|

市場調査レポート

商品コード

1844361

電子パーキングブレーキシステムの市場機会、成長促進要因、産業動向分析、2025~2034年予測Electronic Parking Brake (EPB) System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 電子パーキングブレーキシステムの市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年09月23日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

概要

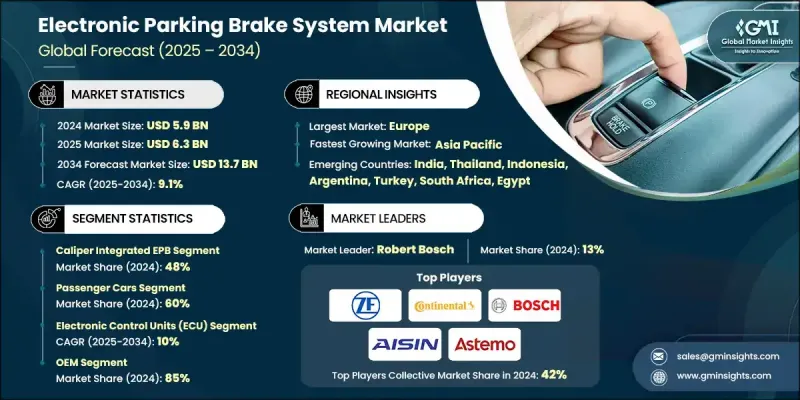

電子パーキングブレーキ(EPB)システムの世界市場規模は、2024年に59億米ドルとなり、CAGR 9.1%で成長し、2034年には137億米ドルに達すると予測されます。

自動車産業が自動化、電動化、先進安全機能を推進することが市場成長を後押ししています。EPBシステムは、その強化された性能、スペースの最適化、最新の運転支援技術とのシームレスな統合により、従来のハンドブレーキに取って代わる傾向が強まっています。自動車メーカーは、特にEV、ハイブリッド車、プラグインハイブリッド車において、オートホールド、ヒルスタートアシスト、スマート緊急ブレーキなどの機能をサポートするためにEPBを組み込んでいます。回生ブレーキや車両エネルギーシステムとの互換性は、次世代電動プラットフォームへの搭載をさらに後押ししています。新しいモデルはまた、コンパクトなアクチュエーターとワイヤレス制御を特徴としており、モジュール性と設計の柔軟性を高めています。交通安全とインテリジェント・ブレーキに対する世界的な規制の高まりに伴い、EPBはさまざまな車両カテゴリーで不可欠な部品になりつつあります。さらに、ソフトウェア制御のブレーキ機能により、EPBはリアルタイムの応答性と診断を提供するスマートセーフティシステムへと変貌しつつあります。持続可能性の動向もEPBの設計に影響を及ぼしており、メーカーはリサイクル可能な材料、低エネルギー部品、環境負荷の低減に重点を置き、世界的なグリーンモビリティの動きと歩調を合わせています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 市場規模 | 59億米ドル |

| 予測金額 | 137億米ドル |

| CAGR | 9.1% |

キャリパー一体型EPBセグメントは、2024年に48%のシェアを占め、2034年までCAGR 10%で成長すると予想されます。このタイプのEPBは、システム全体の重量を最小限に抑え、取り付けを簡素化し、従来の油圧式またはケーブルプル機構よりも優れた性能を発揮できるため、広く支持されています。EPBの採用が増加しているのは、業界が効率的でコンパクトなブレーキ・システム・アーキテクチャを選好していることを反映しています。

乗用車セグメントは2024年に60%のシェアを占め、2034年までCAGR 9.4%で成長すると予測されています。小型車や中型車、セダン、SUVへのEPBの導入が増加しており、特に自動車メーカーがADASプラットフォームと整合する高度なブレーキ技術を求めていることが成長の原動力となっています。北米、アジア太平洋、欧州の規制基準は、強化された安全義務と日常運転における快適性と自動化を求める消費者の需要により、このセグメントにおけるEPBの普及を加速し続けています。

欧州電子パーキングブレーキ(EPB)システム市場は、インテリジェントブレーキシステムを搭載したプレミアム車や高級車の急速な普及に支えられ、2024年には35%のシェアを占める。強力な政策フレームワーク、厳格な自動車安全ベンチマーク、カーエレクトロニクス部門全体で進行中の研究開発により、欧州はEPB技術の最前線における地位を固めています。コネクテッドカー、電動化プラットフォーム、自律走行ソリューションへの継続的なシフトは、この地域の優位性をさらに強めています。

電子パーキングブレーキ(EPB)システムの世界市場で競合情勢を形成している主な企業は、ZF Friedrichshafen、Continental、Hyundai Mobis、Mando、Robert Bosch、曙ブレーキ工業、日立アステモ、ブレンボ、Knorr-Bremse、アイシン精機などです。電子パーキングブレーキシステム市場で事業を展開する企業は、市場での存在感を高めるため、技術革新、モジュール設計、デジタル車両プラットフォームとの統合に注力しています。主要企業は、ADAS互換性、自律走行機能、電子緊急制御をサポートするソフトウェア主導のEPBソリューションに投資しています。プラットフォームベースの開発のためのOEMとの戦略的提携により、さまざまな車種間でのシームレスな統合が可能になります。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- グローバル

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 車両の自動化とADASへの移行

- 車両プラットフォームの電動化(EV、HEV)

- OEMは軽量でモジュール式のブレーキシステムを推進

- 利便性と安全性に対する消費者の需要

- ブレーキバイワイヤシステムの規制義務

- 業界の潜在的リスク&課題

- 極限条件下での電子機器の信頼性

- ADASとECUの統合の複雑さ

- 市場機会

- 市場とパワートレインの統合機会

- 電気およびハイブリッドパワートレインとの統合

- アクチュエータとECU技術の進歩

- ADASおよびブレーキ・バイ・ワイヤプラットフォームの拡張

- 新興市場と中級車における需要の増加

- 将来のイノベーションの機会

- 高度な統合コンセプト

- スマートEPBシステム開発

- 自動運転車の準備

- コネクテッドカー統合

- 市場とパワートレインの統合機会

- 成長可能性分析

- 規制情勢

- ポーターの分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- ESCとABSの統合

- ヒルスタートアシスト&オートホールド機能

- 緊急ブレーキアシスト統合

- ADASと自律システムの統合

- EPBシステムのコスト構造とバリューチェーン分析

- コンポーネントコストの内訳と分析

- システムタイプ別の製造コスト構造

- 統合コストが車両価格に与える影響

- 従来のシステムと比較した総所有コスト

- 価格動向

- 地域別

- 製品別

- 生産統計

- 生産拠点

- 消費拠点

- 輸出と輸入

- 特許分析

- 技術カテゴリとシステムタイプ別の有効な特許

- EPB技術における特許出願動向

- IPライセンシングおよび技術移転モデル

- 特許訴訟リスク評価

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

- 投資および資金調達分析

- EPB技術カテゴリー別研究開発投資

- EPBシステム統合へのOEM投資

- サプライヤー投資と生産能力拡大

- 政府の資金援助と安全性調査プログラム

- サプライチェーンのダイナミクスとコンポーネントの統合

- アクチュエータモーターおよび駆動部品の調達

- 電子制御ユニット開発エコシステム

- センサーとフィードバックシステムの統合

- ソフトウェア開発と検証プロセス

- 標準化の情勢と相互運用性

- ISO規格の開発と実装

- SAE国際EPB規格

- 地域標準の調和化の取り組み

- OEM固有の要件とバリエーション

- ケーススタディと実装例

- テスラEPB統合分析

- 従来のOEM EV EPB戦略

- 中国のEVメーカーがアプローチ

- 学んだ教訓とベストプラクティス

- コネクテッドカーとサイバーセキュリティの統合

- コネクテッドEPBシステムアーキテクチャ

- サイバーセキュリティの要件と脅威

- データ分析とサービス強化

- EPBシステムの信頼性と故障モード分析

- 一般的な故障モードと根本原因

- 信頼性テストと検証

- 予測メンテナンスと診断

- 品質保証と管理

- 将来の見通しと技術革新のタイムライン

- 短期的な混乱(2025-2027)

- マスマーケットにおけるEPB導入の加速

- 電気自動車の統合の成熟度

- 基本的な自律機能の統合

- コネクテッドカーサービス開発

- 中期的な混乱(2028-2030)

- 高度な自動運転車の統合

- ブレーキ・バイ・ワイヤ技術の実用化

- AIを活用した予知保全

- 車両全体のシステム統合

- 長期的な混乱(2031-2034)

- 完全自律走行車EPBシステム

- 先端材料と製造

- 量子コンピューティングの統合

- 次世代モビリティソリューション

- 短期的な混乱(2025-2027)

- 市場進化シナリオ

- 楽観的な成長シナリオ

- 保守的な成長シナリオ

- 混乱シナリオ

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:システム別、2021-2034

- 主要動向

- ケーブルプルシステム

- 電動油圧キャリパーシステム

- キャリパー一体型EPB

- その他

第6章 市場推計・予測:車でお越しの場合, 2021-2034

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV

- 商用車

- 小型商用車

- 中型商用車

- 大型商用車

第7章 市場推計・予測:コンポーネント別、2021-2034

- 主要動向

- 電子制御ユニット(ECU)

- アクチュエータ

- センサー

- スイッチと配線ハーネス

- その他

第8章 市場推計・予測:販売チャネル別、2021-2034

- 主要動向

- OEM

- アフターマーケット

第9章 市場推計・予測:推進力別、2021-2034

- 主要動向

- 内燃機関(ICE)

- ハイブリッド電気自動車(HEV/PHEV)

- バッテリー電気自動車(BEV)

第10章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- ロシア

- ポルトガル

- クロアチア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- シンガポール

- タイ

- インドネシア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

- エジプト

第11章 企業プロファイル

- グローバルプレーヤー

- Aisin Seiki

- Akebono Brake Industry

- Brembo

- Continental

- Hitachi Astemo

- Mando

- Robert Bosch

- ZF Friedrichshafen

- 地域プレーヤー

- Advics

- BWI

- Chassis Brakes International

- Haldex

- Hyundai Mobis

- Knorr-Bremse

- Nissin Kogyo

- WABCO

- 新興プレーヤー

- Aptiv

- Autoliv

- Denso

- Magna International

- Nexteer Automotive

- Schaeffler

- Tenneco

- Valeo