|

市場調査レポート

商品コード

1666917

皮膚科機器の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Dermatology Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 皮膚科機器の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2024年12月20日

発行: Global Market Insights Inc.

ページ情報: 英文 135 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

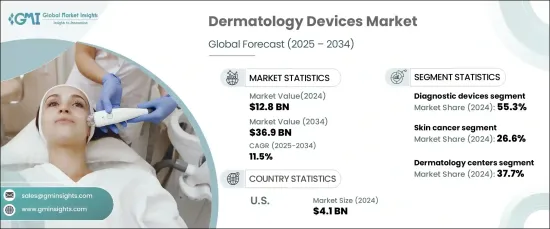

皮膚科機器の世界市場は、2024年に128億米ドルとなり、2025年から2034年にかけて11.5%という驚異的なCAGRで成長すると予想されています。

この成長は主に、皮膚がんを含む皮膚疾患の有病率の増加や、新興国におけるスキンケアへの注目の高まりによるものです。さらに、皮膚科機器の技術的進歩がこの市場の拡大に重要な役割を果たしている一方、先進地域では美容整形に対する需要が高まっています。消費者が肌の健康と美容治療を優先し続ける中、市場は持続的な成長を遂げると思われます。

同市場は診断機器と治療機器に分類され、いずれも世界的に増加する皮膚関連の健康問題に対処する上で重要な役割を果たしています。診断機器は、早期かつ正確な発見に不可欠であり、画像診断システム、皮膚鏡、生検ツールなどが含まれます。一方、治療機器には、光治療システム、レーザー、マイクロダーマブレーション装置、凍結療法機器、電気外科機器、脂肪吸引機器が含まれます。2024年には、診断機器が市場全体の55.3%を占め、市場を独占しました。これは、湿疹や皮膚がんなどの症状をタイムリーに特定する必要性が高まっているためです。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 128億米ドル |

| 予測金額 | 369億米ドル |

| CAGR | 11.5% |

用途別では、皮膚科機器は皮膚がん、肌の若返り、脱毛、ボディライン、乾癬、その他さまざまな皮膚疾患の治療に広く使用されています。皮膚がん分野は2024年に市場をリードし、26.6%のシェアを占めました。これは、皮膚がん患者の世界の増加により、信頼性の高い診断・治療ツールの需要が高まっているためです。先進的な皮膚科機器は、がん性病変と前がん性病変の両方を特定するのに不可欠であり、早期介入と患者の転帰改善を可能にします。

米国の皮膚科機器市場は、2024年に41億米ドルとなり、依然として世界最大です。この優位性は、米国における黒色腫および黒色腫以外の皮膚がんの発生率の高さと、広範な意識向上プログラムおよび皮膚がん予防の取り組みが相まってもたらされたものです。さらに、米国FDAによる先進的な皮膚科機器の承認は、最先端の診断・治療ソリューションの提供を強化し、市場の継続的な成長と革新に寄与しています。皮膚科医療への需要が高まるにつれ、米国はこの急拡大する市場において重要なプレーヤーであり続けると考えられています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- 業界への影響要因

- 成長促進要因

- 世界の皮膚関連疾患および皮膚がんの罹患率の上昇

- 新興諸国におけるスキンケアへの支出の増加

- スキンケア機器の技術進歩

- 先進諸国における美容施術の需要増加

- 業界の潜在的リスク・課題

- 過剰な機器コスト

- 厳しい規制状況

- 成長促進要因

- 成長可能性分析

- 規制状況

- 技術的展望

- 特許分析

- 今後の市場動向

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業市場シェア分析

- 主要市場企業の競合分析

- 競合のポジショニングマトリックス

- 戦略展望

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 診断機器

- 画像診断機器

- 皮膚内視鏡

- 生検装置

- 治療機器

- 光治療器(LED治療)

- レーザー

- マイクロダーマブレーション機器

- 凍結療法機器

- 電気手術機器

- 脂肪吸引機器

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 皮膚がん

- 肌の若返り

- 脱毛

- ボディラインと肌の引き締め

- 乾癬

- その他の用途

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 皮膚科センター

- 病院

- クリニック

- その他の最終用途

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Alma Lasers(Fosun Pharma)

- Ambicare Health

- Bausch Health Companies

- Biolitec

- Bruker Corporation

- Candela Corporation

- Canfield Scientific

- Carl Zeiss

- Cutera

- Cynosure Lutronic

- Genesis Biosystems

- Heine Optotechnik

- Hologic

- Image Derm

- Leica Microsystems

- Lumenis

- Michelson Diagnostics(VivoSight)

- Olympus Corporation

The Global Dermatology Devices Market was valued at USD 12.8 billion in 2024 and is expected to grow at an impressive CAGR of 11.5% from 2025 to 2034. This growth is primarily driven by the increasing prevalence of skin diseases, including skin cancer, as well as the rising focus on skincare in emerging economies. Additionally, technological advancements in dermatology devices are playing a key role in the expansion of this market, while developed regions are seeing heightened demand for cosmetic procedures. As consumers continue to prioritize skin health and aesthetic treatments, the market is set for sustained growth.

The market is categorized into diagnostic and treatment devices, both of which serve critical roles in addressing the increasing incidence of skin-related health concerns globally. Diagnostic devices are essential for early and accurate detection and include imaging systems, dermatoscopes, and biopsy tools. Meanwhile, treatment devices encompass light therapy systems, lasers, microdermabrasion units, cryotherapy tools, electrosurgical equipment, and liposuction devices. In 2024, diagnostic devices dominated the market, accounting for 55.3% of the total share. This is attributed to the growing need for timely identification of conditions such as eczema and skin cancer, as early detection is key to successful treatment outcomes.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $12.8 Billion |

| Forecast Value | $36.9 Billion |

| CAGR | 11.5% |

In terms of application, dermatology devices are widely used in the treatment of skin cancer, skin rejuvenation, hair removal, body contouring, psoriasis, and various other dermatological conditions. The skin cancer segment led the market in 2024, commanding a significant 26.6% share. This is due to the global rise in skin cancer cases, driving the demand for reliable diagnostic and treatment tools. Advanced dermatology devices are indispensable in identifying both cancerous and precancerous lesions, allowing for early intervention and improved patient outcomes.

The U.S. dermatology devices market, with a valuation of USD 4.1 billion in 2024, remains the largest in the world. This dominance is driven by the high rates of melanoma and non-melanoma skin cancers in the U.S., combined with extensive awareness programs and skin cancer prevention initiatives. Furthermore, the approval of advanced dermatology devices by the U.S. FDA has bolstered the availability of cutting-edge diagnostic and treatment solutions, contributing to the market's continued growth and innovation. As the demand for dermatological care intensifies, the U.S. will remain a key player in this rapidly expanding market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of skin associated diseases and skin cancer worldwide

- 3.2.1.2 Increasing expenditure on skin care in developing countries

- 3.2.1.3 Technological advancements in skincare devices

- 3.2.1.4 Growing demand for cosmetic procedures in developed countries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Excessive equipment cost

- 3.2.2.2 Stringent regulatory landscape

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.6 Patent analysis

- 3.7 Future market trends

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy outlook

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Diagnostic devices

- 5.2.1 Imaging devices

- 5.2.2 Dermatoscopes

- 5.2.3 Biopsy devices

- 5.3 Treatment devices

- 5.3.1 Light therapy devices (LED therapy)

- 5.3.2 Lasers

- 5.3.3 Microdermabrasion devices

- 5.3.4 Cryotherapy devices

- 5.3.5 Electrosurgical equipment

- 5.3.6 Liposuction devices

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Skin cancer

- 6.3 Skin rejuvenation

- 6.4 Hair removal

- 6.5 Body contouring and skin tightening

- 6.6 Psoriasis

- 6.7 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Dermatology centers

- 7.3 Hospitals

- 7.4 Clinics

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Alma Lasers (Fosun Pharma)

- 9.2 Ambicare Health

- 9.3 Bausch Health Companies

- 9.4 Biolitec

- 9.5 Bruker Corporation

- 9.6 Candela Corporation

- 9.7 Canfield Scientific

- 9.8 Carl Zeiss

- 9.9 Cutera

- 9.10 Cynosure Lutronic

- 9.11 Genesis Biosystems

- 9.12 Heine Optotechnik

- 9.13 Hologic

- 9.14 Image Derm

- 9.15 Leica Microsystems

- 9.16 Lumenis

- 9.17 Michelson Diagnostics (VivoSight)

- 9.18 Olympus Corporation