|

市場調査レポート

商品コード

1684679

十二指腸内視鏡市場の機会、成長促進要因、産業動向分析、2025年~2034年予測Duodenoscopes Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 十二指腸内視鏡市場の機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年01月13日

発行: Global Market Insights Inc.

ページ情報: 英文 140 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

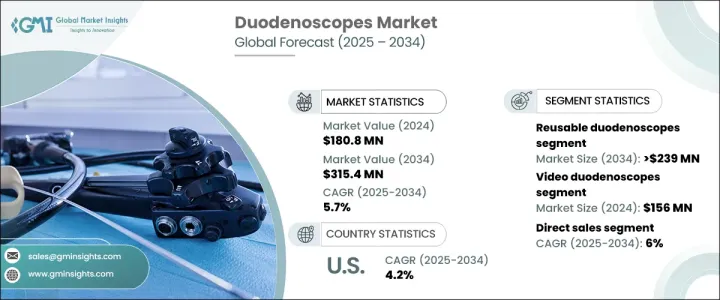

世界の十二指腸内視鏡市場は、2024年に1億8,080万米ドルと評価され、2025年から2034年にかけてCAGR 5.7%で拡大すると予測されています。

この成長軌道は、低侵襲処置に対する需要の急増と消化器ヘルスケアの進歩を反映しています。十二指腸内視鏡は、広範な消化管および肝胆膵疾患の診断と治療において重要な役割を果たしています。ステント留置、結石除去、狭窄管理などの治療介入に使用されることで、これらの機器は現代のヘルスケアに不可欠なものとなっています。十二指腸内視鏡の普及をさらに後押ししているのが、感染管理の重視の高まりと技術の進歩です。さらに、世界の高齢化、消化器系疾患への罹患率の高さが、効果的な診断ツールへの需要に拍車をかけ続け、市場の上昇傾向を確固たるものにしています。

同市場は、再使用型十二指腸内視鏡と単回使用型十二指腸内視鏡に分けられ、再使用型が大きな成長を占めています。再利用型十二指腸内視鏡セグメントはCAGR 5.5%で成長し、2034年には2億3,900万米ドルに達すると予測されています。再利用可能な十二指腸内視鏡は、その費用対効果と大量生産環境への適応性により、病院や診療所で好まれています。これらのデバイスは、徹底的な洗浄のために設計された取り外し可能なコンポーネントを備えており、交差汚染のリスクを最小限に抑え、長期使用のための魅力を高めています。そのため、安全性と効率性を維持しながら処置コストを削減することに重点を置くヘルスケアプロバイダーにとって理想的なソリューションとなっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 1億8,080万米ドル |

| 予測金額 | 3億1,540万米ドル |

| CAGR | 5.7% |

十二指腸内視鏡には、ビデオ十二指腸内視鏡と光ファイバー十二指腸内視鏡の2つのカテゴリーがあります。ビデオ十二指腸内視鏡が市場を独占しており、2024年には1億5,600万米ドルの価値で大きなシェアを占めています。これらの先進的な装置は、比類のない画像品質を提供し、ヘルスケア専門家が消化管問題を正確に診断し、治療することを可能にします。リアルタイムの可視化機能を備えたビデオ十二指腸内視鏡は、処置中の正確な意思決定をサポートします。ナローバンドイメージング(NBI)などの高度な画像技術を統合することで、血管や粘膜の異常の検出を強化します。これらの機能は、従来の外科手術に比べ、回復時間の短縮とリスクの低減を確実にする低侵襲手術において特に有用です。

米国の十二指腸内視鏡市場は、2024年に7,140万米ドルと評価され、2025年から2034年にかけてCAGR 4.2%で成長すると予測されています。この成長の原動力は、消化器疾患の有病率の高さと、高度な診断・治療ツールに対する需要の高まりです。ビデオ十二指腸内視鏡における高精細画像と人工知能の採用は、診断精度を大幅に向上させ、米国ヘルスケア分野での需要をさらに押し上げています。これらの進歩は、処置の効率と患者の転帰を向上させ、十二指腸内視鏡の役割を現代医療に不可欠なものとして確固たるものにしています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 消化器疾患の有病率の増加

- 機器の技術的進歩

- 認知度と診断率の上昇

- 業界の潜在的リスク&課題

- 高コストと厳しい規制要件

- 促進要因

- 成長可能性分析

- 規制状況

- 価格分析

- 償還シナリオ

- 技術展望

- ギャップ分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニング・マトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 再使用型十二指腸内視鏡

- 単回使用十二指腸内視鏡

第6章 市場推計・予測:カテゴリー別、2021年~2034年

- 主要動向

- ビデオ十二指腸内視鏡

- 光ファイバー十二指腸内視鏡

第7章 市場推計・予測:販売チャネル別、2021年~2034年

- 主要動向

- 直販代理店

- 販売代理店

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 外来手術センター

- その他のエンドユーザー

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Ambu

- Boston Scientific

- FUJIFILM

- OLYMPUS

- Ottomed Endoscopy

- PENTAX MEDICAL

- SonoScape

- STORZ

The Global Duodenoscopes Market was valued at USD 180.8 million in 2024 and is projected to expand at a CAGR of 5.7% between 2025 and 2034. This growth trajectory reflects a surge in demand for minimally invasive procedures and advancements in gastrointestinal healthcare. Duodenoscopes play a vital role in diagnosing and treating a wide range of gastrointestinal and hepatopancreaticobiliary conditions. Their use in therapeutic interventions such as stent placements, stone removals, and stricture management has made these devices indispensable in modern healthcare. A growing emphasis on infection control, coupled with technological advancements, is further propelling the adoption of duodenoscopes. Additionally, the aging global population-vulnerable to gastrointestinal disorders-continues to fuel the demand for effective diagnostic tools, cementing the market's upward trend.

The market is divided into reusable and single-use duodenoscopes, with reusable devices accounting for significant growth. The reusable duodenoscope segment is expected to grow at a CAGR of 5.5%, reaching USD 239 million by 2034. Reusable duodenoscopes are a preferred choice for hospitals and clinics due to their cost-effectiveness and adaptability to high-volume settings. These devices feature removable components designed for thorough cleaning, minimizing cross-contamination risks and enhancing their appeal for long-term use. This makes them an ideal solution for healthcare providers focused on maintaining safety and efficiency while reducing procedural costs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $180.8 Million |

| Forecast Value | $315.4 Million |

| CAGR | 5.7% |

Duodenoscopes are available in two categories: video duodenoscopes and fiber optic duodenoscopes. Video duodenoscopes dominate the market, holding a substantial share with a value of USD 156 million in 2024. These advanced devices offer unparalleled imaging quality, enabling healthcare professionals to accurately diagnose and treat gastrointestinal issues. With real-time visualization capabilities, video duodenoscopes support precise decision-making during procedures. Their integration of advanced imaging technologies, such as narrow band imaging (NBI), enhances the detection of vascular and mucosal abnormalities. These features are particularly valuable for minimally invasive procedures, which ensure quicker recovery times and reduced risks compared to traditional surgical methods.

The U.S. duodenoscopes market was valued at USD 71.4 million in 2024 and is set to grow at a CAGR of 4.2% between 2025 and 2034. This growth is driven by a high prevalence of gastrointestinal disorders and a rising demand for advanced diagnostic and therapeutic tools. The adoption of high-definition imaging and artificial intelligence in video duodenoscopes is significantly improving diagnostic accuracy, further boosting demand in the U.S. healthcare sector. These advancements enhance procedural efficiency and patient outcomes, solidifying the role of duodenoscopes as an essential component of modern medical practice.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of gastrointestinal diseases

- 3.2.1.2 Technological advancements in devices

- 3.2.1.3 Rising awareness and diagnosis rates

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost and stringent regulatory requirements

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Pricing analysis

- 3.6 Reimbursement scenario

- 3.7 Technology landscape

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 — 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Reusable duodenoscopes

- 5.3 Single-use duodenoscopes

Chapter 6 Market Estimates and Forecast, By Category, 2021 — 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Video duodenoscopes

- 6.3 Fiber optic duodenoscopes

Chapter 7 Market Estimates and Forecast, By Sales Channel, 2021 — 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Direct sales

- 7.3 Distributors

Chapter 8 Market Estimates and Forecast, By End Use, 2021 — 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Ambulatory surgical centers

- 8.4 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2021 — 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Ambu

- 10.2 Boston Scientific

- 10.3 FUJIFILM

- 10.4 OLYMPUS

- 10.5 Ottomed Endoscopy

- 10.6 PENTAX MEDICAL

- 10.7 SonoScape

- 10.8 STORZ