|

市場調査レポート

商品コード

1684558

カルシニューリン阻害剤の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Calcineurin Inhibitors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| カルシニューリン阻害剤の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年01月03日

発行: Global Market Insights Inc.

ページ情報: 英文 135 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

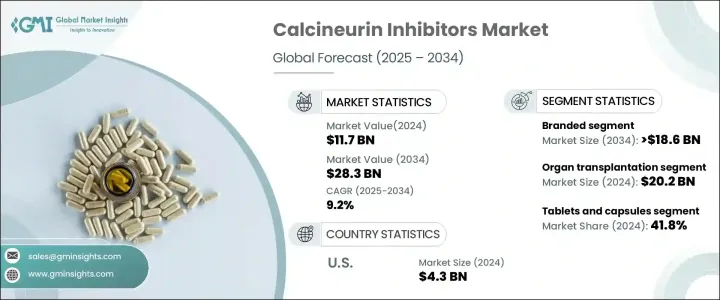

カルシニューリン阻害剤の世界市場は、2024年に117億米ドルと評価され、2025年から2034年にかけてCAGR9.2%で拡大すると予測されています。

この市場成長の主な要因は、自己免疫疾患の有病率の増加と、世界の臓器移植件数の増加です。カルシニューリン阻害剤は、臓器拒絶反応を防ぐために免疫系を抑制するため、特に腎臓、肝臓、心臓、肺移植などの需要の高い手術において、移植医療に不可欠です。移植を成功させるためにこれらの薬剤が果たす重要な役割は、その採用を促進し続け、市場の需要を高めています。世界のヘルスケアの進展に伴い、高齢化や臓器不全の発生率の上昇などの要因により、臓器移植を必要とする人の数が増加しているため、免疫抑制剤の需要はさらに高まっています。

カルシニューリン阻害剤市場において、競合はブランド品とジェネリック医薬品に区分されます。市場の大部分を占めるブランド品セグメントは、9%の成長率でリードすると予測されています。2034年には186億米ドルに達すると予想されています。ブランド品のカルシニューリン阻害剤は、その実証された有効性、強力な安全性プロファイル、臨床試験データによる確かな裏付けから、医療従事者の間で依然として好ましい選択肢となっています。これらの製品は厳格な品質基準を満たすように製造されており、一貫性と信頼性を確保しています。そのため、臓器拒絶反応のリスクを最小限に抑えられるかどうかが成功の鍵を握る、重要な移植プロトコールにおいて、これらの薬剤は最適な選択肢となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 117億米ドル |

| 予測金額 | 283億米ドル |

| CAGR | 9.2% |

カルシニューリン阻害剤は、主に臓器移植、自己免疫疾患、その他の特殊用途の3つの分野で利用されています。臓器移植の分野では、2025年から2034年の間に202億米ドルの売上が見込まれており、移植後のケアにおいてこれらの薬剤が中心的な役割を果たしていることを裏付けています。身体の免疫反応を効果的に管理するその能力は、移植臓器の生存を確実にし、世界中の移植医療において不可欠なものとなっています。免疫抑制療法が依然として臓器拒絶反応の予防の要であるため、カルシニューリン阻害剤はこの分野で優位を占めています。

米国では、カルシニューリン阻害剤市場は2024年に43億米ドルとなり、2025年から2034年にかけてCAGR8.4%で成長すると予測されています。米国はこれらの薬剤の主な市場であり、世界有数の移植センターの存在、強力な償還政策、研究開発への旺盛な投資が市場を牽引しています。さらに、糖尿病や高血圧などの慢性疾患の罹患率が高く、臓器不全につながることが多いため、カルシニューリン阻害剤の需要がさらに高まっています。これらの要因から、米国は世界市場で圧倒的な強さを誇り、この分野での継続的な成長と技術革新を確実なものにしています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- 業界への影響要因

- 成長促進要因

- 臓器移植件数の増加

- 自己免疫疾患の増加

- 免疫抑制剤の研究開発の急増

- 業界の潜在的リスク・課題

- 副作用と代替治療の利用可能性

- 成長促進要因

- 成長可能性分析

- 規制状況

- 技術情勢

- 償還シナリオ

- パイプライン分析

- ポーター分析

- PESTEL分析

- 今後の市場動向

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業市場シェア分析

- 主要市場企業の競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- ブランド

- タクロリムス

- シクロスポリン

- その他のブランド製品

- ジェネリック

- タクロリムス

- シクロスポリン

- その他のジェネリック医薬品

第6章 市場推計・予測:用量別、2021年~2034年

- 主要動向

- 錠剤・カプセル剤

- 軟膏剤

- 注射剤

- その他の剤形

第7章 市場推計・予測:適応症別、2021年~2034年

- 主要動向

- 臓器移植

- 自己免疫疾患

- その他の適応症

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- abbvie

- astellas

- Aurinia

- Biocon

- Dr. Reddy’s

- Glenmark

- LUPIN

- Novartis

- Roche

- VIATRIS

The Global Calcineurin Inhibitors Market, valued at USD 11.7 billion in 2024, is projected to expand at a CAGR of 9.2% from 2025 to 2034. This market growth is primarily fueled by the increasing prevalence of autoimmune disorders and the rising number of organ transplants across the globe. Calcineurin inhibitors are essential in transplant medicine, as they suppress the immune system to prevent organ rejection, particularly in high-demand procedures such as kidney, liver, heart, and lung transplants. The critical role these medications play in ensuring transplant success continues to drive their adoption, thus enhancing their market demand. As the global healthcare landscape evolves, the increasing number of individuals requiring organ transplants-due to factors like aging populations and the rising incidence of organ failure-has further solidified the demand for these immunosuppressive drugs.

Within the calcineurin inhibitors market, the competition is segmented into branded and generic options. The branded segment, accounting for a significant portion of the market, is anticipated to lead with a growth rate of 9%. By 2034, it is expected to reach USD 18.6 billion. Branded calcineurin inhibitors remain the preferred choice among healthcare professionals because of their proven efficacy, strong safety profiles, and solid backing from clinical trial data. These products are manufactured to meet rigorous quality standards, ensuring consistency and reliability. This makes them the go-to option in critical transplant protocols, where success depends on minimizing the risk of organ rejection.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $11.7 Billion |

| Forecast Value | $28.3 Billion |

| CAGR | 9.2% |

Calcineurin inhibitors are utilized primarily in three areas: organ transplantation, autoimmune diseases, and other specialized applications. The organ transplantation segment is expected to generate USD 20.2 billion between 2025 and 2034, underlining the central role of these drugs in post-transplant care. Their ability to manage the body's immune response effectively ensures the survival of transplanted organs, making them indispensable in transplant medicine worldwide. As immunosuppressive therapy remains the cornerstone of preventing organ rejection, calcineurin inhibitors continue to dominate this segment.

In the United States, the calcineurin inhibitors market, valued at USD 4.3 billion in 2024, is projected to grow at a CAGR of 8.4% from 2025 to 2034. The U.S. is a key market for these medications, with the presence of world-leading transplant centers, strong reimbursement policies, and a robust investment in research and development driving the market forward. Moreover, the high rates of chronic conditions such as diabetes and hypertension, which often lead to organ failure, further amplify the demand for calcineurin inhibitors. These factors position the U.S. as a dominant force in the global market, ensuring continued growth and innovation within the sector.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing number of organ transplant procedures

- 3.2.1.2 Rising prevalence of autoimmune diseases

- 3.2.1.3 Surge in immunosuppressive research and development activities

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Side effects and the availability of alternative treatments

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Reimbursement scenario

- 3.7 Pipeline analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Future market trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Branded

- 5.2.1 Tacrolimus

- 5.2.2 Cyclosporine

- 5.2.3 Other branded products

- 5.3 Generic

- 5.3.1 Tacrolimus

- 5.3.2 Cyclosporine

- 5.3.3 Other generic products

Chapter 6 Market Estimates and Forecast, By Dosage, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Tablets and capsules

- 6.3 Ointments

- 6.4 Injections

- 6.5 Other dosage forms

Chapter 7 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Organ transplantation

- 7.3 Autoimmune disease

- 7.4 Other indications

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 abbvie

- 9.2 astellas

- 9.3 Aurinia

- 9.4 Biocon

- 9.5 Dr. Reddy’s

- 9.6 Glenmark

- 9.7 LUPIN

- 9.8 Novartis

- 9.9 Roche

- 9.10 VIATRIS