|

市場調査レポート

商品コード

1766331

DNAフォレンジックの市場機会、成長促進要因、産業動向分析、2025年~2034年予測DNA Forensics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| DNAフォレンジックの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月13日

発行: Global Market Insights Inc.

ページ情報: 英文 132 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

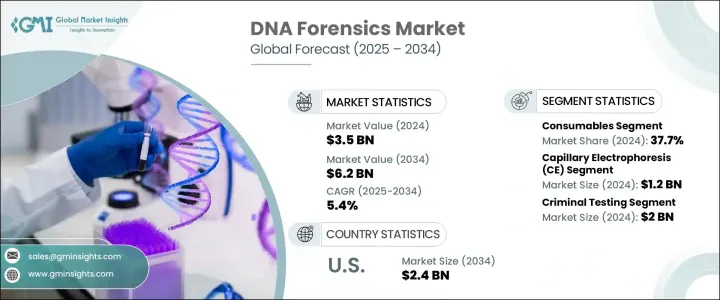

DNAフォレンジックの世界市場規模は、2024年に35億米ドルとなり、CAGR 5.4%で成長し、2034年には62億米ドルに達すると予測されています。

この着実な拡大の背景には、法的捜査や犯罪捜査における正確な識別方法や先進的分析ツールに対するニーズの高まりがあります。犯罪率が世界的に上昇を続ける中、正確なDNAプロファイリングの需要は、現代の司法制度においてますます不可欠になっています。法医学的DNA鑑定が広く採用されるようになったのは、証拠と容疑者を結びつけるその信頼性と、高い信頼性をもって法的手続きをサポートするその能力に負うところが大きいです。

さらに、科学捜査ラボにおける先端技術の統合は、分析プロセスを合理化し、当局が複雑な刑事事件に効率的に対処するのに役立っています。複数の地域の政府は、資金援助やインフラのアップグレードによって科学捜査ラボを積極的に支援しており、刑事司法システムにおけるDNAフォレンジックの利用をさらに加速させています。一方、民間セクタの参入企業は、戦略的提携、パートナーシップ、研究開発イニシアティブを通じて、イノベーションに注力し、未開拓市場への参入を拡大しています。こうした努力の積み重ねが、今後10年間の一貫した市場成長のための強固な基盤を築きつつあります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 35億米ドル |

| 予測金額 | 62億米ドル |

| CAGR | 5.4% |

DNAフォレンジックセグメントの主要企業は、技術の進歩と法医学基準の進化に対応するため、新製品開発に多額の投資を行っています。主要動向は、精度を損なうことなく効率性を高める、より携帯可能な高速DNA分析装置へのシフトです。新製品の発売に加えて、バイオテクノロジー企業は、新たな顧客基盤を獲得し、法医学ツールへのアクセス性を向上させることを目的として、新興国での事業基盤を拡大しています。バイオテクノロジー企業と公的機関との協力関係も、技術知識の交換を促進し、日常的な法医学ワークフローへの新技術の統合を合理化することで、市場の拡大に寄与しています。こうした戦略により、産業は今後も継続的な発展と競合差別化を図っていきます。

ソリューション別では、ソフトウェアセグメントにはLIMSやその他の法医学ソフトウェアツールが含まれます。これらの中で、消耗品セグメントは支配的なカテゴリーとして浮上し、2024年に37.7%の最大の収益シェアを占めています。消耗品需要の増加は、サンプル調製と検査に高品質の材料を一貫して使用する必要があるDNA分析技術の進歩に直結しています。DNAプロファイリングへの依存度が各セグメントで高まるにつれ、試薬、抽出ツール、分析用アクセサリの消費は急増を続け、同セグメントの成長を牽引しています。

市場はまた、キャピラリー電気泳動(CE)、PCR増幅、次世代シーケンス(NGS)、その他など、手法によっても区分されます。キャピラリー電気泳動は主導的地位を占め、2024年には12億米ドルの収益を上げます。高分解能で知られるCEは、劣化したサンプルでもDNA断片を正確に分離・分析できるため、法医学ラボで広く採用されています。その信頼性とスピードは、特に一刻を争う事件の解決に迅速な対応が不可欠な場合、高性能の法医学ワークフローに理想的な選択肢となります。

用途別では、市場は犯罪検査と父子・家族検査に分けられます。犯罪検査が最大のセグメントで、2024年の売上高は20億米ドルです。犯罪捜査の高度化と信頼できるDNA証拠の重視の高まりが、このセグメントを押し上げています。遺伝子検査が法執行に不可欠になるにつれ、効率的な同定と容疑者の検証を可能にする技術に対する需要が増え続けています。DNAデータベースや捜査ツールの利用拡大も、管轄区域を問わずDNAフォレンジックの必要性を高めています。

地域別では北米のが世界市場を席巻し、2024年の総売上高の42.1%以上を占めました。同地域のリーダーシップは、DNA検査技術の急速な進歩、法医学インフラへの官民の強力な投資、法的結果の正確性を向上させることの重視の高まりに後押しされています。北米の内では、米国が依然として主要な貢献国であり、2034年までに市場規模は24億米ドルに達すると予測されています。米国では、有利な施策枠組みや法医学システムの近代化を目指したイニシアチブに支えられ、州と連邦の犯罪ラボで法医学技術の導入が増加しています。

競合情勢は、Illumina、QIAGEN、Thermo Fisher Scientific、Promega、Danaherなどの大手世界企業の存在によって特徴付けられ、これらの企業は合計で市場シェア全体の50%以上を占めています。これらの企業は、迅速DNA技術、系図追跡データベース、小型検査システムなど、次世代法医学ツールの開発に積極的に取り組んでいます。研究開発への戦略的投資、研究機関との提携、新市場への進出が、各社の成長戦略の中心となっています。また、規制の合理化と迅速な承認スケジュールにより、より迅速な市場参入が可能となり、信頼性の高い法医学ソリューションに対する世界の需要の高まりに対応できるようになっています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- 産業への影響要因

- 促進要因

- 法医学プログラムに対する政府の取り組みと資金

- 父子鑑定と家族鑑定における技術的進歩

- 犯罪行為の増加

- 産業の潜在的リスク・課題

- 設備費が高め

- 新興諸国における熟練した専門家の不足

- 市場機会

- 収集時点での迅速なDNA技術の採用

- DNAデータ解釈におけるAIと機械学習の統合の拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- 技術

- 現在の技術動向

- 新興技術

- 価格分析

- 将来の市場動向

- ギャップ分析

- 特許分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡大計画

第5章 市場推定・予測、ソリューション別、2021~2034年

- 主要動向

- キット

- アナライザとシーケンサー

- ソフトウェア

- LIMS

- その他のソフトウェアタイプ

- 消耗品

第6章 市場推定・予測、方法別、2021~2034年

- 主要動向

- キャピラリー電気泳動(CE)

- 次世代シーケンス(NGS)

- PCR増幅

- その他

第7章 市場推定・予測、用途別、2021~2034年

- 主要動向

- 犯罪検査

- 父子・家族検査

第8章 市場推定・予測、地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Abbott Laboratories

- Bio-Rad Laboratories

- Danaher

- GORDIZ

- Illumina

- Laboratory Corporation of America Holdings

- LabVantage Solution

- LabWare

- Promega

- Qiagen

- Thermo Fisher Scientific

- VERISIS

The Global DNA Forensics Market was valued at USD 3.5 billion in 2024 and is estimated to grow at a CAGR of 5.4% to reach USD 6.2 billion by 2034. This steady expansion is driven by a growing need for precise identification methods and advanced analytical tools in legal and criminal investigations. As crime rates continue to rise globally, the demand for accurate DNA profiling is becoming increasingly vital in modern judicial systems. The widespread adoption of forensic DNA testing is largely attributed to its reliability in linking evidence to suspects, as well as its ability to support legal proceedings with high credibility.

Furthermore, the integration of advanced technologies in forensic labs is streamlining the analysis process and helping authorities address complex criminal cases more efficiently. Governments across multiple regions are actively supporting forensic labs with funding and infrastructure upgrades, which is further accelerating the use of DNA forensics in criminal justice systems. Meanwhile, private sector players are focusing on innovation and expanding their reach across untapped markets through strategic alliances, partnerships, and research and development initiatives. These collective efforts are creating a robust foundation for consistent market growth over the next decade.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.5 Billion |

| Forecast Value | $6.2 Billion |

| CAGR | 5.4% |

Leading companies in the DNA forensics space are investing heavily in new product development to keep pace with technological advancements and evolving forensic standards. A key trend is the shift toward more portable, high-speed DNA analysis devices that enhance efficiency without compromising accuracy. In addition to new product launches, players are expanding their operational footprints in emerging economies, aiming to capture new customer bases and improve accessibility to forensic tools. Collaborations between biotech firms and public institutions are also contributing to market expansion by fostering the exchange of technical knowledge and streamlining the integration of newer technologies into routine forensic workflows. These strategies are positioning the industry for continued advancement and competitive differentiation in the years ahead.

Based on solution, the software segment includes LIMS and other forensic software tools. Among these, the consumables segment emerged as the dominant category, accounting for the largest revenue share of 37.7% in 2024. The rising demand for consumables is directly linked to advancements in DNA analysis techniques that require consistent use of high-quality materials for sample preparation and examination. As the reliance on DNA profiling increases across sectors, the consumption of reagents, extraction tools, and analysis accessories continues to surge, driving segment growth.

The market is also segmented by method, including capillary electrophoresis (CE), PCR amplification, next-generation sequencing (NGS), and other techniques. Capillary electrophoresis held the leading position, generating a revenue of USD 1.2 billion in 2024. Known for its high-resolution capabilities, CE is widely adopted in forensic labs due to its precision in separating and analyzing DNA fragments, even in degraded samples. Its reliability and speed make it an ideal choice for high-throughput forensic workflows, especially when quick turnarounds are essential for solving time-sensitive cases.

By application, the market is divided into criminal testing and paternity and familial testing. Criminal testing represented the largest segment, with a revenue of USD 2 billion in 2024. The increasing sophistication of criminal investigations and the growing emphasis on reliable DNA evidence are pushing this segment forward. With genetic testing becoming more integral to law enforcement, demand continues to grow for technologies that enable efficient identification and suspect verification. The expanding use of DNA databases and investigative tools is also amplifying the need for DNA forensics across jurisdictions.

Regionally, North America dominated the global market, accounting for more than 42.1% of total revenue in 2024. The region's leadership is fueled by rapid advancements in DNA testing technologies, strong public and private investments in forensic infrastructure, and a growing emphasis on improving the accuracy of legal outcomes. Within North America, the United States remains the key contributor and is forecast to reach a market value of USD 2.4 billion by 2034. The U.S. is witnessing increased deployment of forensic technologies across both state and federal crime labs, supported by favorable policy frameworks and initiatives aimed at modernizing forensic systems.

The competitive landscape is marked by the presence of major global players, including Illumina, QIAGEN, Thermo Fisher Scientific, Promega, and Danaher, which collectively contribute to more than 50% of the total market share. These companies are actively engaged in the development of next-generation forensic tools, including rapid DNA technologies, genealogical tracing databases, and compact testing systems. Strategic investments in R&D, partnerships with research institutes, and expansion into new markets are central to their growth strategies. Regulatory streamlining and quicker approval timelines are also enabling faster market entry, allowing companies to meet the growing demand for reliable forensic solutions globally.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 Synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Solution

- 2.2.3 Method

- 2.2.4 Application

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Government initiatives and funds for forensic programs

- 3.2.1.2 Technological advancements in paternity and familial testing

- 3.2.1.3 Increasing criminal activities

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of equipment

- 3.2.2.2 Dearth of skilled professional in developing countries

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of rapid DNA technologies at point-of-collection

- 3.2.3.2 Growing integration of AI and machine learning in DNA data interpretation

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Patent analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

- 4.7 Key developments

- 4.7.1 Mergers & acquisitions

- 4.7.2 Partnerships & collaborations

- 4.7.3 New product launches

- 4.7.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Solution, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Kits

- 5.3 Analyzers and sequencers

- 5.4 Software

- 5.4.1 LIMS

- 5.4.2 Other software types

- 5.5 Consumables

Chapter 6 Market Estimates and Forecast, By Method, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Capillary electrophoresis (CE)

- 6.3 Next generation sequencing (NGS)

- 6.4 PCR amplification

- 6.5 Other methods

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Criminal testing

- 7.3 Paternity and familial testing

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 Bio-Rad Laboratories

- 9.3 Danaher

- 9.4 GORDIZ

- 9.5 Illumina

- 9.6 Laboratory Corporation of America Holdings

- 9.7 LabVantage Solution

- 9.8 LabWare

- 9.9 Promega

- 9.10 Qiagen

- 9.11 Thermo Fisher Scientific

- 9.12 VERISIS