据置型触媒システム市場の機会、成長促進要因、産業動向分析、2025~2034年の予測

Stationary Catalytic Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日

- 商品コード

- 1667072

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

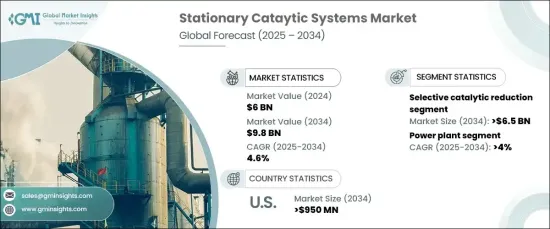

据置型触媒システムの世界市場規模は2024年に60億米ドルとなり、2025年から2034年にかけてCAGR 4.6%で拡大すると予測されています。

この成長の原動力は、エネルギー需要の増加、急速な工業化、エネルギー効率規制の強化です。据置型触媒システムは、窒素酸化物の排出を削減し、クリーンエネルギー目標をサポートする能力から、エネルギー集約型産業でますます使用されるようになっています。セメント生産、発電所、金属加工、製造業などでの採用は、NOxとCO排出の最小化に焦点を当てた政府の義務化によって推進されています。

選択的触媒還元(SCR)分野は、2034年までに65億米ドルを超えると予測され、大きな成長を遂げようとしています。SCR技術は窒素酸化物の削減に非常に効果的で、最大95%のNOx排出削減を達成します。これらのシステムは、アンモニア排出量を許容閾値内に維持しながら、厳しい規制基準を満たすように設計されており、市場の需要を高めています。多様な産業用途に適したコスト効率の高いコンパクトな設計など、SCR技術の絶え間ない進歩が採用をさらに加速しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 60億米ドル |

| 予測金額 | 98億米ドル |

| CAGR | 4.6% |

据置型触媒システムの主要用途は発電所であり、このセグメントは2034年までにCAGR 4%以上で成長すると予想されます。電力需要の増加に伴い、効果的な産業用排出ガス制御の必要性が高まっているため、発電施設ではこれらのシステムを統合することが奨励されています。有害ガスの排出削減を義務付ける規制の枠組みにより、この分野では信頼性の高い排出制御技術の導入が重視されるようになっています。

セメント生産部門も、大気汚染物質のレベル上昇に伴い、排出ガス制御システムの需要を強化しています。厳格なコンプライアンス要件と、排出制限を超過した場合の金銭的罰則のリスクが、SCRや酸化触媒のような技術の重要性を高めています。新興経済諸国では、インフラが拡大し、建設活動が活発化しているため、これらのシステムの大幅な成長が見込まれています。

米国の据置型触媒システム市場は、製造活動の増加と石炭火力発電所からガス火力発電所へのシフトに支えられ、2034年までに9億5,000万米ドルを超えると予測されます。NOxとCOの排出を対象とした環境規制の強化と、これらの汚染物質が環境に与える影響に対する意識の高まりが、市場の成長を強化しています。産業界が進化する環境政策に合わせてよりクリーンな技術を採用するにつれて、据置型触媒システムの需要は大幅に増加するとみられます。

目次

第1章 調査手法と調査範囲

- 市場の定義

- 基本推定と計算

- 予測計算

- データソース

- 1次データ

- 2次データ

- 有償

- 公的

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーターの分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略ダッシュボード

- イノベーションと持続可能性の展望

第5章 市場規模・予測:技術別、2021年~2034年

- 選択的触媒還元

- 酸化触媒

第6章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 発電プラント

- 化学・石油化学

- セメント

- 金属

- 海洋

- 製造業

- その他

第7章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第8章 企業プロファイル

- Agriemach

- Babcock &Wilcox

- CECO Environmental

- Cormetech

- DCL International

- Ducon

- Environmental Energy Services

- GE Vernova

- Hug Engineering

- Johnson Matthey

- Kwangsung

- MAN Energy Solutions

- McGill AirClean

- Mitsubishi Heavy Industries

- Thermax

- Yara International

目次

The Global Stationary Catalytic Systems Market was valued at USD 6 billion in 2024 and is projected to expand at a CAGR of 4.6% from 2025 to 2034. This growth is driven by rising energy demands, rapid industrialization, and stricter energy efficiency regulations. Stationary catalytic systems are increasingly used in energy-intensive industries for their ability to reduce nitrogen oxide emissions and support clean energy goals. Their adoption across cement production, power plants, metal processing, and manufacturing industries is being propelled by government mandates focused on minimizing NOx and CO emissions.

The selective catalytic reduction (SCR) segment is poised for significant growth, with projections exceeding USD 6.5 billion by 2034. SCR technology is highly effective in reducing nitrogen oxides, achieving up to 95% NOx emission reduction. These systems are designed to meet stringent regulatory standards while maintaining ammonia emissions within acceptable thresholds, which enhances their market demand. Continuous advancements in SCR technology, including cost-efficient and compact designs suitable for diverse industrial applications, further accelerate adoption.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6 Billion |

| Forecast Value | $9.8 Billion |

| CAGR | 4.6% |

Power plants represent a key application for stationary catalytic systems, with the segment expected to grow at a CAGR of over 4% by 2034. The increasing need for effective industrial emission controls, in line with growing electricity demands, encourages power generation facilities to integrate these systems. Regulatory frameworks mandating reduced emissions of harmful gases have intensified the focus on deploying reliable emission control technologies across this sector.

The cement production sector, along with rising levels of atmospheric pollutants, is also bolstering demand for emission control systems. Strict compliance requirements and the risk of financial penalties for exceeding emission limits have amplified the importance of technologies like SCR and oxidation catalysts. Developing economies, with their expanding infrastructure and growing construction activities, are expected to drive significant growth in these systems.

The U.S. stationary catalytic systems market is projected to surpass USD 950 million by 2034, supported by increasing manufacturing activities and the shift from coal-based power plants to gas-fired facilities. Stricter environmental regulations targeting NOx and CO emissions, along with heightened awareness of the environmental impacts of these pollutants, are strengthening market growth. As industries adopt cleaner technologies to align with evolving environmental policies, the demand for stationary catalytic systems is set to rise substantially.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Technology, 2021 – 2034 (USD Million)

- 5.1 Selective catalytic reduction

- 5.2 Oxidation catalyst

Chapter 6 Market Size and Forecast, By Application, 2021 – 2034 (USD Million)

- 6.1 Key trends

- 6.2 Power plants

- 6.3 Chemical & petrochemical

- 6.4 Cement

- 6.5 Metal

- 6.6 Marine

- 6.7 Manufacturing

- 6.8 Others

Chapter 7 Market Size and Forecast, By Region, 2021 – 2034 (USD Million, ‘000 Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 France

- 7.3.3 Germany

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Russia

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 Agriemach

- 8.2 Babcock & Wilcox

- 8.3 CECO Environmental

- 8.4 Cormetech

- 8.5 DCL International

- 8.6 Ducon

- 8.7 Environmental Energy Services

- 8.8 GE Vernova

- 8.9 Hug Engineering

- 8.10 Johnson Matthey

- 8.11 Kwangsung

- 8.12 MAN Energy Solutions

- 8.13 McGill AirClean

- 8.14 Mitsubishi Heavy Industries

- 8.15 Thermax

- 8.16 Yara International

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日