鉱業用浮遊化学品の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Mining Flotation Chemicals Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 235 Pages

- 納期

- 2~3営業日

- 商品コード

- 1666913

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

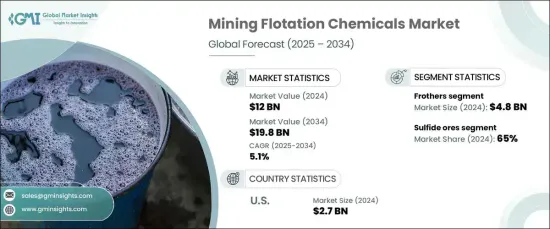

世界の鉱業用浮遊化学品市場は、2024年に120億米ドルとなり、2025年から2034年にかけてCAGR5.1%の堅調な成長が見込まれています。

これらの化学薬品は、鉱物分離において不可欠な役割を果たし、浮遊プロセスにおいて重要な薬剤として作用します。スラリーの表面に安定した泡層を形成することで、鉱物粒子を気泡に付着させ、効率的な抽出を促進します。この技術は、鉱業分野における進歩の最前線にあり続け、建設からテクノロジーまで幅広い産業を支えています。

鉱業用浮遊化学品の需要は、急速な工業化とインフラ開発により、世界中でベースメタルと鉱物のニーズが高まっていることに後押しされています。各国が大規模プロジェクトに投資し続ける中、効率的で持続可能な採掘方法がますます重視されるようになっています。浮遊化学品は、鉱物回収の最適化、廃棄物の削減、全体的な処理効率の向上に不可欠です。鉱物処理技術の革新が進む中、同市場は世界中の採鉱活動の増加から生じる機会を活用する態勢を整えています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 120億米ドル |

| 予測金額 | 198億米ドル |

| CAGR | 5.1% |

市場は、フロザー、コレクター、活性剤、分散剤、特殊化学品など、化学品タイプによって区分されます。フロザーは市場で最大のシェアを占め、収益に大きく貢献しています。鉱物の分離を促進する泡を作る役割があり、なくてはならない存在となっています。もう一つの主要カテゴリーである捕集剤は、気泡への鉱物の付着を促進し、浮遊プロセスでの高い効率を確保するため、需要が高まっています。その他の特殊化学品もまた、鉱業特有の課題に対処する上で極めて重要な役割を担っており、この分野での採用をさらに後押ししています。

鉱石タイプ別に分類すると、市場には硫化鉱と非硫化鉱があります。硫化鉱石は、採掘作業で広く使われているため、現在のところ硫化鉱石が圧倒的なシェアを占めています。しかし、非硫化鉱はその多様な産業用途のために需要が急増しています。非硫化鉱に含まれるリン酸塩やカリのような鉱物は、農業での肥料やその他の工業プロセスでますます使用されるようになっています。鉱業会社は、こうした経済的に実行可能な代替資源を活用するために資源採掘を多様化しており、このセグメントの成長をさらに促進しています。

米国では、鉱業用浮遊化学品市場は2024年時点で27億米ドルと評価されており、堅調な国内鉱業部門によって着実な成長が後押しされています。輸入鉱物への依存を減らし、国内採掘を支援しようという国の動きが大きな推進力となっています。鉱物処理技術の進歩は、鉱業インフラへの多額の投資と相まって、浮遊化学品の採用を促進しています。ハイテク産業に不可欠な重要鉱物は注目の的であり、持続可能な採掘方法を促進する政策が市場拡大をさらに加速させています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 一次

- 二次

- 有料ソース

- 公的ソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 変革

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュース

- 規制状況

- 影響要因

- 成長促進要因

- ベースメタルと貴金属の需要増加

- 鉱石品位の低下

- 浮選技術の進歩

- 業界の潜在的リスク・課題

- 原料価格の変動

- 代替品との競合

- 成長促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業市場シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:化学品タイプ別、2021年~2034年

- 主要動向

- フロザー

- コレクター

- 活性剤

- 分散剤

- その他(減圧剤、表面改質剤)

第6章 市場推計・予測:鉱石タイプ別、2021年~2034年

- 主要動向

- 硫化鉱

- 非硫化鉱

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 卑金属鉱業

- 貴金属鉱業

- 産業鉱物の採掘

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 銅鉱業

- 金・銀鉱山

- ニッケル・白金族金属鉱業

- 亜鉛鉱業

- その他(鉄鉱石、石炭鉱業)

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Arkema

- BASF SE

- Beijing Hengju

- Cheminova

- Chevron Phillips Chemical

- Clariant

- Cytec Industries

- Dow

- Huntsman

- Kemira

- NASACO

- Nouryon

- Rhodia

- Solvay

- Wacker Chemie

目次

The Global Mining Flotation Chemicals Market, valued at USD 12 billion in 2024, is expected to grow at a robust CAGR of 5.1% from 2025 to 2034. These chemicals play an indispensable role in mineral separation, acting as critical agents in the flotation process. By forming a stable froth layer on the surface of the slurry, they enable mineral particles to adhere to air bubbles, facilitating efficient extraction. This technology remains at the forefront of advancements in the mining sector, supporting industries ranging from construction to technology.

The demand for mining flotation chemicals is fueled by the growing need for base metals and minerals worldwide, driven by rapid industrialization and infrastructure development. As nations continue to invest in large-scale projects, the emphasis on efficient and sustainable extraction methods intensifies. Flotation chemicals are integral to optimizing mineral recovery, reducing waste, and improving overall processing efficiency. With ongoing innovations in mineral processing technologies, the market is poised to capitalize on opportunities stemming from increasing mining activities across the globe.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $12 Billion |

| Forecast Value | $19.8 Billion |

| CAGR | 5.1% |

The market is segmented by chemical types, including frothers, collectors, activators, dispersants, and specialty chemicals. Frothers command the largest share of the market, contributing significantly to revenue. Their role in creating froth that facilitates mineral separation makes them indispensable. Collectors, another key category, are experiencing rising demand as they enhance the attachment of minerals to air bubbles, ensuring higher efficiency during the flotation process. Other specialty chemicals also play pivotal roles in addressing unique mining challenges, further boosting their adoption across the sector.

When categorized by ore type, the market includes sulfide ores and non-sulfide ores. Sulfide ores currently dominate, thanks to their prevalence in mining operations. However, non-sulfide ores are witnessing a surge in demand due to their diverse industrial applications. Minerals like phosphate and potash, found in non-sulfide ores, are increasingly used in agriculture for fertilizers and in other industrial processes. Mining companies are diversifying resource extraction to capitalize on these economically viable alternatives, further driving growth in this segment.

In the United States, the mining flotation chemicals market is valued at USD 2.7 billion as of 2024, with steady growth bolstered by a strong domestic mining sector. The nation's push to reduce reliance on imported minerals and support domestic extraction has been a significant driver. Advancements in mineral processing technologies, coupled with substantial investments in mining infrastructure, are fostering the adoption of flotation chemicals. Critical minerals, essential for high-tech industries, are a focal point, with policies promoting sustainable mining practices further accelerating market expansion.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing demand for base and precious metals

- 3.6.1.2 Declining ore grades

- 3.6.1.3 Advancements in flotation technologies

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Price volatility of raw material

- 3.6.2.2 Competition from substitute

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Chemical Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Frothers

- 5.3 Collectors

- 5.4 Activators

- 5.5 Dispersants

- 5.6 Others (depressants, surface modifiers)

Chapter 6 Market Estimates & Forecast, By Ore Type, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Sulfide ores

- 6.3 Non-sulfide ores

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Base metal mining

- 7.3 Precious metal mining

- 7.4 Industrial minerals mining

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Copper mining

- 8.3 Gold and silver mining

- 8.4 Nickel and platinum group metals mining

- 8.5 Zinc mining

- 8.6 Others (iron ore, coal mining)

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Arkema

- 10.2 BASF SE

- 10.3 Beijing Hengju

- 10.4 Cheminova

- 10.5 Chevron Phillips Chemical

- 10.6 Clariant

- 10.7 Cytec Industries

- 10.8 Dow

- 10.9 Huntsman

- 10.10 Kemira

- 10.11 NASACO

- 10.12 Nouryon

- 10.13 Rhodia

- 10.14 Solvay

- 10.15 Wacker Chemie

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 235 Pages

- 納期

- 2~3営業日