|

市場調査レポート

商品コード

1666978

車両ネットワーキング市場の機会、成長促進要因、産業動向分析、2025~2034年の予測Vehicle Networking Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 車両ネットワーキング市場の機会、成長促進要因、産業動向分析、2025~2034年の予測 |

|

出版日: 2024年12月14日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

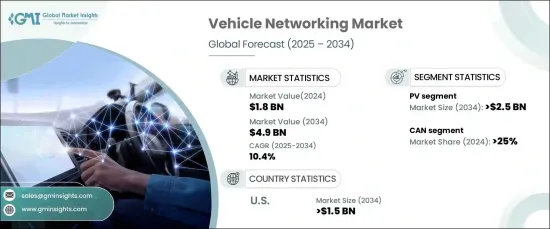

世界の車両ネットワーキング市場は、2024年に18億米ドルに達すると見込まれ、2025年から2034年にかけてCAGR 10.4%の堅調な成長が予測されています。

この成長の主因は、モノのインターネット(IoT)と5Gネットワークの統合によって加速するコネクテッドカー技術の採用です。これらの最先端技術は、車両とインフラ間のシームレスなリアルタイム通信を可能にし、安全性、効率性、全体的な運転体験を向上させています。自律走行車の拡大により、先進的なネットワーキング・ソリューションの需要はさらに高まっています。効率的な車車間(V2V)および車車間(V2I)通信は、自動運転車が円滑に機能するために不可欠であり、自動車産業の将来にとって重要な要素となっています。

さらに、車両診断と予知保全が重視されるようになっていることも、市場の主要な促進要因となっています。高度なネットワーキング技術が導入されたことで、車両性能の継続的なモニタリングが可能になり、潜在的な問題の早期発見が可能になりました。この早期発見により、信頼性が向上するだけでなく、メンテナンス・コストと車両のダウンタイムが削減され、個人消費者とフリート・オペレーターの双方にメリットがもたらされます。さらに、リアルタイムの衝突回避や緊急ブレーキなどの安全機能の進歩が、信頼性の高い高性能な車両ネットワーキング・システムの必要性を押し上げています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 18億米ドル |

| 予測金額 | 49億米ドル |

| CAGR | 10.4% |

車両タイプ別では、乗用車(PV)、小型商用車(LCV)、大型商用車(HCV)、自律走行車両(AGV)に区分されます。PVセグメントは2024年に50%の圧倒的シェアを占め、2034年には25億米ドルに達すると予測されています。この優位性は、インフォテインメント・システム、リアルタイム・ナビゲーション、強化された安全機能など、乗用車への搭載が進む先進車載技術に対する消費者需要の高まりによるところが大きいです。

接続性の面では、車両ネットワーキング市場はLIN、CAN、RF、イーサネット、FlexRay、MOSTに分類されます。CAN(Controller Area Network)セグメントは、その信頼性、堅牢性、費用対効果により、2024年には25%のシェアを占めています。エンジン制御やブレーキなどの重要な自動車システムのリアルタイム・データ・トランスミッションに広く利用されており、電磁干渉の多い過酷な環境でも優れた性能を発揮します。

2024年の車両ネットワーキング市場は米国が首位で、世界シェアの90%を占めています。米国の自動車市場は2034年までに15億米ドルに達すると予想されており、これは同国の確立された自動車部門と、自律走行、電気自動車、5Gコネクティビティといった画期的な技術の急速な導入が原動力となっています。これらの技術革新は高度な車両ネットワーキング・ソリューションに大きく依存しており、米国市場を大きく成長させる促進要因となっています。消費者の期待が高まり、技術が進化し続けるなか、車両ネットワーキング市場は、車両の接続性と性能を高める革新的なソリューションを提供し、目覚ましい拡大を遂げようとしています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- テクノロジープロバイダー

- サービスプロバイダー

- 流通業者

- 最終用途

- 利益率分析

- 価格分析

- コスト内訳

- 技術とイノベーションの展望

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 促進要因

- 政府による二酸化炭素排出量削減への注力

- 電気自動車の販売拡大

- 自動車部品産業に対する政府の支援

- 市場プレーヤーによる戦略的イニシアティブ

- 業界の潜在的リスク&課題

- 電気自動車における半導体消費の増加

- 発展途上国や後発開発途上国における自律移動インフラの不足

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合ポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- PV

- LCV

- HCV

- AGV

第6章 市場推計・予測:コネクティビティ別、2021年~2034年

- 主要動向

- CAN(コントローラエリアネットワーク)

- LIN(ローカル相互接続ネットワーク)

- RF(無線周波数)

- フレックスレイ

- イーサネット

- MOST(メディア指向システム・トランスポート)

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- パワートレイン

- セーフティ

- ボディ・エレクトロニクス

- シャシー

- インフォテインメント

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第9章 企業プロファイル

- Acome

- Analog Devices

- Bosch

- Broadcom

- Continental

- Intel

- Harman

- Marvell Semiconductor

- Microchip Technology

- NXP Semiconductors

- ON Semiconductor

- Qualcomm

- Renesas

- Sierra Wireless

- Spiarent

- Communications

- STMicroelectronics NV

- Texas Instrumental

- Toshiba

- Xilinx

The Global Vehicle Networking Market, with a valuation of USD 1.8 billion in 2024, is expected to grow at a robust CAGR of 10.4% from 2025 to 2034. This growth is primarily driven by the accelerating adoption of connected car technologies, fueled by the integration of the Internet of Things (IoT) and 5G networks. These cutting-edge technologies enable seamless real-time communication between vehicles and infrastructure, enhancing safety, efficiency, and the overall driving experience. The expansion of autonomous vehicles has further spurred demand for advanced networking solutions. Efficient vehicle-to-vehicle (V2V) and vehicle-to-infrastructure (V2I) communication are vital for the smooth functioning of self-driving cars, making them a critical component in the future of the automotive industry.

Furthermore, the increasing emphasis on vehicle diagnostics and predictive maintenance is becoming a major market driver. With advanced networking technologies in place, continuous monitoring of vehicle performance is now possible, allowing for early detection of potential issues. This early detection not only ensures better reliability but also helps to reduce maintenance costs and vehicle downtime, benefiting both individual consumers and fleet operators. In addition, advancements in safety features, such as real-time collision avoidance and emergency braking, are pushing the need for reliable, high-performance vehicle networking systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.8 Billion |

| Forecast Value | $4.9 Billion |

| CAGR | 10.4% |

In terms of vehicle types, the market is segmented into Passenger Vehicles (PV), Light Commercial Vehicles (LCV), Heavy Commercial Vehicles (HCV), and Autonomous Guided Vehicles (AGV). The PV segment held a dominant 50% share in 2024 and is forecast to reach USD 2.5 billion by 2034. This dominance is largely due to the growing consumer demand for advanced in-car technologies, including infotainment systems, real-time navigation, and enhanced safety features that are increasingly being incorporated into passenger vehicles.

On the connectivity front, the vehicle networking market is categorized into LIN, CAN, RF, Ethernet, FlexRay, and MOST. The CAN (Controller Area Network) segment held a 25% share in 2024 thanks to its reliability, robustness, and cost-effectiveness. It's widely used for real-time data transmission in critical automotive systems like engine control and braking, providing exceptional performance even in harsh environments with high electromagnetic interference.

The U.S. vehicle networking market was the leader in 2024, accounting for 90% of the global share. The market in the U.S. is expected to reach USD 1.5 billion by 2034, driven by the country's well-established automotive sector and rapid adoption of groundbreaking technologies such as autonomous driving, electric vehicles, and 5G connectivity. These innovations rely heavily on advanced vehicle networking solutions, propelling the U.S. market toward substantial growth. As consumer expectations rise and technology continues to evolve, the vehicle networking market is poised for remarkable expansion, delivering innovative solutions that enhance vehicle connectivity and performance.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Technology providers

- 3.2.2 Service providers

- 3.2.3 Distributors

- 3.2.4 End use

- 3.3 Profit margin analysis

- 3.4 Pricing analysis of

- 3.5 Cost breakdown

- 3.6 Technology & innovation landscape

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Government focus on reducing carbon emissions

- 3.9.1.2 Growing sales of electric vehicles

- 3.9.1.3 Government support for automotive components industry

- 3.9.1.4 Strategic initiatives by market players

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Increasing consumption of semiconductors in electric vehicles

- 3.9.2.2 Lack of autonomous mobility infrastructure in developing and underdeveloped countries

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 PV

- 5.3 LCV

- 5.4 HCV

- 5.5 AGV

Chapter 6 Market Estimates & Forecast, By Connectivity, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 CAN (Controller Area Network)

- 6.3 LIN (Local Interconnect Network)

- 6.4 RF (Radio Frequency)

- 6.5 FlexRay

- 6.6 Ethernet

- 6.7 MOST (Media Oriented Systems Transport)

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Powertrain

- 7.3 Safety

- 7.4 Body electronics

- 7.5 Chassis

- 7.6 Infotainment

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Russia

- 8.3.7 Nordics

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 ANZ

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 South Africa

- 8.6.3 Saudi Arabia

Chapter 9 Company Profiles

- 9.1 Acome

- 9.2 Analog Devices

- 9.3 Bosch

- 9.4 Broadcom

- 9.5 Continental

- 9.6 Intel

- 9.7 Harman

- 9.8 Marvell Semiconductor

- 9.9 Microchip Technology

- 9.10 NXP Semiconductors

- 9.11 ON Semiconductor

- 9.12 Qualcomm

- 9.13 Renesas

- 9.14 Sierra Wireless

- 9.15 Spiarent

- 9.16 Communications

- 9.17 STMicroelectronics NV

- 9.18 Texas Instrumental

- 9.19 Toshiba

- 9.20 Xilinx