|

市場調査レポート

商品コード

1684684

船舶用トランスデューサー市場の機会、成長促進要因、産業動向分析、2025年~2034年予測Marine Transducers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 船舶用トランスデューサー市場の機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年01月14日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

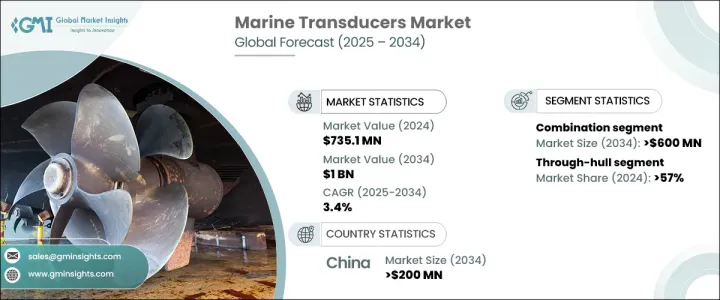

世界の船舶用トランスデューサー市場は、2024年に7億3,510万米ドルと評価され、2025年から2034年にかけて3.4%のCAGRが見込まれます。

この成長の主な要因は、ソナーおよびイメージング技術の急速な進歩であり、水中可視化の精度、鮮明度、有効性を高め続けています。CHIRPソナーやサイドスキャンソナーなどの最先端の技術革新は水中画像に革命をもたらし、ナビゲーション、漁業、海洋調査をより正確で効率的なものにしています。

高解像度ソナーシステムの需要が高まるにつれ、船舶用トランスデューサーに依存する業界は、業務を改善するために洗練されたソリューションを採用しています。商業漁業、海軍防衛、海洋調査におけるリアルタイムデータのニーズの高まりは、市場拡大をさらに促進しています。さらに、ソナー技術へのAIと機械学習の統合は検出能力を向上させ、無線接続とスマート機能は船舶用トランスデューサーをより使いやすくしています。これらの要因が総合的に、先進的な船舶用トランスデューサーの採用拡大に寄与し、現代の海洋アプリケーションにおける役割を確固たるものにしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 7億3,510万米ドル |

| 予測金額 | 10億米ドル |

| CAGR | 3.4% |

市場はタイプ別に区分され、主なカテゴリーには温度変換器、深度変換器、速度変換器、コンビネーション・トランスデューサーが含まれます。2024年には、コンビネーション・トランスデューサーが60%のシェアを占め、市場をリードします。このセグメントは、深度測定、魚検出、水中イメージングを1つのデバイスに統合した多機能性により、2034年までに6億米ドルを創出すると予測されています。複数の機能を1つのトランスデューサに統合できるため、コストとスペースが大幅に削減され、小型船や商業漁業用途に非常に好まれます。また、効率とスペースの最適化が重要な軍事・研究分野でもコンビネーション・トランスデューサーの需要が高まっています。

設置方法別では、船体貫通型、船体内型、トランサムマウント型に分類されます。2024年には、船体貫通型トランスデューサが、その卓越した耐久性と過酷な海洋環境で効率的に機能する能力により、57%のシェアを占めました。水面下に設置されるこれらのトランスデューサは、水深と水温の高精度の測定値を提供し、厳しい条件下では他の選択肢を凌駕します。商業漁業、海洋探査、海軍の用途で広く使用されているため、需要が増え続けています。メーカー各社はまた、長寿命と性能を向上させるために先進的な素材やコーティングを開発しており、船体貫通型トランスデューサはプロ用および産業用アプリケーションに好まれる選択肢となっています。

中国は船舶用トランスデューサー市場で圧倒的な強さを維持しており、2024年には世界売上高の45%を占めています。2034年までに、同国市場は2億米ドルを生み出すと予測されています。海洋エレクトロニクスと造船の世界的リーダーとして、中国は船舶用トランスデューサー製造の革新と効率化を推進し続けています。整備された海軍インフラ、拡大する海運産業、海洋研究開発への投資の増加が成長を促す主な要因となっています。漁船団の近代化と海上安全保障の強化に向けた政府の後押しが、市場の拡大をさらに後押ししています。旺盛な内需と盛んな輸出市場により、中国は今後10年間、船舶用トランスデューサー生産の最前線に立ち続ける態勢を整えています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- 利益率分析

- 価格分析

- 特許状況

- コスト内訳

- 技術革新の状況

- 主要ニュース&イニシアチブ

- 規制状況

- 影響要因

- 促進要因

- ソナーおよび画像技術の進歩

- レクリエーション・ボートとフィッシング活動の成長

- IoTおよびAI対応海洋機器の採用増加

- 商業および防衛海洋アプリケーションの拡大

- 業界の潜在的リスク&課題

- 高度な変換器と設置の高コスト

- 小型船や非商用船での採用が限定的

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 深度変換器

- 速度変換器

- 温度変換器

- コンビネーション・トランスデューサー

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 商業船舶

- レジャーボート

- 漁業

- 海軍防衛

- 海洋エネルギー探査

- 海洋調査

第7章 市場推計・予測:設備別、2021年~2032年

- 主要動向

- スルーハル

- インハル

- トランサムマウント

第8章 市場推計・予測:技術別、2021年~2032年

- 主要動向

- シングルビーム

- マルチビーム

- サイドスキャンソナー

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Airmar

- Benthos

- BioSonics

- EdgeTech

- eSonar

- Furuno

- Garmin

- Hydroacoustic

- Johnson Outdoors

- Kongsberg

- Marport

- Navico

- Phoenix

- SAIYANG

- SEIWA

- Simrad

- Sonotronics

- Teledyne Technologies

- Tritech

- Wesmar

The Global Marine Transducers Market was valued at USD 735.1 million in 2024 and is expected to experience a CAGR of 3.4% between 2025 and 2034. This growth is primarily fueled by rapid advancements in sonar and imaging technologies, which continue to enhance the precision, clarity, and effectiveness of underwater visualizations. Cutting-edge innovations, such as CHIRP and side-scan sonars, are revolutionizing underwater imaging, making navigation, fishing, and marine research more accurate and efficient.

As demand for high-resolution sonar systems increases, industries that rely on marine transducers are adopting sophisticated solutions to improve their operations. The growing need for real-time data in commercial fishing, naval defense, and oceanographic research is further driving market expansion. Additionally, the integration of AI and machine learning into sonar technologies is improving detection capabilities, while wireless connectivity and smart features are making marine transducers more user-friendly. These factors collectively contribute to the increasing adoption of advanced marine transducers, solidifying their role in modern marine applications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $735.1 Million |

| Forecast Value | $1 Billion |

| CAGR | 3.4% |

The market is segmented by type, with key categories including temperature transducers, depth transducers, speed transducers, and combination transducers. In 2024, combination transducers led the market with a commanding 60% share. This segment is anticipated to generate USD 600 million by 2034, thanks to its multifunctional capabilities that integrate depth measurement, fish detection, and underwater imaging into a single device. The ability to consolidate multiple functionalities into one transducer significantly reduces costs and space requirements, making them highly preferred for smaller vessels and commercial fishing applications. The demand for combination transducers is also increasing in military and research sectors, where efficiency and space optimization are critical.

By installation method, the market is categorized into through-hull, in-hull, and transom-mount transducers. In 2024, through-hull transducers dominated with a 57% share due to their exceptional durability and ability to function efficiently in harsh marine environments. These transducers, installed beneath the water surface, provide highly accurate readings for depth and temperature, outperforming alternative options in challenging conditions. Their widespread use in commercial fishing, offshore exploration, and naval applications continues to bolster their demand. Manufacturers are also developing advanced materials and coatings to enhance longevity and performance, making through-hull transducers a preferred choice for professional and industrial applications.

China remains a dominant force in the marine transducers market, accounting for 45% of global sales in 2024. By 2034, the country's market is projected to generate USD 200 million. As a global leader in marine electronics and shipbuilding, China continues to drive innovation and efficiency in marine transducer manufacturing. The nation's well-developed naval infrastructure, expanding shipping industry, and increasing investments in marine research and development are key factors fueling growth. Government-backed initiatives to modernize fishing fleets and enhance maritime security further support market expansion. With strong domestic demand and a thriving export market, China is poised to remain at the forefront of marine transducer production in the coming decade.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.2 Pricing analysis

- 3.3 Patent landscape

- 3.4 Cost breakdown

- 3.5 Technology & innovation landscape

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Advancements in sonar and imaging technologies

- 3.8.1.2 Growth in recreational boating and fishing activities

- 3.8.1.3 Increasing adoption of IoT and AI-enabled marine devices

- 3.8.1.4 Expansion of commercial and defense marine applications

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High cost of advanced transducers and installation

- 3.8.2.2 Limited adoption in small and non-commercial vessels

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Depth transducers

- 5.3 Speed transducers

- 5.4 Temperature transducers

- 5.5 Combination transducers

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Commercial shipping

- 6.3 Recreational boating

- 6.4 Fisheries

- 6.5 Naval defense

- 6.6 Offshore energy exploration

- 6.7 Oceanographic research

Chapter 7 Market Estimates & Forecast, By Installation, 2021 - 2032 ($Bn, Units)

- 7.1 Key trends

- 7.2 Through-hull

- 7.3 In-hull

- 7.4 Transom-mount

Chapter 8 Market Estimates & Forecast, By Technology, 2021 - 2032 ($Bn, Units)

- 8.1 Key trends

- 8.2 Single beam

- 8.3 Multi-beam

- 8.4 Side-scan sonar

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Airmar

- 10.2 Benthos

- 10.3 BioSonics

- 10.4 EdgeTech

- 10.5 eSonar

- 10.6 Furuno

- 10.7 Garmin

- 10.8 Hydroacoustic

- 10.9 Johnson Outdoors

- 10.10 Kongsberg

- 10.11 Marport

- 10.12 Navico

- 10.13 Phoenix

- 10.14 SAIYANG

- 10.15 SEIWA

- 10.16 Simrad

- 10.17 Sonotronics

- 10.18 Teledyne Technologies

- 10.19 Tritech

- 10.20 Wesmar