住宅用スマート水道メーター市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Residential Smart Water Meter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日

- 商品コード

- 1667000

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

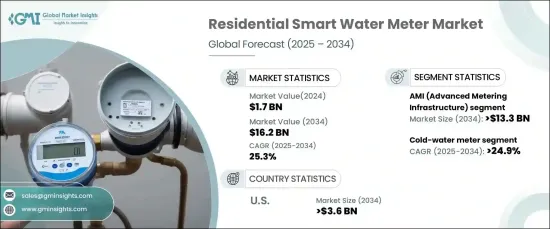

住宅用スマート水道メーターの世界市場は、2024年に17億米ドルと評価され、2025年から2034年にかけて25.3%という驚異的なCAGRで拡大すると予測されています。

この成長の主な要因は、節水に対する関心の高まり、進行中の技術革新、政府支援のイニシアティブの数々です。効率的な水管理に対する世界の需要が高まるにつれ、スマート水道メーターは一般家庭や公益事業者にとって不可欠なツールになりつつあります。これらの高度なデバイスは、水の使用量をリアルタイムで監視することを可能にし、消費者が水漏れを検知し、無駄遣いを減らし、消費量を最適化できるようにします。世界的に水不足に対する懸念が高まっていることから、資源管理に対するより持続可能でスマートなアプローチの必要性が高まっています。これに対応するため、自治体や公益企業はスマートメーターシステムに多額の投資を行っています。さらに、モノのインターネット(IoT)とデータ分析をこれらのメーターに統合することで、強力で使いやすいプラットフォームへと変貌しつつあります。これらのシステムは実用的な洞察を提供し、住宅所有者や水道事業者が十分な情報に基づいた意思決定を行い、資源効率を向上させるのに役立っています。

この市場の主要プレーヤーである高度計測インフラ(AMI)セグメントは、2034年までに133億米ドルに達すると予想されています。AMIの魅力は、卓越した精度でリアルタイムデータを提供し、公益事業者と消費者間の双方向通信を実現する能力にあります。AMI技術により、水道事業者は遠隔地から使用量を追跡し、漏水を検知し、請求プロセスを合理化することができ、これらはすべて、無収益水の損失を最小限に抑えながら運営効率を高めるのに役立ちます。多くの利点を持つAMIは、特に資源の節約と運用の最適化が最重要視される地域において、近代的な水管理システムのバックボーンとしてますます注目されています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 17億米ドル |

| 予測金額 | 162億米ドル |

| CAGR | 25.3% |

市場の成長は、住宅分野におけるスマート水道メーターの需要にも大きく影響されます。2034年までのCAGRは24.9%で、これらのメーターは、特に飲料水の消費量を追跡するのに不可欠な冷水メーターの場合に、広く採用されると予想されます。冷水メーターは、消費者や公益事業者が水資源を効果的に管理するのに役立つことから、使用が急増しています。規制の圧力や、IoTやAMIの開発を含む技術の進歩は、これらのメーターをより正確で使いやすいものにし、その魅力をさらに高めています。

米国では、住宅用スマート水道メーター市場は2034年までに36億米ドルを生み出すと予測されています。これは、持続可能性に対する意識の高まり、特に干ばつに見舞われやすい地域での水不足に対処する緊急の必要性、水インフラの近代化が主な原因です。州や連邦政府の規制がより持続可能な水利用を推進する中、米国中の公益事業会社は、水消費をより効果的に監視・管理するためにスマートメーター・ソリューションを導入しています。最先端技術と強力な政策支援を組み合わせることで、米国市場は今後10年間で目覚ましい成長を遂げると思われます。

目次

第1章 調査手法と調査範囲

- 市場の定義

- 基本推定と計算

- 予測計算

- データソース

- 1次データ

- 2次データ

- 有償

- 公的

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーターの分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- PESTEL分析

第4章 競合情勢

- 戦略ダッシュボード

- イノベーションと持続可能性の展望

第5章 市場規模・予測:技術別、2021年~2034年

- 主要動向

- AMI

- AMR

第6章 市場規模・予測:製品別、2021年~2034年

- 主要動向

- 温水メーター

- 冷水メーター

第7章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- イタリア

- ロシア

- スペイン

- アジア太平洋

- 中国

- オーストラリア

- インド

- 日本

- 韓国

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

- 南アフリカ

- エジプト

- ラテンアメリカ

- ブラジル

- アルゼンチン

第8章 企業プロファイル

- Aclara Technologies

- Apator

- Arad Group

- Badger Meter

- BMETERS

- Diehl Stiftung

- Honeywell International

- Itron

- Kamstrup

- Landis+Gyr

- Nepune Technology Group

- Ningbo Water Meter

- Schneider Electric

- Sensus

- Siemens

- Sontex

- Zenner International

目次

The Global Residential Smart Water Meter Market, valued at USD 1.7 billion in 2024, is projected to expand at a staggering CAGR of 25.3% between 2025 and 2034. This growth is largely fueled by increasing concerns about water conservation, ongoing technological innovations, and a host of government-backed initiatives. As the global demand for efficient water management grows, smart water meters are becoming indispensable tools for households and utilities alike. These advanced devices enable real-time monitoring of water usage, empowering consumers to detect leaks, reduce wastage, and optimize consumption. Given the escalating concerns about water scarcity worldwide, there is a growing need for more sustainable and smarter approaches to resource management. In response, municipalities and utilities are investing heavily in smart metering systems. Moreover, the integration of the Internet of Things (IoT) and data analytics into these meters is transforming them into powerful, user-friendly platforms. These systems offer actionable insights, helping homeowners and water service providers make informed decisions and improve resource efficiency.

The Advanced Metering Infrastructure (AMI) segment, which is a key player in this market, is expected to reach USD 13.3 billion by 2034. The appeal of AMI lies in its ability to deliver real-time data with remarkable accuracy and offer two-way communication between utilities and consumers. AMI technology allows water service providers to remotely track usage, detect leaks, and streamline billing processes, all of which help boost operational efficiency while minimizing non-revenue water losses. With its many benefits, AMI is increasingly seen as the backbone of modern water management systems, especially in areas where resource conservation and operational optimization are paramount.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.7 Billion |

| Forecast Value | $16.2 Billion |

| CAGR | 25.3% |

The market's growth is also heavily influenced by the demand for smart water meters in residential sectors. With a CAGR of 24.9% through 2034, these meters are expected to gain widespread adoption, particularly in the case of cold-water meters, which are vital for tracking potable water consumption. Cold-water meters are seeing a surge in use, driven by their ability to help consumers and utilities manage water resources effectively. Regulatory pressures and technological advancements, including developments in IoT and AMI, are making these meters more accurate and user-friendly, further enhancing their appeal.

In the United States, the residential smart water meter market is projected to generate USD 3.6 billion by 2034. This is largely attributed to heightened awareness of sustainability, the urgent need to address water shortages, especially in drought-prone regions, and the modernization of water infrastructure. With state and federal regulations pushing for more sustainable water usage, utilities across the U.S. are adopting smart metering solutions to monitor and manage water consumption more effectively. By combining cutting-edge technology with strong policy support, the U.S. market is set for impressive growth in the coming decade.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Technology, 2021 – 2034 (USD Million, ‘000 Units)

- 5.1 Key trends

- 5.2 AMI

- 5.3 AMR

Chapter 6 Market Size and Forecast, By Product, 2021 – 2034 (USD Million, ‘000 Units)

- 6.1 Key trends

- 6.2 Hot water meter

- 6.3 Cold water meter

Chapter 7 Market Size and Forecast, By Region, 2021 – 2034 (USD Million, ‘000 Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 France

- 7.3.3 Germany

- 7.3.4 Italy

- 7.3.5 Russia

- 7.3.6 Spain

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 India

- 7.4.4 Japan

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Turkey

- 7.5.4 South Africa

- 7.5.5 Egypt

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 Aclara Technologies

- 8.2 Apator

- 8.3 Arad Group

- 8.4 Badger Meter

- 8.5 BMETERS

- 8.6 Diehl Stiftung

- 8.7 Honeywell International

- 8.8 Itron

- 8.9 Kamstrup

- 8.10 Landis+Gyr

- 8.11 Nepune Technology Group

- 8.12 Ningbo Water Meter

- 8.13 Schneider Electric

- 8.14 Sensus

- 8.15 Siemens

- 8.16 Sontex

- 8.17 Zenner International

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日