|

市場調査レポート

商品コード

1666962

特殊ポリスチレン樹脂市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Specialty Polystyrene Resin Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 特殊ポリスチレン樹脂市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2024年12月18日

発行: Global Market Insights Inc.

ページ情報: 英文 235 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

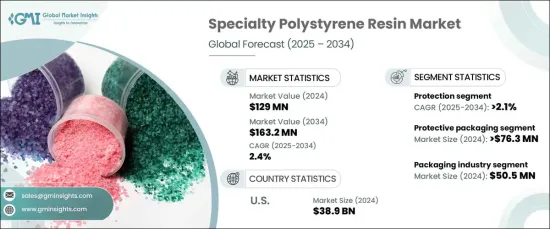

世界の特殊ポリスチレン樹脂市場は、2024年に1億2,900万米ドルとなり、2025年から2034年までのCAGRは2.4%と予測され、着実な成長が見込まれています。

特殊ポリスチレン樹脂は、強化された衝撃強度、耐熱性、長持ちする耐久性など、その卓越した性能特性で認められています。標準的なポリスチレンとは異なり、これらの樹脂は優れた機能性を必要とする用途に対応するため、電子機器、医療機器、高性能パッケージングなどの分野で好まれる材料となっています。産業界が厳しい性能要求を満たす材料を優先し続ける中、特殊ポリスチレン樹脂の市場は拡大する傾向にあります。この成長は、製造技術の進歩、材料効率に対する意識の高まり、様々な用途における軽量でコスト効率の高いソリューションの傾向の高まりによってさらに促進されます。

特殊ポリスチレン樹脂市場の保護分野は、2024年に5,700万米ドルの評価額を達成し、予測期間中のCAGRは2.1%となる見込みです。このセグメントは、耐久性、耐衝撃性、熱安定性を必要とする用途における材料の価値を強調するものです。繊細な電子機器の保護ケーシングから自動車分野の部品に至るまで、特殊ポリスチレン樹脂は、輸送、取り扱い、保管中に信頼できる保護を必要とする重要なニーズに対応しています。その軽量性と費用対効果により、ポリスチレン樹脂の魅力はさらに高まり、性能とコストの両方を最適化しようとする業界にとって最良の選択肢となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 1億2,900万米ドル |

| 予測金額 | 1億6,320万米ドル |

| CAGR | 2.4% |

2024年に7,630万米ドルと評価された保護包装分野は、今後10年間CAGR 2.1%で成長すると予測されています。軽量で耐久性があり、コスト効率の高いパッケージング・ソリューションに対する需要の高まりが、特殊ポリスチレン樹脂の採用を後押ししています。これらの材料は衝撃吸収と断熱に優れているため、電子機器や生鮮品などのデリケートな品目の包装に不可欠です。特に家電やヘルスケア業界におけるeコマースの急速な拡大に伴い、頑丈な保護パッケージへのニーズが高まっています。特殊ポリスチレン樹脂は、強度、信頼性、コストのバランスが取れたソリューションを提供し、この成長の要として台頭してきています。

米国の特殊ポリスチレン樹脂市場は2024年に3,890万米ドルを生み出し、2025年から2034年までのCAGRは2.5%と予測されています。米国での市場拡大は、包装、エレクトロニクス、自動車、ヘルスケアなど、産業全般にわたる特殊ポリスチレン樹脂の幅広い用途が原動力となっています。包装分野、特に食品包装は、この材料の透明性と保護特性から大きな恩恵を受けています。さらに、持続可能性とリサイクル可能性への注目の高まりが市場力学に影響を与えています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 1次データ

- 2次データ

- 有料情報源

- 公的情報源

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 破壊

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 促進要因

- 環境に優しい素材への需要の高まり

- エレクトロニクス分野での用途拡大

- 材料技術の進歩

- 業界の潜在的リスク&課題

- 環境への懸念

- リサイクルの課題

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競争情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:機能別、2021年~2034年

- 主要動向

- 保護

- 断熱

- 軽量化

- 耐久性

- 透明性

- その他

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 保護包装

- 建築・建設

- 自動車・輸送

- 電気・電子

- ヘルスケア

- その他

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 包装業界

- エレクトロニクス産業

- 自動車産業

- 建設業界

- ヘルスケア産業

- その他

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Asahi Kasei

- BASF

- Braskem

- China Petrochemical Corporation

- ExxonMobil

- Formosa Plastics Corporation

- INEOS Styrolution

- LG Chem

- Mitsubishi Chemical Corporation

- SABIC

- Sinopec

- Styron(Dow)

- TotalEnergies

The Global Specialty Polystyrene Resin Market, valued at USD 129 million in 2024, is poised for steady growth, with projections indicating a CAGR of 2.4% from 2025 to 2034. Specialty polystyrene resin is recognized for its exceptional performance attributes, including enhanced impact strength, heat resistance, and long-lasting durability. Unlike standard polystyrene, these resins cater to applications that require superior functionality, making them a preferred material in sectors such as electronics, medical devices, and high-performance packaging. As industries continue to prioritize materials that meet stringent performance demands, the market for specialty polystyrene resin is set to expand. This growth is further fueled by advancements in manufacturing technologies, increasing awareness of material efficiency, and the rising trend of lightweight, cost-effective solutions across various applications.

The protection segment of the specialty polystyrene resin market achieved a valuation of USD 57 million in 2024, with expectations of a 2.1% CAGR over the forecast period. This segment underscores the material's value in applications necessitating added durability, impact resistance, and thermal stability. From protective casings for sensitive electronics to components in the automotive sector, specialty polystyrene resins address the critical need for reliable protection during shipping, handling, and storage. Their lightweight nature and cost-effectiveness further enhance their appeal, positioning them as a top choice for industries seeking to optimize both performance and cost.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $129 million |

| Forecast Value | $163.2 million |

| CAGR | 2.4% |

The protective packaging sector, valued at USD 76.3 million in 2024, is projected to grow at a CAGR of 2.1% over the next decade. The increasing demand for lightweight, durable, and cost-efficient packaging solutions drives the adoption of specialty polystyrene resins. These materials excel at shock absorption and thermal insulation, making them indispensable for packaging delicate items such as electronics and perishables. With the rapid expansion of e-commerce, particularly in the consumer electronics and healthcare industries, the need for robust protective packaging is intensifying. Specialty polystyrene resins are emerging as a cornerstone of this growth, delivering solutions that balance strength, reliability, and cost.

The U.S. specialty polystyrene resin market generated USD 38.9 million in 2024, with projections of a 2.5% CAGR from 2025 to 2034. The market's expansion in the U.S. is driven by the broad application of specialty polystyrene resins across industries, including packaging, electronics, automotive, and healthcare. The packaging sector, especially food packaging, benefits significantly from the material's clarity and protective properties. Furthermore, the rising focus on sustainability and recyclability is influencing market dynamics, as consumers and manufacturers increasingly prioritize environmentally friendly solutions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Growing demand for eco-friendly materials

- 3.6.1.2 Expanding applications in electronics

- 3.6.1.3 Advancements in material technology

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Environmental concerns

- 3.6.2.2 Recycling challenges

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Function, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Protection

- 5.3 Insulation

- 5.4 Lightweight

- 5.5 Durability

- 5.6 Transparency

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Application, 2021-2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Protective packaging

- 6.3 Building & construction

- 6.4 Automotive & transportation

- 6.5 Electrical & electronics

- 6.6 Healthcare

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Packaging industry

- 7.3 Electronics industry

- 7.4 Automotive industry

- 7.5 Construction industry

- 7.6 Healthcare industry

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Asahi Kasei

- 9.2 BASF

- 9.3 Braskem

- 9.4 China Petrochemical Corporation

- 9.5 ExxonMobil

- 9.6 Formosa Plastics Corporation

- 9.7 INEOS Styrolution

- 9.8 LG Chem

- 9.9 Mitsubishi Chemical Corporation

- 9.10 SABIC

- 9.11 Sinopec

- 9.12 Styron (Dow)

- 9.13 TotalEnergies