中央車両コントローラー市場の機会、成長促進要因、産業動向分析、2025~2034年予測

Central Vehicle Controller Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 175 Pages

- 納期

- 2~3営業日

- 商品コード

- 1684686

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

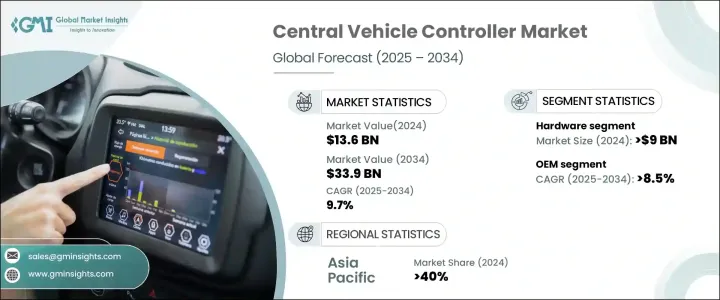

中央車両コントローラーの世界市場は、2024年に136億米ドルとなり、電気自動車(EV)の普及と高度な車両制御システムに対するニーズの高まりを背景に、2025年から2034年にかけてCAGR 9.7%で拡大する見通しです。

自動車メーカーが効率を高め、ハードウェアの複雑さを軽減する革新的なソリューションを求める中、CVCは最新の車両アーキテクチャにおける重要なコンポーネントとして浮上しています。これらのコントローラは、複数の車両機能を集中システムに統合し、エネルギーの最適化、リアルタイムのデータ利用、車両全体の性能を向上させます。制御操作を合理化することで、メーカーはアダプティブ・クルーズ・コントロール、レーンキーピング・アシスタンス、自律走行機能などのインテリジェント機能を統合することができます。

車両の電動化とコネクティビティが業界の優先事項となる中、こうした先進的なコントローラーの需要は急増し続けています。さらに、スマートモビリティ・ソリューションとソフトウェア定義車両の台頭がCVC技術への投資をさらに加速させ、自動車メーカーは性能、安全性、持続可能性を高めることができます。低排出ガスと車両効率向上を求める規制圧力が高まる中、自動車業界は、優れた機能性、コスト削減、進化するモビリティ・エコシステムとのシームレスな統合を実現する集中制御アーキテクチャへの移行を積極的に進めています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 136億米ドル |

| 予測金額 | 339億米ドル |

| CAGR | 9.7% |

市場はハードウェア・コンポーネントとソフトウェア・コンポーネントに区分され、2024年にはハードウェア・セグメントが90億米ドルで優位を占めています。このセグメントの急拡大は、集中型車両制御をサポートする高性能コンピューティング・システムに対する需要の高まりに起因しています。これらのハードウェア・ソリューションは、リアルタイム・ナビゲーション、自動ブレーキ、予知保全など、高度な車両機能を実現する上で重要な役割を果たしています。EVの増産とADAS(先進運転支援システム)の推進に伴い、自動車メーカーは車両のインテリジェンスと応答性を高めるエネルギー効率の高いハードウェア・ソリューションに多額の投資を行っています。自動車技術の進歩に伴い、強力なプロセッサー、高度なセンサー、人工知能ベースの制御システムの統合が、このセグメントのさらなる成長を促進すると予想されます。

最終用途別では、市場は相手先ブランド製造(OEM)とアフターマーケットに分類され、OEMがこのセグメントをリードしています。OEM市場は、2025年から2034年にかけてCAGR 8.5%で拡大すると予測されており、これは自動車メーカーの集中型車両アーキテクチャへのシフトが原動力となっています。これらのシステムにより、メーカーは生産プロセスを合理化し、ハードウェアの冗長性を減らし、車両効率を高めることができます。CVCの統合により、自動車メーカーは排ガス、サイバーセキュリティ、車両の安全性に関する厳しい規制基準を満たすことができます。自動車がソフトウェア中心になるにつれ、OEMは接続性の向上、メンテナンスコストの削減、車両設計の将来性を考慮して、これらのシステムの採用を優先しています。

アジア太平洋地域は依然として最大の地域市場であり、2024年の世界シェアの40%を占めています。同地域の優位性は、EV採用の増加、政府の強力なインセンティブ、自動車技術の大幅な進歩によって後押しされています。中国、日本、韓国などの国々は自動車の電動化に多額の投資を行っており、自動車メーカーはエネルギー管理と性能を強化するために集中制御システムの統合を促しています。税制上の優遇措置、排出削減義務、スマート・モビリティ・インフラへの投資が、この地域でのCVC技術の採用をさらに加速させています。インテリジェントな輸送ソリューションへの注目が高まる中、アジア太平洋地域は世界の中央車両コントローラー市場におけるリーダーシップを維持すると予想されます。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場スコープと定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- 部品メーカー

- メーカー

- 流通業者

- エンドユーザー

- 利益率分析

- 技術革新の状況

- 特許分析

- 規制状況

- コスト分析

- ADAS(先進運転支援システム)の進化

- 影響要因

- 促進要因

- ADAS(先進運転支援システム)の需要増加

- 電気自動車およびハイブリッド車の採用増加

- 自動車の安全性と規制遵守の重視の高まり

- コネクティビティとスマート車両機能の統合への注目の高まり

- 業界の潜在的リスク&課題

- システム開発コストの高さ

- CVCシステムと既存の自動車プラットフォームとの統合の複雑さ

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ハードウェア

- マイクロコントローラー

- メモリーユニット

- 通信モジュール

- コントローラ・エリア・ネットワーク(CAN)

- ローカル相互接続ネットワーク(LIN)

- フレックスレイ

- イーサネット

- その他

- ソフトウェア

- オペレーティング・システム

- ミドルウェア

- アプリケーションソフトウェア

第6章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV

- 商用車

- 小型商用車(LCV)

- 大型商用車(HCV)

第7章 市場推計・予測:推進力別、2021年~2034年

- 主要動向

- ICE

- 電気自動車

- バッテリー電気自動車(BEV)

- プラグインハイブリッド車(PHEV)

- ハイブリッド電気自動車(HEV)

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- ADASと安全システム

- ボディコントロール&コンフォートシステム

- パワートレイン・マネジメント

- インフォテインメントシステム

- ビークルダイナミクス&コントロール

- その他

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- Aptiv

- Bosch

- Continental

- Denso

- Ford Motors

- General Motors

- Hyundai Motors

- Infineon Technologies

- Magna International

- NVIDIA

- NXP Semiconductors

- Qualcomm

- Renesas Electronics

- STMicroelectronics

- Tesla

- Texas Instruments

- Toyota Motor

- Valeo

- Volkswagen

- ZF Friedrichshafen

目次

The Global Central Vehicle Controller Market was valued at USD 13.6 billion in 2024 and is poised to expand at a CAGR of 9.7% between 2025 and 2034, driven by the increasing adoption of electric vehicles (EVs) and the growing need for advanced vehicle control systems. As automakers seek innovative solutions to enhance efficiency and reduce hardware complexity, CVCs have emerged as a critical component in modern vehicle architecture. These controllers consolidate multiple vehicle functions into a centralized system, improving energy optimization, real-time data utilization, and overall vehicle performance. By streamlining control operations, CVCs enable manufacturers to integrate intelligent features such as adaptive cruise control, lane-keeping assistance, and autonomous driving capabilities.

With vehicle electrification and connectivity becoming industry priorities, the demand for these advanced controllers continues to surge. Additionally, the rise of smart mobility solutions and software-defined vehicles has further fueled investments in CVC technologies, allowing automakers to enhance performance, safety, and sustainability. As regulatory pressures for lower emissions and enhanced vehicle efficiency grow, the automotive industry is actively transitioning toward centralized control architectures that offer superior functionality, reduced costs, and seamless integration with evolving mobility ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $13.6 Billion |

| Forecast Value | $33.9 Billion |

| CAGR | 9.7% |

The market is segmented into hardware and software components, with the hardware segment dominating in 2024 at USD 9 billion. The rapid expansion of this segment is attributed to the rising demand for high-performance computing systems that support centralized vehicle control. These hardware solutions play a crucial role in enabling sophisticated vehicle functionalities, including real-time navigation, automated braking, and predictive maintenance. With the increasing production of EVs and the push for advanced driver assistance systems (ADAS), automakers are investing heavily in energy-efficient hardware solutions that enhance vehicle intelligence and responsiveness. As automotive technology advances, the integration of powerful processors, advanced sensors, and artificial intelligence-based control systems is expected to drive further growth in this segment.

By end-use, the market is categorized into original equipment manufacturers (OEMs) and the aftermarket, with OEMs leading the segment. The OEM market is projected to expand at a CAGR of 8.5% from 2025 to 2034, driven by automakers' shift toward centralized vehicle architectures. These systems allow manufacturers to streamline production processes, reduce hardware redundancy, and enhance vehicle efficiency. The integration of CVCs enables automakers to meet stringent regulatory standards related to emissions, cybersecurity, and vehicle safety. As vehicles become more software-centric, OEMs are prioritizing the adoption of these systems to improve connectivity, reduce maintenance costs, and future-proof their vehicle designs.

Asia Pacific remains the largest regional market, accounting for 40% of the global share in 2024. The region's dominance is fueled by the rising adoption of EVs, strong government incentives, and significant advancements in automotive technology. Countries such as China, Japan, and South Korea are investing heavily in vehicle electrification, prompting automakers to integrate centralized control systems for enhanced energy management and performance. Tax benefits, emission reduction mandates, and investments in smart mobility infrastructure further accelerate the adoption of CVC technologies in the region. With a growing focus on intelligent transportation solutions, Asia Pacific is expected to maintain its leadership in the global central vehicle controller market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Component providers

- 3.2.2 Manufacturers

- 3.2.3 Distributors

- 3.2.4 End users

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Regulatory landscape

- 3.7 Cost analysis

- 3.8 Evolution of Advanced Driver Assistance Systems (ADAS)

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing demand for Advanced Driver Assistance Systems (ADAS)

- 3.9.1.2 Rising adoption of electric and hybrid vehicles

- 3.9.1.3 Growing emphasis on vehicle safety and regulatory compliance

- 3.9.1.4 Enhanced focus on connectivity and integration of smart vehicle features

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High cost of system development

- 3.9.2.2 Integration complexity of CVC systems with existing automotive platforms

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Microcontroller

- 5.2.2 Memory unit

- 5.2.3 Communication module

- 5.2.3.1 Controller Area Network (CAN)

- 5.2.3.2 Local Interconnect Network (LIN)

- 5.2.3.3 FlexRay

- 5.2.3.4 Ethernet

- 5.2.4 Others

- 5.3 Software

- 5.3.1 Operating system

- 5.3.2 Middleware

- 5.3.3 Application software

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light Commercial Vehicles (LCV)

- 6.3.2 Heavy Commercial Vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 ICE

- 7.3 Electric vehicles

- 7.3.1 Battery Electric Vehicles (BEV)

- 7.3.2 Plug-in Hybrid Electric Vehicles (PHEV)

- 7.3.3 Hybrid Electric Vehicles (HEV)

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 ADAS & safety system

- 8.3 Body control & comfort system

- 8.4 Powertrain management

- 8.5 Infotainment system

- 8.6 Vehicle dynamics and control

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Aptiv

- 11.2 Bosch

- 11.3 Continental

- 11.4 Denso

- 11.5 Ford Motors

- 11.6 General Motors

- 11.7 Hyundai Motors

- 11.8 Infineon Technologies

- 11.9 Magna International

- 11.10 NVIDIA

- 11.11 NXP Semiconductors

- 11.12 Qualcomm

- 11.13 Renesas Electronics

- 11.14 STMicroelectronics

- 11.15 Tesla

- 11.16 Texas Instruments

- 11.17 Toyota Motor

- 11.18 Valeo

- 11.19 Volkswagen

- 11.20 ZF Friedrichshafen

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 175 Pages

- 納期

- 2~3営業日