|

市場調査レポート

商品コード

1666966

ペット用がん治療薬の市場機会、成長促進要因、産業動向分析、2025~2034年予測Pet Cancer Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ペット用がん治療薬の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2024年12月04日

発行: Global Market Insights Inc.

ページ情報: 英文 136 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

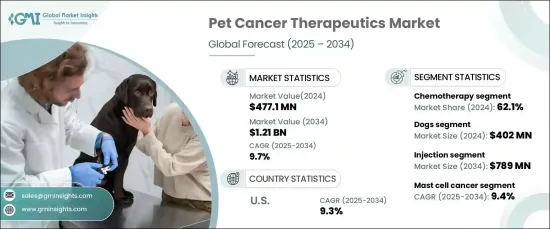

ペット用がん治療薬の世界市場は、2024年に4億7,710万米ドルに達し、2025~2034年にかけてCAGR 9.7%で成長すると予測されています。

この成長の主な要因は、ペットの飼い主が動物に対する高度ヘルスケアをますます優先するようになり、ペットの人間化の傾向が高まっていることです。診断能力の向上と、標的療法や免疫療法を含む最先端の治療が、獣医によるがん治療へのアクセス性と有効性をさらに高めています。

ペットの高齢化はがんの有病率の上昇につながり、腫瘍学的ソリューションの需要を大幅に押し上げています。このような消費者行動の変化は、獣医学における絶え間ない進歩と相まって、ペットのための革新的な延命治療に対する市場ニーズの高まりを裏付けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 4億7,710万米ドル |

| 予測金額 | 12億1,000万米ドル |

| CAGR | 9.7% |

市場は動物種ごとに犬、猫、その他の動物に区分されます。犬が最大の市場シェアを占め、2024年の市場規模は4億200万米ドルでした。この優位性は、他のペットと比較して犬ではリンパ腫、骨肉腫、乳腺腫瘍などのがんの発生率が高いことに起因しています。犬の腫瘍学における専門的治療の必要性の高まりは、効果的な治療オプションの需要を促進し続けています。

治療法別では、化学療法、免疫療法、標的療法、併用療法があります。化学療法は2024年に62.1%のシェアを獲得し、主要セグメントとして浮上しました。がん細胞を標的とし、その増殖を抑制する有効性で知られる化学療法は、さまざまながん、特にリンパ腫や肥満細胞腫の治療の要であり続けています。特に一般的な犬のがんに対する寛解成功率が高いことから、獣医によるがん治療における化学療法の継続的な優位性が確保されています。

米国のペット用がん治療薬市場は、2025~2034年を通してCAGR 9.3%を維持しました。このリーダーシップは、同国の強固な獣医ヘルスケアインフラ、高いペット飼育率、高度ながん治療に対する広範な認識によってもたらされました。獣医腫瘍学の研究と技術への多額の投資は、免疫療法や標的治療を含む革新的な治療法の開発を可能にし、米国市場をさらに強化しています。

さらに、高齢化したペットの間でがんの有病率が増加していることから、高品質の治療ソリューションに対する需要が引き続き高まっています。高度な獣医学的治療に対する認識と採用が高まるにつれ、ペット用がん治療薬市場は世界的に力強い成長が見込まれ、北米は業界の動向を形成する上で極めて重要な役割を担っています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- ペットの人間化の増加

- ペットのがん罹患率の上昇

- 獣医腫瘍学における診断と治療の進歩

- 認識と診断能力の向上

- 業界の潜在的リスク&課題

- 高額な治療費

- 副作用と動物への耐性

- 促進要因

- 成長可能性の分析

- 規制状況

- パイプライン分析

- 今後の市場動向

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 企業マトリックス分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:動物種別、2021~2034年

- 主要動向

- 犬

- 猫

- その他

第6章 市場推計・予測:治療法別、2021~2034年

- 主要動向

- 化学療法

- 免疫療法

- 標的療法

- 併用療法

第7章 市場推計・予測:投与経路別、2021~2034年

- 主要動向

- 経口

- 注射

第8章 市場推計・予測:がん種別、2021~2034年

- 主要動向

- リンパ腫

- 肥満細胞腫

- メラノーマ

- 乳腺がん、扁平上皮がん

- その他

第9章 市場推計・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- AB Science

- Boehringer Ingelheim International

- CureLab Oncology

- Dechra Pharmaceuticals

- Elanco Animal Health

- ELIAS Animal Health

- NovaVive

- Qbiotics

- Pfizer

- Torigen

- Vibrac

- Vivesto

- Zoetis

The Global Pet Cancer Therapeutics Market reached USD 477.1 million in 2024 and is anticipated to grow at a CAGR of 9.7% from 2025 to 2034. This growth is primarily attributed to the rising trend of pet humanization, as pet owners increasingly prioritize advanced healthcare for their animals. Enhanced diagnostic capabilities and cutting-edge treatments, including targeted therapies and immunotherapies, are further boosting the accessibility and effectiveness of veterinary cancer care.

The aging pet population has led to a higher prevalence of cancer, significantly driving the demand for oncology solutions. This evolution in consumer behavior, combined with continual advancements in veterinary medicine, underlines the growing market need for innovative and life-prolonging treatments for pets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $477.1 Million |

| Forecast Value | $1.21 Billion |

| CAGR | 9.7% |

The market is segmented by species into dogs, cats, and other animals. Dogs held the largest market share, valued at USD 402 million in 2024. This dominance is attributed to the higher incidence of cancers such as lymphoma, osteosarcoma, and mammary tumors in dogs compared to other pets. The growing need for specialized treatments in canine oncology continues to propel the demand for effective therapeutic options.

By therapy, the market includes chemotherapy, immunotherapy, targeted therapy, and combination therapy. Chemotherapy emerged as the leading segment, generating a 62.1% share in 2024. Known for its efficacy in targeting and inhibiting the growth of cancer cells, chemotherapy remains a cornerstone of treatment for various cancers, particularly lymphoma and mast cell tumors. Its high success rates in remission, especially for common canine cancers, ensure its continued prominence in veterinary oncology.

U.S. pet cancer therapeutics market held a CAGR of 9.3% throughout 2025-2034. This leadership is driven by the country's robust veterinary healthcare infrastructure, high pet ownership rates, and widespread awareness of advanced cancer treatments. Significant investments in veterinary oncology research and technology enable the development of innovative therapies, including immunotherapy and targeted treatments, further strengthening the U.S. market.

Additionally, the increasing prevalence of cancer among aging pets continues to fuel the demand for high-quality therapeutic solutions. As awareness and adoption of advanced veterinary care rise, the pet cancer therapeutics market is expected to witness robust growth globally, with North America maintaining a pivotal role in shaping industry trends.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increased pet humanization

- 3.2.1.2 Rising cancer incidence in pets

- 3.2.1.3 Advancements in veterinary oncology diagnosis and treatment

- 3.2.1.4 Growing awareness and diagnostic capabilities

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment costs

- 3.2.2.2 Side effects and animal tolerance

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Pipeline analysis

- 3.6 Future market trends

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Species, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Dogs

- 5.3 Cats

- 5.4 Other species

Chapter 6 Market Estimates and Forecast, By Therapy, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Chemotherapy

- 6.3 Immunotherapy

- 6.4 Targeted therapy

- 6.5 Combination therapy

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Injection

Chapter 8 Market Estimates and Forecast, By Cancer Type, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Lymphoma

- 8.3 Mast cell cancer

- 8.4 Melanoma

- 8.5 Mammary and squamous cell cancer

- 8.6 Other cancer types

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AB Science

- 10.2 Boehringer Ingelheim International

- 10.3 CureLab Oncology

- 10.4 Dechra Pharmaceuticals

- 10.5 Elanco Animal Health

- 10.6 ELIAS Animal Health

- 10.7 NovaVive

- 10.8 Qbiotics

- 10.9 Pfizer

- 10.10 Torigen

- 10.11 Vibrac

- 10.12 Vivesto

- 10.13 Zoetis