|

市場調査レポート

商品コード

1892787

眼科用抗VEGF治療薬市場機会、成長要因、業界動向分析、および2025年から2034年までの予測Ophthalmic Anti-VEGF Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 眼科用抗VEGF治療薬市場機会、成長要因、業界動向分析、および2025年から2034年までの予測 |

|

出版日: 2025年12月08日

発行: Global Market Insights Inc.

ページ情報: 英文 142 Pages

納期: 2~3営業日

|

概要

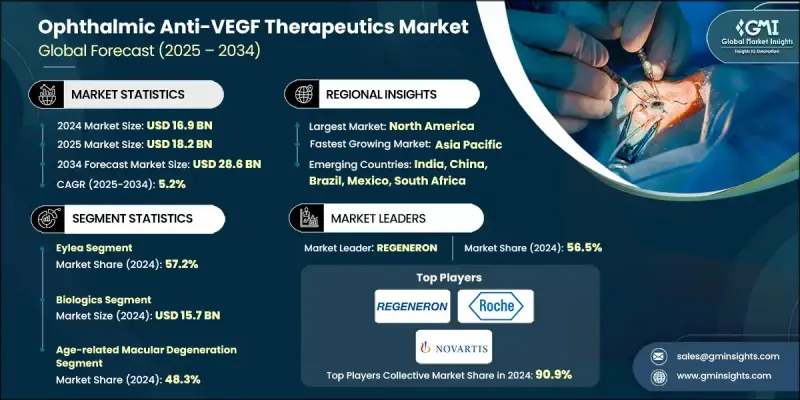

世界の眼科用抗VEGF治療薬市場は、2024年に169億米ドルと評価され、2034年までにCAGR5.2%で成長し、286億米ドルに達すると予測されています。

市場拡大の主な要因としては、網膜疾患の増加、世界の糖尿病患者の増加、継続的な人口の高齢化、そして専門的な眼科施設の急速な整備が挙げられます。抗VEGF薬は、網膜における異常な血管形成に関与するVEGFの活性を阻害することで作用します。このため、加齢黄斑変性(AMD)、糖尿病性黄斑浮腫(DME)、網膜静脈閉塞症(RVO)などの疾患において、これらの治療法は不可欠です。糖尿病網膜症、糖尿病関連黄斑合併症、加齢性視覚変性の症例増加が、治療対象患者の層を拡大し続けています。同時に、継続的な調査努力により、持続性の向上、安全性の強化、複数の経路を標的とする能力を備えた改良分子が生み出されています。これらの革新は、第一選択治療の選択肢拡大、切り替え戦略の最適化、投与間隔の長期化支援を通じて、治療パターンを再構築しています。治療環境が多様化する中、臨床的実績と高齢化・糖尿病患者層における持続的な需要により、プレミアム医薬品カテゴリーは商業的に持続可能な状態を維持しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年度 | 2025-2034 |

| 開始時価値 | 169億米ドル |

| 予測金額 | 286億米ドル |

| CAGR | 5.2% |

アイレアセグメントは、優れた臨床結果、信頼性の高い安全性、および高用量製剤による投与間隔の延長により、2024年に57.2%のシェアを占めました。糖尿病性網膜症におけるその幅広い採用は、世界的に急増する糖尿病患者数によってさらに強化されており、これが長期的な利用と高い年間治療量を継続的に牽引しています。

加齢黄斑変性(AMD)セグメントは2024年に48.3%のシェアを占め、2034年までに132億米ドルに達すると予測されています。AMDは主に高齢者に発症するため、高齢者人口が急速に拡大する市場では治療需要が引き続き増加しています。抗VEGF治療はAMD治療の基盤であり、世界中の高齢化人口において着実な成長をもたらしています。

北米眼科用抗VEGF治療薬市場は、AMD、糖尿病性黄斑浮腫(DME)、糖尿病網膜症の患者基盤が厚いことから、2024年に64.8%のシェアを占めました。同地域は、堅固な臨床インフラ、豊富な専門医の確保、そして継続的な治療遵守を促進する高効率な供給・投与システムという利点を有しています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 眼疾患の増加傾向

- 高齢化人口の増加

- 医薬品開発における技術的進歩

- 眼科疾患の適時治療に対する意識の高まり

- 業界の潜在的リスク&課題

- 治療費の高騰

- 副作用と安全性に関する懸念

- 市場機会

- バイオシミラー及び低コスト代替品の普及拡大

- 医療アクセスが拡大する新興市場への進出

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- 技術動向

- 現在の技術動向

- 新興技術

- 将来の市場動向

- パイプライン分析

- 価格分析、2024

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- 世界

- 北米

- 欧州

- アジア太平洋地域

- 競合ポジショニングマトリックス

- 主要市場企業の競合分析

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 拡大計画

第5章 市場推計・予測:抗VEGF療法別、2021-2034

- 主要動向

- アイリーア

- ヴァビスモ

- ルーセンティス

- その他の抗VEGF療法

第6章 市場推計・予測:薬剤タイプ別、2021-2034

- 主要動向

- 生物学的製剤

- バイオシミラー

第7章 市場推計・予測:適応症別、2021-2034

- 主要動向

- 加齢黄斑変性

- 糖尿病網膜症

- 黄斑浮腫

- 網膜静脈閉塞症

- 近視性脈絡膜新生血管

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- AMGEN

- Astellas

- Biocon Biologics

- Biogen

- CELLTRION

- Intas Pharmaceuticals

- KANGHONG PHARMACEUTICALS

- LUPIN

- NOVARTIS

- REGENERON

- Reliance Life Sciences

- Roche

- SANDOZ

- STADA

- teva