|

市場調査レポート

商品コード

1913405

消防車市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Fire Truck Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 消防車市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2025年12月24日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

概要

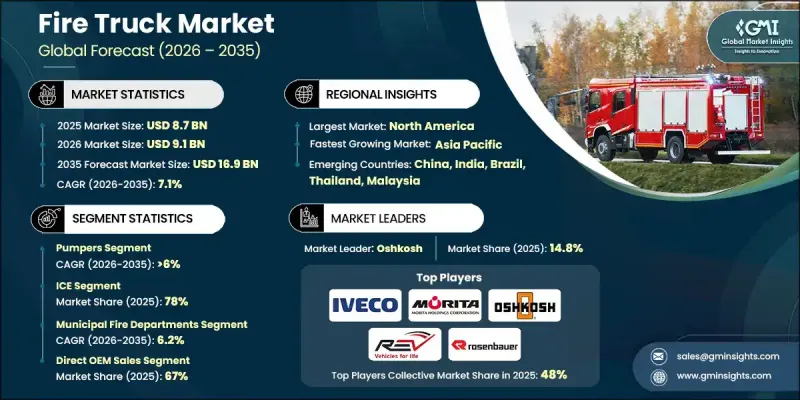

世界の消防車市場は2025年に87億米ドルと評価され、2035年までにCAGR 7.1%で成長し、169億米ドルに達すると予測されています。

急速な都市化が進み、人口密度、高層建築、産業活動が増加し続けることで火災リスクと緊急時対応要件が高まっていることから、市場は着実な勢いを増しています。自治体や工業地帯では、拡大する住宅地、商業施設、インフラ資産を保護するため、近代的な消防車両群への予算配分を増加させています。消防当局は、進化する安全基準、排出ガス規制、性能要件に対応するため、車両群の近代化をますます優先しています。多くの消防署では、運用上の信頼性やコンプライアンス基準を満たさなくなった旧式車両を退役させ、ポンプ能力の向上、到達距離の延長、乗員の安全システムの強化を備えた先進的な消防車両への投資を進めています。最新の消防車は信頼性の向上、稼働停止時間の削減、デジタル技術の統合強化を実現し、各機関の緊急対応態勢強化に貢献しております。また、リアルタイム診断、状況認識、効率的な資源配置を支援するコネクテッドシステムの普及拡大も市場を後押ししており、複雑な緊急事態においても消防機関が迅速に対応し、より効果的に活動することを可能にしております。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 87億米ドル |

| 予測金額 | 169億米ドル |

| CAGR | 7.1% |

ポンプ車カテゴリーは2025年に43%のシェアを占め、2026年から2035年にかけてCAGR6%で成長すると予測されています。需要は、ポンプ効率の向上、車両操作性の改善、密集した都市環境での効果的な運用能力によって支えられています。老朽化した車両の代替と、費用対効果の高い多目的消防車両への関心の高まりが、このセグメントの拡大を継続的に後押ししています。

内燃機関ベースの消防車は2025年に78%のシェアを占め、2035年までCAGR6.6%で成長すると予測されています。この優位性は、確立された駆動系技術、燃料の広範な入手可能性、そして過酷な消防活動において持続的な出力を供給できる能力によって支えられています。排出ガス制御と車載監視システムの継続的な改良により、これらの車両は厳格化する環境基準への適合を維持しています。

米国消防車市場は2025年に31億9,000万米ドルの規模に達しました。老朽化した車両の更新は、維持費の増加、安全性の不足、更新された運用基準への適合といった課題に取り組む消防部門にとって、依然として主要な成長要因です。複数レベルでの資金調達施策が近代的な緊急車両の調達を加速させ、更新サイクルの短縮と消防士の保護・車両信頼性への投資拡大を支えています。

よくあるご質問

目次

第1章 調査手法

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 都市化とインフラ拡張

- 厳格な防火安全規制

- フリートの近代化と更新サイクル

- 消防設備における技術的進歩

- 業界の潜在的リスク&課題

- 車両およびメンテナンスコストの高さ

- 長いOEMリードタイムと予算制約

- 市場機会

- 電動化・ハイブリッド消防車

- 空港及び産業用消防需要

- テレメトリー及びテレマティクス統合

- アフターマーケットにおけるアップグレードと改造

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 連邦自動車安全基準(FMVSS)

- 環境保護庁(EPA)欧州

- 欧州

- VDAガイドライン(VDA 5)

- EU型式認証/完成車型式認証(WVTA)

- UNE規格(スペイン規格協会)

- 省令及びUNI規格

- BS EN規格及び英国型式認証

- アジア太平洋地域

- 中国国家標準(GB)

- 日本JIS規格の要件

- 韓国KS認証

- 自動車産業標準140

- タイ工業規格協会(TISI)

- ラテンアメリカ

- INMETRO(国立計量研究所)

- INTI認証(国立工業技術研究所)

- NOM規格(Norma Oficial Mexicana)

- 中東・アフリカ

- ESMA/エミレーツ適合性評価スキーム(ECAS)

- GCC技術規制

- SABS認証

- 北米

- ポーター分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格分析

- 製品別

- 地域別

- コスト内訳分析

- 総所有コスト(TCO)フレームワーク

- 技術タイプ別総所有コスト(TCO)

- 部品単価分析

- AMと従来型製造のコスト比較

- 生産統計

- 生産拠点

- 消費拠点

- 輸出入

- 特許分析

- 持続可能性と環境面

- 持続可能な実践

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- カーボンフットプリントに関する考慮事項

- 使用事例

- アフターマーケットサービス及び再生エコシステム

- 保守・サービス契約

- スペアパーツ及び改修需要

- ライフサイクルサービス収益への貢献度

- フリートライフサイクル及び更新サイクル分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画と資金調達

第5章 市場推計・予測:車両別、2022-2035

- ポンプ車

- 高所作業車(はしご車)

- タンカー

- 救助車

- 航空機救助消防車両(ARFF車両)

- 産業用トラック

- 特殊トラック

第6章 市場推計・予測:パワートレイン別、2022-2035

- 内燃機関(ICE)

- 電気自動車

- ハイブリッド

第7章 市場推計・予測:用途別、2022-2035

- 自治体消防署

- 空港消防サービス

- 産業用消防サービス

- 山火事管理

- その他

第8章 市場推計・予測:容量別、2022-2035

- 1,000ガロン未満

- 1,000~2,000ガロン

- 2,000ガロン以上

第9章 市場推計・予測:販売チャネル別、2022-2035

- 直接OEM販売

- 正規販売店/販売代理店

第10章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- ロシア

- ポーランド

- ルーマニア

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- ANZ

- ベトナム

- インドネシア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ地域

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- 世界企業

- Bronto Skylift

- IVECO(Magirus)

- KME Fire Apparatus

- Metz Fire &Rescue

- Morita

- Oshkosh

- REV

- Rosenbauer

- Seagrave Fire Apparatus

- Ziegler

- 地域メーカー

- Danko Emergency Equipment

- Darley

- Desautel

- E-ONE

- Ferrara Fire Apparatus

- HME Ahrens

- Marion Body Works

- Smeal Fire Apparatus

- Terberg DTS

- Vema Lift

- 新興メーカー

- Chase enterprise

- FPT Industrial Electric Fire Truck

- Minerva Fire Trucks

- Sino Fire Trucks

- TATA Fire Trucks

- Volkan Fire Trucks