水性ポリウレタン分散液市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Waterborne Polyurethane Dispersions Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 310 Pages

- 納期

- 2~3営業日

- 商品コード

- 1667066

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

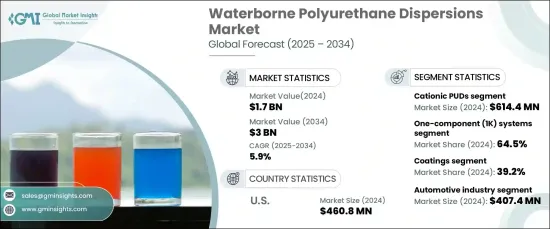

水性ポリウレタン分散液の世界市場は、2024年に17億米ドルと評価され、2025年から2034年にかけてCAGR 5.9%で成長すると予測されています。

この堅調な成長の背景には、コーティング剤、接着剤、塗料、シーラントなど多様な用途で、環境に優しく高性能な材料に対する需要が高まっていることがあります。産業界では、環境に配慮した慣行への世界のシフトに合わせるため、持続可能で低VOCのソリューションを優先する傾向が強まっています。水性ポリウレタン分散液は、性能、汎用性、環境適合性の優れた組み合わせを提供するため、あらゆる産業で魅力的な選択肢となっています。さらに、ポリマー技術の進歩と環境規制の強化が、これらのディスパージョンの採用をさらに後押ししています。二酸化炭素排出量を削減し、厳しい持続可能性基準を満たすことが重視されるようになったことで、水系PUDはより環境に優しい技術に移行する産業にとって重要なソリューションとして位置づけられています。

市場はタイプ別に、アニオン性、カチオン性、非イオン性、自己架橋性、ハイブリッド・ポリウレタン・ディスパージョンに区分されます。2024年には、カチオン性PUDが市場を独占し、全体の売上高に6億1,440万米ドル寄与しました。正電荷を帯びた構造で知られるカチオン性PUDは優れた接着力を発揮するため、耐久性と信頼性の高い接着が重要な繊維や包装などの用途で特に重宝されています。そのユニークな特性により、高性能の接着ソリューションが求められる分野で不可欠な材料となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 17億米ドル |

| 予測金額 | 30億米ドル |

| CAGR | 5.9% |

同市場はまた、機能性に基づいて1成分系(1K)と2成分系(2K)に分類されます。2024年には、1液型システムが64.5%と大きなシェアを占めています。これらの調合済みシステムは、追加の硬化成分を必要としないため、塗布工程が簡素化され、効率が向上します。その使い勝手の良さから、建設、自動車、家具製造など、作業の合理化が不可欠な業界で好まれています。

米国の水性ポリウレタン分散液市場は2024年に4億6,080万米ドルを創出したが、これは低VOCで環境に配慮した製品に対する需要の高まりによるものです。自動車、繊維、建設などの主要産業が、市場成長を後押しする上で極めて重要な役割を果たしています。グリーンケミストリーと持続可能な生産を重視する規制が強化される中、米国では水系PUDの採用が増え続けています。産業革新におけるリーダーシップとポリマー技術の進歩が相まって、米国は水系PUDの開発と応用の主要拠点となっています。自動車、包装、木材コーティングなどの分野では、性能に妥協することなく環境に優しい材料を優先する産業が多いため、高い需要が見られます。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 1次データ

- 2次データ

- 有料情報源

- 公的情報源

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 破壊

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 促進要因

- 高性能製品に対する需要の高まり

- 環境規制と持続可能な製品に対する需要の増加

- 業界の潜在的リスク&課題

- 高コスト

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場規模・予測:タイプ別、2021年~2034年

- 主要動向

- アニオン性PUD

- カチオンPUD

- 非イオン性PUD

- 自己架橋型PUD

- ハイブリッドPUD

第6章 市場規模・予測:機能性別、2021年~2034年

- 主要動向

- 一液型(1K)システム

- 2成分(2K)システム

第7章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 接着剤・シーラント

- コーティング剤

- 合成皮革製造

- 軟包装

- その他

第8章 市場規模・予測:最終用途産業別、2021年~2034年

- 主要動向

- 自動車

- 建設

- 繊維

- 家具

- 包装

- その他

第9章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- BASF

- Cargill

- Covestro

- DIC Corporation

- Dow

- Evonik

- HMG Paints

- Huntsman

- Lanxess

- Nippon Polyurethane

- PPG Industries

- RPM International

- Toyo Kasei

- Wacker Chemie

目次

The Global Waterborne Polyurethane Dispersions Market was valued at USD 1.7 billion in 2024 and is projected to grow at a CAGR of 5.9% from 2025 to 2034. This robust growth is fueled by the rising demand for eco-friendly and high-performance materials in diverse applications such as coatings, adhesives, paints, and sealants. Industries increasingly prioritize sustainable and low-VOC solutions to align with global shifts toward environmentally responsible practices. Waterborne polyurethane dispersions offer an exceptional combination of performance, versatility, and eco-friendliness, making them an attractive choice across industries. Additionally, advancements in polymer technology and stricter environmental regulations are further driving the adoption of these dispersions. The growing emphasis on reducing carbon footprints and meeting stringent sustainability standards has positioned waterborne PUDs as a key solution for industries transitioning to greener technologies.

By type, the market is segmented into anionic, cationic, nonionic, self-crosslinking, and hybrid polyurethane dispersions. In 2024, cationic PUDs dominated the market, contributing USD 614.4 million to the overall revenue. Known for their positively charged structure, cationic PUDs deliver superior adhesion, making them particularly valuable in applications such as textiles and packaging, where durable and reliable bonding is critical. Their unique properties position them as an indispensable material in sectors that demand high-performance adhesion solutions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.7 Billion |

| Forecast Value | $3 Billion |

| CAGR | 5.9% |

The market is also categorized based on functionality, dividing into one-component (1K) and two-component (2K) systems. In 2024, one-component systems captured a significant share of 64.5%. These pre-formulated systems eliminate the need for additional curing components, simplifying application processes and enhancing efficiency. Their user-friendly nature makes them a preferred choice in industries where streamlined operations are essential, including construction, automotive, and furniture manufacturing.

The U.S. waterborne polyurethane dispersions market generated USD 460.8 million in 2024, driven by the growing demand for low-VOC, eco-conscious products. Key industries, such as automotive, textiles, and construction, have played a pivotal role in boosting market growth. With increasing regulatory emphasis on green chemistry and sustainable production, the adoption of waterborne PUDs in the U.S. continues to rise. The country's leadership in industrial innovation, coupled with advancements in polymer technology, positions it as a major hub for the development and application of waterborne PUDs. High demand is evident in sectors like automotive, packaging, and wood coatings, as industries prioritize environmentally friendly materials without compromising performance.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Growing demand for high-performance products

- 3.6.1.2 Increasing environmental regulations & demand for sustainable products

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High cost

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Size and Forecast, By Type, 2021-2034 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Anionic PUDs

- 5.3 Cationic PUDs

- 5.4 Nonionic PUDs

- 5.5 Self-crosslinking PUDs

- 5.6 Hybrid PUDs

Chapter 6 Market Size and Forecast, By Functionality, 2021-2034 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 One-component (1K) systems

- 6.3 Two-component (2K) systems

Chapter 7 Market Size and Forecast, By Application, 2021-2034 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Adhesives & sealants

- 7.3 Coatings

- 7.4 Synthetic leather production

- 7.5 Flexible packaging

- 7.6 Others

Chapter 8 Market Size and Forecast, By End Use Industry, 2021-2034 (USD Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 Automotive

- 8.3 Construction

- 8.4 Textile

- 8.5 Furniture

- 8.6 Packaging

- 8.7 Others

Chapter 9 Market Size and Forecast, By Region, 2021-2034 (USD Billion, Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 BASF

- 10.2 Cargill

- 10.3 Covestro

- 10.4 DIC Corporation

- 10.5 Dow

- 10.6 Evonik

- 10.7 HMG Paints

- 10.8 Huntsman

- 10.9 Lanxess

- 10.10 Nippon Polyurethane

- 10.11 PPG Industries

- 10.12 RPM International

- 10.13 Toyo Kasei

- 10.14 Wacker Chemie

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 310 Pages

- 納期

- 2~3営業日