|

市場調査レポート

商品コード

1928911

船舶用レーダー市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Marine Radar Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 船舶用レーダー市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2026年01月09日

発行: Global Market Insights Inc.

ページ情報: 英文 225 Pages

納期: 2~3営業日

|

概要

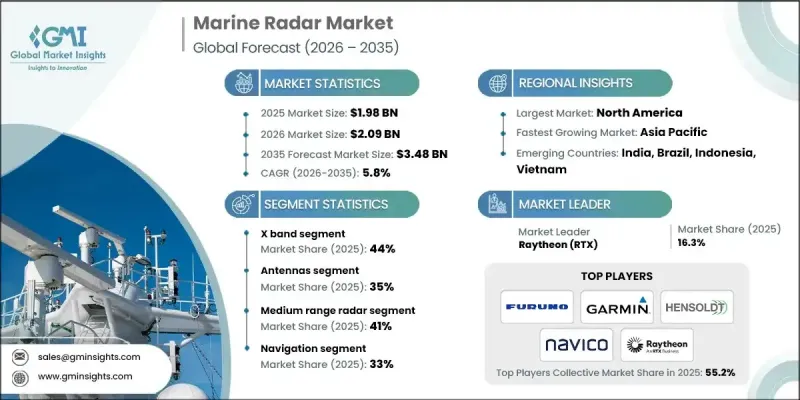

世界の船舶用レーダー市場は、2025年に19億8,000万米ドルと評価され、2035年までにCAGR5.8%で成長し、34億8,000万米ドルに達すると予測されています。

海上貿易量の増加と船舶の混雑化が進む中、信頼性の高い航行・監視システムの必要性が高まっています。交通量の多い水路における海難事故への警戒感の高まりが、先進的なレーダーソリューションへの投資拡大を促しています。レーダー技術の継続的な革新により更新サイクルが加速する一方、老朽化した商用・防衛艦隊が代替需要を牽引しています。ソリッドステートレーダーソリューションは、耐久性、動作安定性、およびメンテナンス需要の低減により、ますます支持されています。船舶レーダーシステムは現在、状況認識を向上させるため、電子海図プラットフォームや船舶識別技術との統合がより頻繁に行われています。船舶交通監視サービスの拡大は、沿岸および陸上ベースのレーダー設置に対する需要を支えています。視界不良時の航行精度への関心の高まりは、レーダー性能基準をさらに向上させています。艦隊近代化イニシアチブも、レーダー交換に対する持続的な需要に寄与しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 19億8,000万米ドル |

| 予測金額 | 34億8,000万米ドル |

| CAGR | 5.8% |

Xバンドセグメントは2025年に44%のシェアを占め、2026年から2035年にかけてCAGR5.3%で成長すると予測されています。これらのシステムは、短距離から中距離における航行支援、衝突回避、運用制御に広く利用されています。国際海事規制では、総トン数300トンを超える船舶へのレーダー設置が義務付けられており、セグメントの需要を後押ししています。

アンテナセグメントは2025年に35%のシェアを占め、2035年までCAGR5.3%で成長する見込みです。性能精度、探知範囲、解像度は商業船隊や漁船隊においてアンテナの品質に大きく依存するため、アンテナはレーダー保守費用の大部分を占めています。

米国海洋レーダー市場は2025年に88%のシェアを占め、5億7,450万米ドルに達しました。商業船舶、海軍作戦、レクリエーションボートにおける高い採用率に加え、厳格な海上安全基準と密集した沿岸交通が相まって、現代的なレーダーシステムへの継続的な需要を支え続けています。

よくあるご質問

目次

第1章 調査手法

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 世界海運貿易の成長

- より厳格な海上安全規制

- 沿岸水域および港湾水域における交通渋滞の増加

- 技術アップグレードとデジタル統合

- 業界の潜在的リスク&課題

- 高い設置および保守コスト

- 混雑海域における信号干渉とクラッター

- 市場機会

- 老朽化する世界の船隊からの改修需要

- 洋上風力および洋上エネルギープロジェクトの拡大

- ソリッドステートおよびデジタルレーダーの採用動向

- 成長可能性分析

- 規制情勢

- 北米

- 米国沿岸警備隊(USCG)レーダー搭載および観測要員要件

- 米国沿岸警備隊(USCG)による46 CFRに基づくレーダー装置の承認

- 連邦通信委員会(FCC)レーダー認証基準

- カナダ運輸省海洋レーダー適合ガイドライン

- 欧州

- 欧州海上安全庁(EMSA)の監督と実施

- 船舶用機器指令(MED)型式承認要件

- EU旗国及び港湾国管理によるレーダー検査

- レーダー装置に関する調和された欧州規格(EN)

- アジア太平洋地域

- 中国船級協会(CCS)レーダー型式承認基準

- インド海運総局レーダー適合規則

- 国土交通省レーダー規制

- 韓国海事局(KR)レーダー要件

- ASEAN地域海上安全及びレーダー調和ガイドライン

- ラテンアメリカ

- ブラジル海事局(ANTAQ)レーダー装置基準

- アルゼンチン沿岸警備隊レーダー適合規制

- メキシコ海軍・運輸省レーダー規則

- 地域別SOLAS実施状況と旗国管理

- 中東・アフリカ

- アラブ首長国連邦連邦運輸局海事レーダー基準

- サウジアラビア港湾庁レーダー要件

- 南アフリカ海事安全庁(SAMSA)の規制

- 地域別における国際海事機関(IMO)及び国際電気標準会議(IEC)レーダー性能基準の採用状況

- 北米

- ポーターの分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 生産統計

- 生産拠点

- 消費ハブ

- 輸出と輸入

- コスト内訳分析

- レーダーシステムの取得コスト

- 設置および統合コスト

- 運用および保守コスト

- ソフトウェアアップグレードおよびキャリブレーション費用

- 規制認証および型式承認コスト

- 訓練および乗組員習熟コスト

- 特許分析

- 持続可能性と環境面

- 持続可能な実践

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境配慮型イニシアチブ

- カーボンフットプリントに関する考慮事項

- 船舶用レーダーシステムアーキテクチャ及び統合フレームワーク

- スタンドアロン型と統合ブリッジシステム(IBS)の比較

- ECDIS、AIS、ARPA、INSとのレーダー統合

- オープン型とプロプライエタリ型の航法システムアーキテクチャ

- センサー融合環境におけるレーダーの役割

- OEM差別化と技術ポジショニング要因

- 探知距離、分解能、およびクラッター抑制のベンチマーク

- ソリッドステートレーダーとマグネトロンレーダーの差別化

- ソフトウェア定義レーダーの機能

- 信頼性、平均故障間隔(MTBF)、およびライフサイクル性能指標

- レトロフィットと新造船の需要動向

- SOLAS、IMO及び海軍調達基準の影響

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画と資金調達

第5章 市場推計・予測:レーダー別、2022-2035

- Xバンド

- Sバンド

- Cバンドレーダー

- その他

第6章 市場推計・予測:コンポーネント別、2022-2035

- 送信機

- アンテナ

- 受信機

- プロセッサー

- ディスプレイ

- その他

第7章 市場推計・予測:範囲別、2022-2035

- 短距離レーダー(1~20海里)

- 中距離レーダー(20~50海里)

- 長距離レーダー(50~100海里以上)

第8章 市場推計・予測:用途別、2022-2035

- ナビゲーション

- 衝突回避

- 監視・セキュリティ

- 漁業活動

- 沿岸交通の監視

- 気象監視

- その他

第9章 市場推計・予測:最終用途別、2022-2035

- 商用船舶

- 海軍・防衛/軍事用船舶

- レクリエーション用ボート/ヨット

- 個人所有のボート所有者

- 漁船

- その他

第10章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- オランダ

- スウェーデン

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- シンガポール

- タイ

- インドネシア

- ベトナム

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ地域

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

第11章 企業プロファイル

- 世界プレイヤー

- BAE Systems

- Furuno Electric

- Garmin

- Hensoldt

- Kongsberg Gruppen

- Leonardo

- Lockheed Martin

- Navico

- Northrop Grumman

- Raymarine

- Raytheon RTX

- Saab

- Sperry Marine

- Teledyne FLIR

- Thales

- 地域プレーヤー

- GEM Elettronica

- JRC Nisshinbo

- Koden Electronics

- Samyung ENC

- TOKIO KEIKI

- 新興企業/ディスラプター

- Alphatron Marine

- Rutter

- Terma