティおよび環境面

- 持続可能な取り組み

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- カーボンフットプリントに関する考察

- 予測の前提条件およびシナリオ分析(1次調査に基づく)

- ベースケース-CAGRを牽引する主要なマクロ経済および業界変数

- 楽観的シナリオ- マクロ経済および業界における追い風

- 悲観シナリオ- マクロ経済の減速または業界の逆風

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 企業のティア別ベンチマーク

- ティア分類基準および選定基準

- 売上高、地域、イノベーション別のティア・ポジショニング・マトリックス

- 主な発展

- 合併・買収

- パートナーシップおよび提携

- 新製品の発売

- 事業拡大計画と資金調達

第5章 市場推計・予測:コンポーネント別、2022-2035

- パワーモジュール

- ヒューズおよび遮断器

- コネクタおよび端子

- リレー

- 電圧レギュレータ

- その他

第6章 市場推計・予測:モジュール別、2022-2035

- 低電圧

- 中電圧

- 高電圧

第7章 市場推計・予測:車両別、2022-2035

- 乗用車

- ハッチバック

- セダン

- SUV

- 商用車

- 小型商用車(LCV)

- 中型商用車(MCV)

- 大型商用車(HCV)

第8章 市場推計・予測:販売チャネル別、2022-2035

- OEM

- アフターマーケット

第9章 市場推計・予測:用途別、2022-2035

- 照明システム

- インフォテインメントシステム

- HVACシステム

- 安全・運転支援システム

- パワートレインシステム

- バッテリー管理システム

- その他

第10章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- オランダ

- スウェーデン

- デンマーク

- ポーランド

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- シンガポール

- タイ

- インドネシア

- ベトナム

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- コロンビア

- 中東・アフリカ(MEA)

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- イスラエル

第11章 企業プロファイル

- 世界企業

- Aptiv

- Continental

- Denso

- Eaton

- Hitachi Astemo

- Lear

- Mitsubishi Electric

- Robert Bosch

- TE Connectivity

- Valeo

- 地域企業

- DRAXLMAIER

- Furukawa Electric

- Leoni

- Panasonic Automotive Systems

- Sumitomo Electric Industries

- Yazaki

- 新興企業

- Infineon Technologies

- NXP Semiconductors

- onsemi(ON Semiconductor)

- STMicroelectronics

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 295 Pages

- 納期

- 2~3営業日