サイバーセキュリティメッシュの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Cybersecurity Mesh Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1666936

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

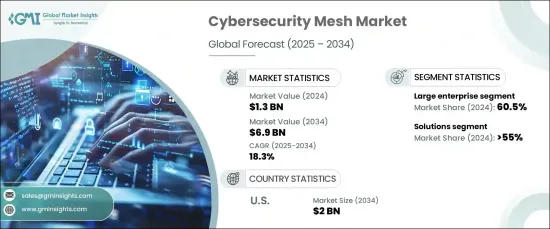

世界のサイバーセキュリティメッシュ市場は、2024年に13億米ドルとなり、2025年から2034年にかけてCAGR18.3%で成長すると予想されています。

この成長は、より高度で適応性の高いセキュリティソリューションが求められるサイバー脅威の高度化が主な要因となっています。人工知能(AI)や自動化を活用して脆弱性を悪用する現代の攻撃者から組織を守るには、従来のセキュリティ手法ではもはや不十分です。その結果、企業はリアルタイムの脅威検知、高度な分析、自動応答を提供するソリューションを求めています。この需要の変化は、クラウドやオンプレミスのリソースを含む複雑で分散化した環境を保護するために設計されたサイバーセキュリティメッシュアーキテクチャの採用を加速させています。

ハイブリッド環境とマルチクラウド環境の台頭も、市場拡大に寄与する重要な要因です。こうした環境は柔軟性、拡張性、コスト効率に優れている一方で、セキュリティ管理を複雑にしています。企業は、異なるシステム間のシームレスな相互運用性を維持しながら、さまざまなクラウドプラットフォームにわたって機密データやワークロードを保護できるセキュリティ戦略を確保する必要があります。このような複雑性の増大により、多様なエンドポイントやネットワークを監視し保護する高度なサイバーセキュリティメッシュソリューションの必要性が浮き彫りになっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 13億米ドル |

| 予測金額 | 69億米ドル |

| CAGR | 18.3% |

市場はソリューションとサービスに区分され、2024年の市場シェアはソリューションが55%以上を占め最大となりました。さまざまな環境で包括的な保護を提供する統合型分散型セキュリティソリューションへの需要が、この優位性を後押ししています。これらのソリューションは、リアルタイムの脅威検知、リスク管理、自動応答を提供するため、機密データを扱い、大規模なデジタルインフラを運用する組織にとって不可欠なものとなっています。

サービスセグメントも小規模ながら成長を遂げています。サイバーセキュリティメッシュの導入が進むにつれて、組織の既存のITエコシステム内にこれらのソリューションを効果的に統合・最適化するための専門家によるコンサルティング、実装、マネージドサービスに対する需要が生まれています。この動向は特に大企業で顕著であり、分散ネットワークや膨大なデータを保護できる拡張性と柔軟性のあるサイバーセキュリティソリューションに対するニーズから、市場シェアの60%以上を占めています。

中小企業(SME)も、市場シェアは小さいものの、サイバーセキュリティメッシュを採用しています。中小企業は、特定のニーズに合わせてカスタマイズできる、費用対効果が高く拡張性の高いソリューションを求めるようになっています。デジタルプラットフォームやクラウドベースのサービスへの依存度が高まる中、中小企業は、サイバー脅威からネットワークやエンドポイントを保護するサイバーセキュリティメッシュの価値を認識しつつあります。

米国では、複雑なITインフラを保護できる、統合された柔軟で拡張可能なセキュリティソリューションに対する需要の高まりにより、サイバーセキュリティメッシュの市場は2034年までに約20億米ドルに達すると予想されています。同業界の主要企業は、AI、機械学習、高度分析に投資することで、サイバーセキュリティ製品を改善し、金融、ヘルスケア、政府機関など、さまざまな分野の進化するニーズに対応しています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 一次調査と検証

- 一次ソース

- データマイニングソース

- 市場定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- サプライヤーの状況

- 最終用途

- 利益率分析

- 特許分析

- 技術とイノベーションの展望

- 主要ニュースと取り組み

- 規制状況

- 使用事例

- 影響要因

- 成長促進要因

- 巧妙なサイバー脅威の増加

- ハイブリッド・マルチクラウド環境の採用

- 規制コンプライアンス要件

- IoTとエッジコンピューティングの拡大

- 業界の潜在的リスク・課題

- 高い導入コスト

- 統合の複雑さ

- 成長促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- サービス

- ソリューション

第6章 市場推計・予測:展開モデル別、2021年~2034年

- 主要動向

- クラウド

- オンプレミス

- ハイブリッド

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 中小企業

- 大企業

第8章 市場推計・予測:業界別、2021年~2034年

- 主要動向

- 銀行

- IT・通信

- ヘルスケア

- 保険

- 政府機関

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Check Point

- Cisco

- CrowdStrike

- Darktrace

- F5

- FireEye

- Fortinet

- IBM

- Juniper Networks

- McAfee

- Microsoft

- Palo Alto Networks

- Proofpoint

- RSA

- SentinelOne

- Sophos

- Symantec

- Tenable

- Trend Micro

- Zscaler

目次

The Global Cybersecurity Mesh Market, valued at USD 1.3 billion in 2024, is expected to grow at a CAGR of 18.3% from 2025 to 2034. This growth is largely driven by the increasing sophistication of cyber threats, which demand more advanced and adaptive security solutions. Traditional security methods are no longer sufficient to protect organizations from modern attackers who utilize artificial intelligence (AI) and automation to exploit vulnerabilities. As a result, companies are looking for solutions that provide real-time threat detection, advanced analytics, and automated responses. This shift in demand is accelerating the adoption of cybersecurity mesh architectures, which are designed to secure complex, decentralized environments, including cloud and on-premises resources.

The rise in hybrid and multi-cloud environments is another significant factor contributing to the market's expansion. While these environments offer flexibility, scalability, and cost-efficiency, they also complicate security management. Organizations need to ensure that their security strategies can protect sensitive data and workloads across various cloud platforms while maintaining seamless interoperability between different systems. This increased complexity highlights the need for advanced cybersecurity mesh solutions to monitor and secure diverse endpoints and networks.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.3 Billion |

| Forecast Value | $6.9 Billion |

| CAGR | 18.3% |

The market is segmented into solutions and services, with the solutions segment holding the largest market share in 2024, accounting for more than 55%. The demand for integrated, decentralized security solutions that provide comprehensive protection across a variety of environments is driving this dominance. These solutions offer real-time threat detection, risk management, and automated responses, making them critical for organizations handling sensitive data and operating large-scale digital infrastructures.

The services segment, while smaller, is also experiencing growth. The increasing adoption of cybersecurity mesh has created a demand for expert consultation, implementation, and managed services to effectively integrate and optimize these solutions within organizations' existing IT ecosystems. This trend is particularly noticeable in large enterprises, which account for over 60% of the market share due to their need for scalable and flexible cybersecurity solutions that can secure distributed networks and vast volumes of data.

Small and medium-sized enterprises (SME) are also adopting cybersecurity mesh, though their market share is smaller. SME are increasingly looking for cost-effective, scalable solutions that can be customized to suit their specific needs. With a greater reliance on digital platforms and cloud-based services, SME are recognizing the value of cybersecurity mesh in safeguarding their networks and endpoints from cyber threats.

In the U.S., the market for cybersecurity mesh is expected to reach nearly USD 2 billion by 2034, driven by the growing demand for integrated, flexible, and scalable security solutions that can protect complex IT infrastructures. Major companies in the industry are investing in AI, machine learning, and advanced analytics to improve their cybersecurity offerings and meet the evolving needs of various sectors, including finance, healthcare, and government.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 End use

- 3.3 Profit margin analysis

- 3.4 Patent analysis

- 3.5 Technology & innovation landscape

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Use cases

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rise in sophisticated cyber threats

- 3.9.1.2 Adoption of hybrid and multi-cloud environments

- 3.9.1.3 Regulatory compliance requirements

- 3.9.1.4 Expansion of IOT and edge computing

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High implementation costs

- 3.9.2.2 Complexity in integration

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Services

- 5.3 Solutions

Chapter 6 Market Estimates & Forecast, By Deployment Model, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Cloud

- 6.3 On-Premises

- 6.4 Hybrid

Chapter 7 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 SME

- 7.3 Large enterprises

Chapter 8 Market Estimates & Forecast, By Vertical, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Banking

- 8.3 IT & Telecom

- 8.4 Healthcare

- 8.5 Insurance

- 8.6 Government

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Check Point

- 10.2 Cisco

- 10.3 CrowdStrike

- 10.4 Darktrace

- 10.5 F5

- 10.6 FireEye

- 10.7 Fortinet

- 10.8 IBM

- 10.9 Juniper Networks

- 10.10 McAfee

- 10.11 Microsoft

- 10.12 Palo Alto Networks

- 10.13 Proofpoint

- 10.14 RSA

- 10.15 SentinelOne

- 10.16 Sophos

- 10.17 Symantec

- 10.18 Tenable

- 10.19 Trend Micro

- 10.20 Zscaler

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日