|

市場調査レポート

商品コード

1684559

抗凝固剤逆転薬の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Anticoagulant Reversal Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 抗凝固剤逆転薬の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年01月06日

発行: Global Market Insights Inc.

ページ情報: 英文 135 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

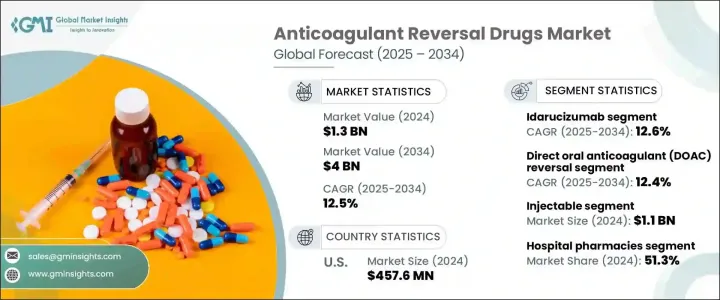

抗凝固剤逆転薬の世界市場は2024年に13億米ドルと評価され、2025年から2034年にかけてCAGR12.5%で予測され、目覚ましい成長を遂げようとしています。

この市場拡大は、抗凝固剤の使用量の増加と出血性合併症の発生率の上昇に大きく後押しされており、効果的な逆転薬の必要性が強調されています。深部静脈血栓症、肺塞栓症、心房細動などの心血管疾患や血栓性疾患が増加の一途をたどる中、緊急時に抗凝固作用を速やかに逆転させる薬剤の需要も高まっています。直接経口抗凝固剤(DOAC)、ワルファリン、ヘパリンに対する新たな逆転薬の導入により、治療の状況は一変し、患者にとってもヘルスケアプロバイダーにとっても、より信頼性が高く、利用しやすいものとなっています。

世界の高齢化と慢性疾患の増加により、抗凝固剤の使用量は大幅に増加しています。現在、長期抗凝固療法は、さまざまな心血管疾患や血栓性疾患に対する一般的な治療法となっています。しかし,これらの治療は出血性合併症のリスクを増大させるため、信頼性の高い抗凝固剤逆転オプションの必要性が生じています。抗凝固剤逆転薬はこの課題に対処し、重篤な出血や手術などの有害事象の際に患者の安全を確保します。医療技術の進歩により、より効果的で迅速な逆転治療薬の開発が進むにつれ、市場はさらなる成長を遂げ、臨床と病院の両方でこれらの治療薬が広く採用されるようになります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 13億米ドル |

| 予測金額 | 40億米ドル |

| CAGR | 12.5% |

市場は製品タイプ別に区分され、アンデキサネットアルファ、フィトナジオン(ビタミンK)、プロトロンビン複合体濃縮製剤、イダルシズマブ、プロタミン、その他関連製品が含まれます。イダルシズマブは、2024年に4億4,350万米ドルと評価され、ダビガトランの効果を逆転させる役割を担うことから、予測期間中のCAGRは12.6%と予想されています。ダビガトランは、特に心房細動や深部静脈血栓症などの疾患の管理に広く使用されているDOACです。

投与経路に関しては、市場は注射剤と経口剤に分かれます。注射剤セグメントは市場をリードしており、2024年の市場規模は11億米ドルです。こうした即効性のある薬剤は、大出血や緊急手術など、即座の介入が重要な緊急事態における抗凝固療法の再開に不可欠です。

米国では、抗凝固剤逆転薬の市場規模は2024年に4億5,760万米ドルとなりました。心血管疾患や腎疾患など、抗凝固療法を必要とする慢性疾患の罹患率の増加が、抗凝固剤とその逆転薬の両方の需要を押し上げています。さらに、より安全性の高い抗凝固剤やその逆剤の開発を奨励する規制当局の支援が、継続的な成長を遂げている米国市場をさらに後押ししています。血栓塞栓症や出血性疾患のリスクを抱える高齢者人口が増加傾向にある米国では、新しい抗凝固剤や逆転療法が導入され、臨床診療に組み込まれるにつれて、市場は持続的な需要が見込まれます。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- 業界への影響要因

- 成長促進要因

- 高齢化人口の増加

- 抗凝固療法を必要とする疾患の有病率の上昇

- 新規抗凝固剤の出現

- 業界の潜在的リスク・課題

- 抗凝固剤に伴う副作用

- 成長促進要因

- 成長可能性分析

- 規制状況

- パイプライン分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- イダルシズマブ

- フィトナジオン(ビタミンK)

- プロトロンビン複合体濃縮製剤

- アンデキサネットアルファ

- プロタミン

- その他の製品

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 直接経口抗凝固剤(DOAC)逆転剤

- ワルファリン逆転

- ヘパリン・低分子ヘパリン(LMWH)戻入剤

- その他の用途

第7章 市場推計・予測:投与経路別、2021年~2034年

- 主要動向

- 注射剤

- 経口剤

第8章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 病院薬局

- 小売薬局

- オンライン薬局

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Amneal Pharmaceuticals

- AstraZeneca

- Cipla

- CSL Behring Limited

- Dr. Reddy’s Laboratories

- Endo International

- Lupin

- Mylan N.V.

- Novartis

- Pfizer

- Sun Pharmaceutical Industries

- Teva Pharmaceutical Industries

The Global Anticoagulant Reversal Drugs Market, valued at USD 1.3 billion in 2024, is set to experience impressive growth, projected at a CAGR of 12.5% from 2025 to 2034. This market expansion is largely driven by the growing usage of anticoagulants and the rising incidence of bleeding complications, which emphasize the need for effective reversal agents. As cardiovascular diseases and thrombotic conditions like deep vein thrombosis, pulmonary embolism, and atrial fibrillation continue to increase, so does the demand for drugs that can quickly reverse anticoagulation effects in emergency situations. With the introduction of novel reversal agents for direct oral anticoagulants (DOACs), warfarin, and heparin, the landscape is transforming, making treatment more reliable and accessible for both patients and healthcare providers.

Aging populations worldwide, coupled with an increasing prevalence of chronic conditions, have significantly amplified the use of anticoagulants. Long-term anticoagulation therapy is now a common treatment for a variety of cardiovascular and thrombotic diseases. However, these treatments increase the risk of bleeding complications, creating a critical need for reliable reversal options. Anticoagulant reversal drugs address this challenge, ensuring patient safety during adverse events like severe bleeding or surgeries. As advancements in medical technology drive the development of more effective and rapid reversal therapies, the market is poised for further growth, benefiting from the wider adoption of these treatments in both clinical and hospital settings.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.3 Billion |

| Forecast Value | $4 Billion |

| CAGR | 12.5% |

The market is segmented by product type, which includes andexanet alfa, phytonadione (vitamin K), prothrombin complex concentrates, idarucizumab, protamine, and other related products. Idarucizumab, valued at USD 443.5 million in 2024, is anticipated to experience a CAGR of 12.6% during the forecast period, driven by its role in reversing the effects of dabigatran. Dabigatran is a widely used DOAC, particularly for managing conditions such as atrial fibrillation and deep venous thrombosis.

When it comes to the route of administration, the market is split into injectable and oral forms. The injectable segment leads the market, valued at USD 1.1 billion in 2024, as injectables are preferred in critical situations for their quick and effective action. These fast-acting drugs are essential for reversing anticoagulation during emergencies like severe bleeding or urgent surgeries, where immediate intervention is crucial.

In the U.S., the anticoagulant reversal drugs market was valued at USD 457.6 million in 2024. The increasing incidence of chronic conditions requiring anticoagulation therapy, such as cardiovascular and kidney diseases, has driven the demand for both anticoagulants and their reversal agents. Furthermore, regulatory support that encourages the development of safer anticoagulants and reversal therapies further boosts the U.S. market, which is experiencing continued growth. With a large and growing elderly population at risk for thromboembolic and bleeding disorders, the U.S. market is expected to see sustained demand as new reversal drugs and therapies are introduced and incorporated into clinical practices.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing aging population

- 3.2.1.2 Rising prevalence of conditions requiring anticoagulation therapy

- 3.2.1.3 Emergence of new anticoagulants

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Side effects associated with these drugs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Pipeline analysis

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Idarucizumab

- 5.3 Phytonadione (Vitamin K)

- 5.4 Prothrombin complex concentrates

- 5.5 Andexanet alfa

- 5.6 Protamine

- 5.7 Other products

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Direct oral anticoagulant (DOAC) reversal

- 6.3 Warfarin reversal

- 6.4 Heparin and low-molecular-weight heparin (LMWH) reversal

- 6.5 Other applications

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Injectable

- 7.3 Oral

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 Online pharmacies

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Amneal Pharmaceuticals

- 10.2 AstraZeneca

- 10.3 Cipla

- 10.4 CSL Behring Limited

- 10.5 Dr. Reddy’s Laboratories

- 10.6 Endo International

- 10.7 Lupin

- 10.8 Mylan N.V.

- 10.9 Novartis

- 10.10 Pfizer

- 10.11 Sun Pharmaceutical Industries

- 10.12 Teva Pharmaceutical Industries