|

市場調査レポート

商品コード

1684695

データセンター用エネルギー貯蔵市場の機会、成長促進要因、産業動向分析、2025年~2034年予測Data Center Energy Storage Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| データセンター用エネルギー貯蔵市場の機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年01月16日

発行: Global Market Insights Inc.

ページ情報: 英文 175 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

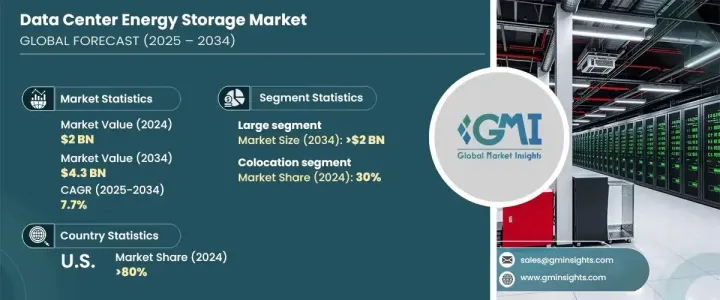

世界のデータセンター用エネルギー貯蔵市場は2024年に20億米ドルと評価され、力強い成長軌道にあり、2025年から2034年のCAGRは7.7%と予測されています。

デジタルサービスの需要が急増する中、データセンターは、中断のない電力供給を確保し、エネルギー消費を最適化する効率的なエネルギー貯蔵ソリューションの導入にますます迫られています。企業は従来の電力網から脱却し、代わりに持続可能性の目標に沿い、運用の回復力を高める高度な蓄電技術に注目するようになっています。二酸化炭素排出量やエネルギーコストの上昇に対する懸念が高まる中、再生可能エネルギーの統合を推進する動きはかつてないほど強まっています。企業は最先端のストレージ・システムを活用することで、稼働時間を維持し、電気料金を削減し、より環境に優しいデジタル・インフラへの移行を支援しています。

クラウド・コンピューティング、人工知能、ビッグデータ分析の急速な拡大により、スケーラブルなエネルギー貯蔵ソリューションの必要性が高まっています。デジタルトランザクションとデータ処理は拡大を続け、高性能コンピューティングを維持できるエネルギー効率の高いシステムへの依存度が高まっています。世界中の組織は、電力の信頼性を向上させ、ダウンタイムのリスクを最小限に抑えるため、革新的なエネルギー貯蔵技術に投資しています。規制の枠組みが持続可能性を重視する中、データセンターは進化する市場で競争力を維持するため、環境に優しいエネルギーソリューションを優先しています。リチウムイオンバッテリー、フライホイール、その他のエネルギー効率に優れたシステムを組み込んだハイブリッド・エネルギー・ストレージへの移行は、レジリエントで持続可能なインフラへの移行をさらに強調しています。電源管理システムの継続的な進歩により、データセンターは高速コンピューティング性能を維持しながらエネルギー効率を最適化しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 20億米ドル |

| 予測金額 | 43億米ドル |

| CAGR | 7.7% |

データセンターの規模による市場セグメンテーションには、小規模、中規模、大規模施設が含まれます。2024年には、大規模データセンターが市場シェアの46%を占め、売上予測は2034年までに20億米ドルに達します。大容量データセンターは、シームレスな運用を保証し、重要なコンピューティング環境の中断を防ぐために、高度なエネルギー貯蔵ソリューションに依存しています。エネルギー需要の増加に伴い、企業はシステムの回復力を強化し、停電を減らし、エネルギー効率を最適化するために、高度なストレージ技術を統合しています。こうした大規模センターでは、増大するデータ負荷をサポートする堅牢なストレージインフラが必要とされ、エネルギーストレージシステムへの大規模な投資が推進されています。

市場はさらに用途別に分類され、銀行、エネルギー、政府、ヘルスケア、製造、IT、コロケーションサービスが含まれます。2024年には、コロケーションセンターの市場シェアが30%を占め、共有データストレージ施設への嗜好の高まりを反映しています。コロケーション・サービスを利用する企業は、継続的な電力供給を優先するため、エネルギー貯蔵ソリューションが運用戦略に不可欠な要素となっています。サードパーティ製データストレージへの依存度が高まるにつれ、エネルギー効率の高いインフラへの需要が高まり、コロケーションプロバイダーは最先端の電力管理ソリューションを導入せざるを得なくなっています。高度なエネルギー貯蔵技術は、信頼性を維持しながらコスト効率の高い運用を実現し、この分野での採用をさらに促進しています。

米国のデータセンター用エネルギー貯蔵市場は、2024年の世界シェアの80%を占め、業界の主要な牽引役としての地位を固めています。同地域は大規模インフラプロジェクトで主導権を握っており、企業がより柔軟で費用対効果の高いエネルギー消費戦略を求めているため、先進的なストレージソリューションの採用が加速しています。北米全域の企業は、持続可能性目標を達成し、二酸化炭素排出量を削減し、電力の信頼性を向上させるため、エネルギー効率化イニシアチブを積極的に強化しています。環境に優しいインフラへの強い関心とエネルギー貯蔵技術への継続的な投資により、この地域は市場成長の最前線に位置しています。カーボンニュートラルの達成に向けた取り組みが進む中、北米のデータセンターはエネルギー効率の新たな基準を設定し、市場の拡大と長期的な存続可能性を強化しています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場範囲と定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 原材料サプライヤー

- 部品サプライヤー

- メーカー

- 技術プロバイダー

- 流通業者

- エンドユーザー

- サプライヤーの状況

- 利益率分析

- 技術とイノベーションの展望

- 特許分析

- 規制状況

- 価格分析

- 影響要因

- 促進要因

- 効率化のための再生可能エネルギー源の統合

- データセンターにおけるバックアップ電源ソリューションの需要

- グリーンエネルギー貯蔵ソリューションの採用

- エネルギー貯蔵システムの技術的進歩

- 業界の潜在的リスク&課題

- エネルギー貯蔵技術の高い初期費用

- 大規模展開における技術的限界

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:データセンター規模別、2021年~2034年

- 主要動向

- 小規模

- 中規模

- 大規模

第6章 市場推計・予測:ティア別、2021年~2034年

- 主要動向

- ティア1

- ティア2

- ティア3

- ティア4

第7章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- リチウムイオン電池

- 鉛蓄電池

- ニッケル・カドミウム電池

- フライホイール蓄電

- スーパーキャパシタ

- フロー電池

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- BFSI

- コロケーション

- エネルギー

- 政府機関

- ヘルスケア

- 製造業

- IT・通信

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- ABB

- BYD

- Cummins

- Delta

- Eaton

- Generac Power Systems

- Hitachi Energy

- Huawei

- Johnson Controls International

- Legrand

- LG Energy Solution

- Mitsubishi

- Riello Elettronica

- Samsung SDI

- Schneider Electric

- Siemens

- Socomec

- Tesla

- Toshiba

- Vertiv

The Global Data Center Energy Storage Market, valued at USD 2 billion in 2024, is on a strong growth trajectory, with a projected CAGR of 7.7% between 2025 and 2034. As the demand for digital services surges, data centers are under increasing pressure to adopt efficient energy storage solutions that ensure uninterrupted power supply and optimize energy consumption. Businesses are moving away from traditional power grids, focusing instead on advanced storage technologies that align with sustainability goals and enhance operational resilience. With growing concerns over carbon footprints and rising energy costs, the push for renewable energy integration is stronger than ever. Companies are leveraging cutting-edge storage systems to maintain uptime, reduce electricity expenses, and support the shift toward a greener digital infrastructure.

The rapid expansion of cloud computing, artificial intelligence, and big data analytics has intensified the need for scalable energy storage solutions. Digital transactions and data processing continue to escalate, increasing dependency on energy-efficient systems that can sustain high-performance computing. Organizations worldwide are investing in innovative energy storage technologies to improve power reliability and minimize the risk of downtime. As regulatory frameworks emphasize sustainability, data centers are prioritizing eco-friendly energy solutions to remain competitive in the evolving market. The industry's transition toward hybrid energy storage, incorporating lithium-ion batteries, flywheels, and other energy-efficient systems, further underscores the shift toward a resilient, sustainable infrastructure. With the continued advancement of power management systems, data centers are optimizing energy efficiency while maintaining high-speed computing performance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2 Billion |

| Forecast Value | $4.3 Billion |

| CAGR | 7.7% |

Market segmentation by data center size includes small, medium, and large facilities. In 2024, large data centers accounted for 46% of the market share, with revenue projections reaching USD 2 billion by 2034. High-capacity data centers depend on sophisticated energy storage solutions to ensure seamless operations, preventing disruptions in critical computing environments. As energy demands rise, businesses are integrating advanced storage technologies to enhance system resilience, reduce power failures, and optimize energy efficiency. These large-scale centers require robust storage infrastructure to support increasing data loads, driving significant investments in energy storage systems.

The market is further categorized by application, covering banking, energy, government, healthcare, manufacturing, IT, and colocation services. In 2024, colocation centers held a 30% market share, reflecting the growing preference for shared data storage facilities. Businesses utilizing colocation services prioritize continuous power availability, making energy storage solutions an essential component of their operational strategy. The increasing reliance on third-party data storage has intensified the demand for energy-efficient infrastructure, compelling colocation providers to implement cutting-edge power management solutions. Advanced energy storage technology ensures cost-effective operations while maintaining reliability, further driving adoption across the sector.

The US data center energy storage market accounted for 80% of the global share in 2024, solidifying its position as a major industry driver. The region's leadership in large-scale infrastructure projects has accelerated the adoption of advanced storage solutions as businesses seek more flexible and cost-effective energy consumption strategies. Companies across North America are actively enhancing energy efficiency initiatives to meet sustainability targets, reducing carbon emissions, and improving power reliability. The strong focus on eco-friendly infrastructure and continuous investment in energy storage technologies have positioned the region at the forefront of market growth. With increasing efforts to achieve carbon neutrality, North American data centers are setting new standards for energy efficiency, reinforcing market expansion and long-term viability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material suppliers

- 3.1.2 Component suppliers

- 3.1.3 Manufacturers

- 3.1.4 Technology providers

- 3.1.5 Distributors

- 3.1.6 End users

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Regulatory landscape

- 3.7 Pricing analysis

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Integration of renewable energy sources for efficiency

- 3.8.1.2 Demand for backup power solutions in data centers

- 3.8.1.3 Adoption of green energy storage solutions

- 3.8.1.4 Technological advancements in energy storage systems

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High upfront costs of energy storage technologies

- 3.8.2.2 Technological limitations in large-scale deployments

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Data Center Size, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Small

- 5.3 Medium

- 5.4 Large

Chapter 6 Market Estimates & Forecast, By Tier, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Tier 1

- 6.3 Tier 2

- 6.4 Tier 3

- 6.5 Tier 4

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Lithium-ion batteries

- 7.3 Lead-acid batteries

- 7.4 Nickel-cadmium batteries

- 7.5 Flywheel energy storage

- 7.6 Supercapacitors

- 7.7 Flow batteries

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 BFSI

- 8.3 Colocation

- 8.4 Energy

- 8.5 Government

- 8.6 Healthcare

- 8.7 Manufacturing

- 8.8 IT & telecom

- 8.9 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 ABB

- 10.2 BYD

- 10.3 Cummins

- 10.4 Delta

- 10.5 Eaton

- 10.6 Generac Power Systems

- 10.7 Hitachi Energy

- 10.8 Huawei

- 10.9 Johnson Controls International

- 10.10 Legrand

- 10.11 LG Energy Solution

- 10.12 Mitsubishi

- 10.13 Riello Elettronica

- 10.14 Samsung SDI

- 10.15 Schneider Electric

- 10.16 Siemens

- 10.17 Socomec

- 10.18 Tesla

- 10.19 Toshiba

- 10.20 Vertiv