|

市場調査レポート

商品コード

1666922

制御ケーブルの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Control Cable Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 制御ケーブルの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2024年12月24日

発行: Global Market Insights Inc.

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

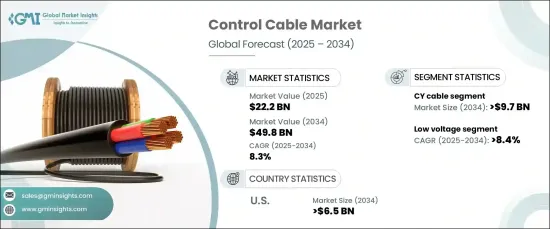

世界の制御ケーブル市場は、2024年に222億米ドルの評価額を達成し、2025年から2034年にかけてCAGR8.3%で拡大すると予測されています。

この目覚しい成長軌道は、産業、商業、および住宅部門でオートメーション技術が広く採用されていることが主な原因です。機械、装置、通信システムのデータや信号の伝送に不可欠な制御ケーブルは、現代産業の要になりつつあります。産業界が効率改善と運用コスト削減のために自動化を導入するにつれ、耐久性が高く高性能な制御ケーブルの需要が急増し続けています。

この市場は、柔軟性、耐熱性、および電磁シールドを強化する技術革新により、ケーブル技術の急速な進歩からも恩恵を受けています。これらの改良により、製造工場や発電施設などの高ストレス環境でもケーブルが確実に機能するようになりました。さらに、再生可能エネルギープロジェクトの増加、スマートインフラの推進、モノのインターネット(IoT)デバイスの普及といった世界の動向が需要を大きく促進しています。企業は厳しい安全規制を満たし、エネルギー消費量を削減しようと努めているため、現代の課題に合わせた技術的に高度な制御ケーブルへの投資が増加しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 222億米ドル |

| 予測金額 | 498億米ドル |

| CAGR | 8.3% |

アジア太平洋と中東を中心とする新興国では、建設・インフラブームが到来しており、市場の拡大がさらに加速しています。急速な都市化、政府の支援による再生可能エネルギーへの取り組み、スマートシティへの投資が、エネルギー効率の高い制御ケーブルシステムの必要性を煽っています。新興国市場は、安全で効率的かつ信頼性の高いケーブルソリューションに対する需要の高まりに対応するため、革新的な製品を開発しており、今後10年間は堅調な成長が見込まれます。

制御ケーブルタイプの中では、CYケーブルが卓越したシールド能力と電磁干渉(EMI)を最小限に抑える能力により、2034年までに97億米ドルに達すると予測されています。通信や産業オートメーションなど、正確なデータ伝送と高いシグナルインテグリティが最優先される業界では、CYケーブルが好まれています。要求の厳しい用途における汎用性と優れた性能により、CYケーブルは市場での優位性を保ち続けています。

電圧に関しては、低電圧分野は2034年までCAGR8.4%で成長すると予測されています。エネルギー効率の高いシステムへの需要の高まりとインフラプロジェクトの拡大が、低電圧ケーブルの採用を後押ししています。これらのケーブルは、制御システム、データトランスミッション、オートメーションプロセスで広く使用されており、安全性と性能の最適な融合を実現しています。IoTデバイスの普及は、スマートシティ構想と相まって、多様な産業における低電圧制御ケーブルの需要をさらに促進しています。

米国の制御ケーブル市場は、産業オートメーション、インフラ近代化、先端技術統合の動向に後押しされ、2034年までに65億米ドルを創出すると予想されています。発電、石油・ガス、通信などの主要産業では、効率を高め、操業を最適化し、ダウンタイムを最小化するために制御ケーブルを活用する傾向が強まっており、持続的な成長の舞台となっています。

目次

第1章 調査手法と調査範囲

- 市場の定義

- 基本推定と計算

- 予測計算

- データソース

- 一次

- 二次

- 有償

- 公開

第2章 業界洞察

- 業界エコシステム分析

- 規制状況

- 業界への影響要因

- 成長促進要因

- 業界の潜在的リスク・課題

- 成長ポテンシャル分析

- ポーター分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- PESTEL分析

第3章 競合情勢

- 戦略ダッシュボード

- イノベーションと持続可能性の展望

第4章 市場規模・予測:ケーブルタイプ別、2021年~2034年

- 主要動向

- CYケーブル

- YYケーブル

- SYケーブル

- LiYCYケーブル

- LiYYケーブル

- LiHHケーブル

- LiHCHケーブル

第5章 市場規模・予測:電圧別、2021年~2034年

- 主要動向

- 低

- 中

- 高

第6章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- コンベアシステム

- 組立リンク

- ロボット生産ライン

- 空調システム

- 機械

- 工具製造

- 配電

第7章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- イタリア

- ロシア

- スペイン

- アジア太平洋

- 中国

- オーストラリア

- インド

- 日本

- 韓国

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

- 南アフリカ

- エジプト

- ラテンアメリカ

- ブラジル

- アルゼンチン

第8章 企業プロファイル

- Belden

- Brugg Cables

- Eland Cables

- Furukawa Electric

- KEC International

- KEI Industries

- Klaus Faber

- LS Cable &System

- Nexans

- NKT

- Prysmian Group

- RR Kabel

- Southwire Company

- Sumitomo Electric Industries

- Universal Cables

The Global Control Cable Market achieved a valuation of USD 22.2 billion in 2024 and is anticipated to expand at a CAGR of 8.3% from 2025 to 2034. This impressive growth trajectory is largely attributed to the widespread adoption of automation technologies across industrial, commercial, and residential sectors. Control cables, which are indispensable for transmitting data and signals in machinery, equipment, and communication systems, are becoming a cornerstone of modern industries. As industries embrace automation to improve efficiency and reduce operational costs, the demand for durable, high-performance control cables continues to surge.

The market is also benefiting from rapid advancements in cable technology, with innovations enhancing flexibility, thermal resistance, and electromagnetic shielding. These improvements enable cables to perform reliably in high-stress environments, such as manufacturing plants and power generation facilities. Moreover, global trends like the rise of renewable energy projects, the push for smart infrastructure, and the proliferation of Internet of Things (IoT) devices are significantly driving demand. As businesses strive to meet stringent safety regulations and reduce energy consumption, they are increasingly investing in technologically advanced control cables tailored to modern challenges.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $22.2 Billion |

| Forecast Value | $49.8 Billion |

| CAGR | 8.3% |

Emerging economies, particularly in Asia-Pacific and the Middle East, are experiencing a construction and infrastructure boom, further amplifying the market's expansion. Rapid urbanization, government-backed renewable energy initiatives, and investments in smart cities are fueling the need for energy-efficient control cable systems. Manufacturers are responding by developing innovative products to meet the growing demand for safe, efficient, and reliable cabling solutions, positioning the market for robust growth over the next decade.

Among cable types, CY cables are forecasted to reach USD 9.7 billion by 2034, driven by their exceptional shielding capabilities and ability to minimize electromagnetic interference (EMI). Industries like telecommunications and industrial automation, where precise data transmission and high signal integrity are paramount, have made CY cables a preferred choice. Their versatility and superior performance in demanding applications ensure their continued dominance in the market.

In terms of voltage, the low voltage segment is projected to grow at a CAGR of 8.4% through 2034. The rising demand for energy-efficient systems and expanding infrastructure projects have propelled the adoption of low voltage cables. These cables are widely used in control systems, data transmission, and automation processes, delivering an optimal blend of safety and performance. The proliferation of IoT devices, coupled with smart city initiatives, is further driving demand for low voltage control cables across diverse industries.

The US control cable market is expected to generate USD 6.5 billion by 2034, bolstered by trends in industrial automation, infrastructure modernization, and advanced technology integration. Key industries such as power generation, oil and gas, and telecommunications are increasingly leveraging control cables to enhance efficiency, optimize operations, and minimize downtime, setting the stage for sustained growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Industry Insights

- 2.1 Industry ecosystem analysis

- 2.2 Regulatory landscape

- 2.3 Industry impact forces

- 2.3.1 Growth drivers

- 2.3.2 Industry pitfalls & challenges

- 2.4 Growth potential analysis

- 2.5 Porter's analysis

- 2.5.1 Bargaining power of suppliers

- 2.5.2 Bargaining power of buyers

- 2.5.3 Threat of new entrants

- 2.5.4 Threat of substitutes

- 2.6 PESTEL analysis

Chapter 3 Competitive landscape, 2024

- 3.1 Strategic dashboard

- 3.2 Innovation & sustainability landscape

Chapter 4 Market Size and Forecast, By Cable Type, 2021 – 2034 (USD Million, ‘000 Tonnes)

- 4.1 Key trends

- 4.2 CY cable

- 4.3 YY cable

- 4.4 SY cable

- 4.5 LiYCY cable

- 4.6 LiYY cable

- 4.7 LiHH cable

- 4.8 LiHCH cable

Chapter 5 Market Size and Forecast, By Voltage, 2021 – 2034 (USD Million, ‘000 Tonnes)

- 5.1 Key trends

- 5.2 Low

- 5.3 Medium

- 5.4 High

Chapter 6 Market Size and Forecast, By Application, 2021 – 2034 (USD Million, ‘000 Tonnes)

- 6.1 Key trends

- 6.2 Conveyor systems

- 6.3 Assembly links

- 6.4 Robotics production lines

- 6.5 Air conditioning systems

- 6.6 Machine

- 6.7 Tool manufacturing

- 6.8 Power distribution

Chapter 7 Market Size and Forecast, By Region, 2021 – 2034 (USD Million, ‘000 Tonnes)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 France

- 7.3.3 Germany

- 7.3.4 Italy

- 7.3.5 Russia

- 7.3.6 Spain

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 India

- 7.4.4 Japan

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Turkey

- 7.5.4 South Africa

- 7.5.5 Egypt

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 Belden

- 8.2 Brugg Cables

- 8.3 Eland Cables

- 8.4 Furukawa Electric

- 8.5 KEC International

- 8.6 KEI Industries

- 8.7 Klaus Faber

- 8.8 LS Cable & System

- 8.9 Nexans

- 8.10 NKT

- 8.11 Prysmian Group

- 8.12 RR Kabel

- 8.13 Southwire Company

- 8.14 Sumitomo Electric Industries

- 8.15 Universal Cables