固体レーザー市場の機会、成長促進要因、産業動向分析、2025~2034年予測

Solid-State Laser Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日

- 商品コード

- 1684549

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

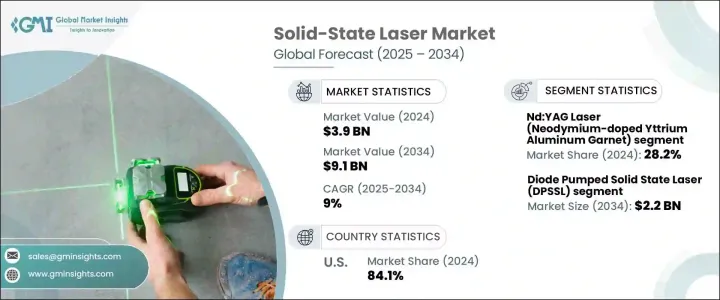

世界の固体レーザー市場は急速な成長を遂げており、2024年の評価額は39億米ドル、2025年から2034年までのCAGRは9%と予測されています。

この目覚しい拡大は、特に小型化、エネルギー効率、性能向上の分野における画期的な技術進歩によるものです。研究者は常にレーザ能力の限界を押し広げようと努力しており、出力の増大、レーザーサイズの縮小、精度の向上に注力しています。

このような進歩により、ヘルスケア、通信、製造業など様々な業界において、より高性能で費用対効果の高いソリューションが期待され、数多くの新しいアプリケーションが誕生しています。固体レーザーの技術革新は、高品質で信頼性の高いレーザを低コストで製造することを可能にするだけでなく、これまで未開発であった市場での使用範囲を拡大しています。その結果、固体レーザーの需要は、その多用途性と最先端のアプリケーションに牽引され、急な上昇軌道に乗っています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 39億米ドル |

| 予測金額 | 91億米ドル |

| CAGR | 9% |

固体レーザーは、従来のレーザ技術と比較して、加工速度の高速化、高精度化、材料廃棄量の削減など、幅広いメリットを提供します。産業界が自動化と高品質生産基準の必要性に焦点を当て続ける中、製造業における固体レーザーの需要は増加傾向にあります。このように、より精密で効率的な生産プロセスへのニーズが高まっていることが、市場の急成長に寄与している主な要因の1つです。さらに、これらのレーザのコスト効率の良さは、性能の向上とともに、日進月歩のマーケットプレースで競争力を維持しようとする企業にとって非常に魅力的なものとなっています。

材料タイプでは、Nd:YAGレーザ(ネオジムドープイットリウムアルミニウムガーネット)、Er:YAGレーザ(エルビウムドープイットリウムアルミニウムガーネット)、アレキサンドライトレーザ、Ti:Sapphireレーザ(チタンドープサファイア)、その他など様々なカテゴリに市場は細分化されます。2024年現在、Nd:YAGレーザセグメントが市場シェアの28.2%を占め、圧倒的な強さを誇っています。これらのレーザーは、連続波モードとパルスモードの両方で動作できる汎用性の高さと、1064nmの有効波長が材料への深い浸透に理想的であることから支持されています。

技術面では、市場はダイオード励起固体レーザー(DPSSL)、ファイバーレーザー、ディスクレーザー、薄板レーザー、光励起半導体レーザー(OPSL)などのセグメントに分けられます。このうち、DPSSLは、2034年までに22億米ドルの推定値に達し、主要技術になると予想されています。高効率、コンパクト設計、安定性で知られるDPSSLは、精密で信頼性の高いレーザビームを必要とする産業でますます求められています。

米国の固体レーザー市場は、世界市場の大部分を占めており、2024年には84.1%という驚異的なシェアを占めています。この優位性は、ヘルスケア、航空宇宙、防衛分野で固体レーザーが広く採用されていることが背景にあります。この国の盛んな研究開発エコシステムは、最先端技術への政府の多額の投資と相まって、この分野の継続的な技術革新に拍車をかけています。さらに、自動車やエレクトロニクスなどの産業における精密製造需要の高まりが、世界の固体レーザー市場における米国の主導的地位をさらに強化しています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 1次データ

- 2次データ

- 有料情報源

- 公的情報源

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 破壊

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 促進要因

- 技術の進歩と小型化

- レーザーによる製造・加工需要の増加

- 医療・ヘルスケア用途の急増

- 通信システムにおけるアプリケーションの増加

- 業界の潜在的リスク&課題

- 高い初期コストと複雑な統合

- 代替技術との競合

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:素材別、2021年~2034年

- 主要動向

- Nd:YAGレーザー(ネオジム添加イットリウム・アルミニウム・ガーネット)

- Er:YAGレーザー(エルビウム添加イットリウム・アルミニウム・ガーネット)

- アレキサンドライトレーザー

- Ti:Sapphireレーザー(チタンドープサファイア).

- その他

第6章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- ダイオード励起固体レーザー(DPSSL)

- ファイバーレーザー

- ディスクレーザー

- シンスラブレーザー

- 光励起半導体レーザー(OPSL)

- その他

第7章 市場推計・予測:パワーレンジ別、2021年~2034年

- 主要動向

- 低出力(100W未満)

- 中出力(100W~1kW)

- 高出力(1 kW超)

第8章 市場推計・予測:波長帯別、2021年~2034年

- 主要動向

- 紫外線(UV)

- 可視光

- 赤外線(IR)

- 中赤外(MIR)

第9章 市場推計・予測:動作タイプ別、2021-2034年

- 主要動向

- パルス動作

- 常用波動作

第10章 市場推計・予測:用途別、2021-2034年

- 主要動向

- 自動車

- 産業用

- データストレージ

- 医療

- 防衛・航空宇宙

- 通信

- その他

第11章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第12章 企業プロファイル

- ALPHALAS GmbH

- AMS Technologies Ltd.

- Coherent Inc.

- CrystaLaser, LLC

- Daheng New Epoch Technology, Inc.

- Edgewave

- Hamamatsu Photonics K.K.

- IPG Photonics

- Jenoptik Laser GmbH

- JENOPTIK

- Jiangsu Lumispot Technology Co., Ltd.

- Laserglow Technologies

- LASEROPTEK Co., Ltd.

- LUMIBIRD

- Lumentum Operations LLC

- Maxphotonics

- nLight

- Northrop Grumman Corporation

- Photonic Solutions Ltd.

- Quanta System SP

目次

The Global Solid-State Laser Market is experiencing rapid growth, with a valuation of USD 3.9 billion in 2024 and a projected CAGR of 9% from 2025 to 2034. This impressive expansion can be attributed to groundbreaking technological advancements, particularly in the areas of miniaturization, energy efficiency, and performance enhancement. Researchers are constantly working to push the boundaries of laser capabilities, focusing on increasing power output, shrinking laser sizes, and enhancing precision.

These advancements are unlocking a multitude of new applications across various industries, such as healthcare, telecommunications, and manufacturing, as businesses are drawn to the promise of higher performance and cost-effective solutions. Innovations in solid-state lasers are not only enabling the production of high-quality, reliable lasers at a lower cost but also expanding the scope of their use in previously untapped markets. As a result, the demand for solid-state lasers is on a steep upward trajectory, driven by their versatility and cutting-edge applications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.9 Billion |

| Forecast Value | $9.1 Billion |

| CAGR | 9% |

Solid-state lasers offer a wide array of benefits when compared to traditional laser technologies, including faster processing speeds, higher precision, and reduced material waste. As industries continue to focus on automation and the need for high-quality production standards, the demand for solid-state lasers in manufacturing is on the rise. This growing need for more precise and efficient production processes is one of the key factors contributing to the market's rapid growth. Additionally, the cost-effective nature of these lasers, along with their improved performance, makes them highly attractive to businesses looking to stay competitive in an ever-evolving marketplace.

In terms of material type, the market is segmented into various categories, including Nd:YAG lasers (Neodymium-doped Yttrium Aluminum Garnet), Er:YAG lasers (Erbium-doped Yttrium Aluminum Garnet), Alexandrite lasers, Ti:Sapphire lasers (Titanium-doped Sapphire), and others. As of 2024, the Nd:YAG laser segment is the dominant force, accounting for 28.2% of the market share. These lasers are favored for their versatility, being able to operate in both continuous-wave and pulsed modes, and their effective wavelength of 1064 nm, which is ideal for deep material penetration.

On the technology front, the market is divided into segments such as Diode Pumped Solid State Lasers (DPSSL), fiber lasers, disk lasers, thin slab lasers, and Optically Pumped Semiconductor Lasers (OPSL). Of these, DPSSLs are expected to be the leading technology, reaching an estimated value of USD 2.2 billion by 2034. Known for their high efficiency, compact design, and stability, DPSSLs are increasingly sought after by industries that require precise, reliable laser beams for their operations.

The U.S. solid-state laser market commands a significant portion of the global market, holding an impressive 84.1% share in 2024. This dominance is fueled by the widespread adoption of solid-state lasers in healthcare, aerospace, and defense sectors. The country's thriving research and development ecosystem, coupled with substantial government investments in cutting-edge technologies, has spurred continued innovation in the field. Furthermore, the growing demand for precision manufacturing in industries such as automotive and electronics further bolsters the U.S.'s leadership position in the global solid-state laser market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Technological advancements and miniaturization

- 3.6.1.2 Increased demand for laser-based manufacturing and processing

- 3.6.1.3 Surge in medical and healthcare applications

- 3.6.1.4 Rising application in communication systems

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High initial costs and complex integration

- 3.6.2.2 Competition from alternative technologies

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Material, 2021-2034 (USD Billion)

- 5.1 Key trends

- 5.2 Nd:YAG Laser (Neodymium-doped Yttrium Aluminum Garnet)

- 5.3 Er:YAG Laser (Erbium-doped Yttrium Aluminum Garnet)

- 5.4 Alexandrite Laser

- 5.5 Ti:Sapphire Laser (Titanium-doped Sapphire).

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Technology, 2021-2034 (USD Billion)

- 6.1 Key trends

- 6.2 Diode Pumped Solid State Laser (DPSSL)

- 6.3 Fiber laser

- 6.4 Disk laser

- 6.5 Thin slab laser

- 6.6 Optically Pumped Semiconductor Laser (OPSL)

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Power Range, 2021-2034 (USD Billion)

- 7.1 Key trends

- 7.2 Low power (< 100 W)

- 7.3 Medium power (100 W - 1 kW)

- 7.4 High power (> 1 kW)

Chapter 8 Market Estimates & Forecast, By Wavelength Range, 2021-2034 (USD Billion)

- 8.1 Key trends

- 8.2 Ultraviolet (UV)

- 8.3 Visible

- 8.4 Infrared (IR)

- 8.5 Mid-Infrared (MIR)

Chapter 9 Market Estimates & Forecast, By Operation Type, 2021-2034 (USD Billion)

- 9.1 Key trends

- 9.2 Pulsed operation

- 9.3 Continuous wave operation

Chapter 10 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion)

- 10.1 Key trends

- 10.2 Automotive

- 10.3 Industrial

- 10.4 Data storage

- 10.5 Medical

- 10.6 Defense and aerospace

- 10.7 Telecommunications

- 10.8 Others

Chapter 11 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 ALPHALAS GmbH

- 12.2 AMS Technologies Ltd.

- 12.3 Coherent Inc.

- 12.4 CrystaLaser, LLC

- 12.5 Daheng New Epoch Technology, Inc.

- 12.6 Edgewave

- 12.7 Hamamatsu Photonics K.K.

- 12.8 IPG Photonics

- 12.9 Jenoptik Laser GmbH

- 12.10 JENOPTIK

- 12.11 Jiangsu Lumispot Technology Co., Ltd.

- 12.12 Laserglow Technologies

- 12.13 LASEROPTEK Co., Ltd.

- 12.14 LUMIBIRD

- 12.15 Lumentum Operations LLC

- 12.16 Maxphotonics

- 12.17 nLight

- 12.18 Northrop Grumman Corporation

- 12.19 Photonic Solutions Ltd.

- 12.20 Quanta System SP

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日