|

市場調査レポート

商品コード

1666909

自動車予測技術市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Automotive Predictive Technology Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車予測技術市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2024年12月02日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

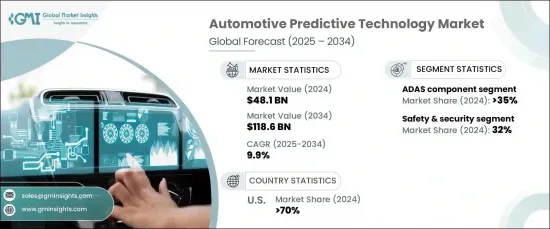

世界の自動車予測技術市場は、2024年に481億米ドルと評価され、2025年から2034年にかけて9.9%のCAGRで堅調な成長を遂げると予想されています。 この成長の促進要因は、ADAS(先進安全機能)と運転支援システムに対する需要の高まりです。

自動車メーカーは、交通パターン、ドライバーの行動、車両性能などのリアルタイム・データを分析することにより、車両の安全性を高め、事故を防止し、全体的な運転体験を改善するために、加速度的に予測技術を採用しています。また、予知保全も大きな支持を得ており、潜在的な問題を早期に発見することで予期せぬ故障を防ぎ、車両の信頼性を高めています。

市場拡大に拍車をかけている主な要因は、電気自動車(EV)の導入が増加していることです。自動車産業がより持続可能な社会を目指す中、EVの性能を最適化し、バッテリーの寿命を延ばすためには、予測技術が不可欠となっています。これらの技術は、高度な分析を用いてバッテリーの消耗を予測し、充電習慣を監視し、エネルギー効率を高めることで、EVの最適な性能と寿命を確保します。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 481億米ドル |

| 予測金額 | 1,186億米ドル |

| CAGR | 9.9% |

市場のハードウェア・セグメントには、ADASコンポーネント、OBDデバイス、テレマティクス・システムが含まれます。2024年にはADASコンポーネントが市場シェアの35%を占め、2034年までに480億米ドルを創出すると予測されています。自動化とより安全なドライビング・ソリューションに対する需要の高まりが、アダプティブ・クルーズ・コントロール、レーン・アシスト、衝突検知などのADAS機能の統合につながっています。センサー、カメラ、レーダー、人工知能を活用することで、これらの技術は車両がリアルタイムでリスクを予測・軽減することを可能にし、交通安全を大幅に強化します。

市場はまた、予知保全、車両健康モニタリング、安全・セキュリティ、運転パターン分析などの用途別にも区分されます。2024年には、交通事故死者数の減少に世界的に注目が集まっていることを背景に、安全・セキュリティ分野が市場シェアの32%を占めています。ヒューマンエラーが交通事故の主な要因であることから、予測技術は危険を予測し、全体的な交通安全を向上させる上で極めて重要になっています。

米国の自動車予測技術市場は2024年に圧倒的な70%のシェアで世界市場をリードしました。同国は自律走行車(AV)と先進予測システムの開発でリーダーシップを発揮しており、自動車メーカーやハイテク企業から多額の投資を集めています。予測技術はAVにとって極めて重要で、センサーやカメラからのデータを処理して複雑な環境をナビゲートし、衝突を回避し、迅速かつ的確な判断を下すことを可能にします。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場範囲と定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 自動車OEM

- テクノロジープロバイダー

- データ分析およびクラウドサービスプロバイダー

- 最終用途

- サプライヤーの状況

- 利益率分析

- テクノロジー&イノベーション・情勢

- 特許分析

- 主要ニュースと取り組み

- 規制状況

- ケーススタディ

- 影響要因

- 促進要因

- 自動車の安全性と効率性に対する需要の高まり

- パーソナライズされたコネクテッド・エクスペリエンスへの需要

- 人工知能(AI)と機械学習(ML)の急速な統合

- コネクテッドカーの採用増加

- 業界の潜在的リスク&課題

- データプライバシーとセキュリティへの懸念

- 高い導入コスト

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 予知保全

- 車両ヘルスモニタリング

- 安全・セキュリティ

- 走行パターン分析

- その他

第6章 市場推計・予測:展開別、2021年~2034年

- 主要動向

- オンプレミス

- クラウド

第7章 市場推計・予測:ハードウェア別、2021年~2034年

- 主要動向

- ADASコンポーネント

- OBD

- テレマティクス

第8章 市場推計・予測:車種別、2021年~2034年

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV車

- 商用車

- 小型商用車(LCV)

- 大型商用車(HCV)

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Aisin

- Aptiv

- Bosch

- Continental

- Garrett Motion

- HARMAN

- Honeywell

- Infineon

- Intel

- Lear

- Magna

- Mobileye

- NVIDIA

- NXP

- Qualcomm

- Renesas

- Siemens

- Valeo

- Visteon

- ZF Friedrichshafen

The Global Automotive Predictive Technology Market, valued at USD 48.1 billion in 2024, is expected to experience robust growth at a CAGR of 9.9% from 2025 to 2034. This growth is driven by the increasing demand for advanced safety features and driver assistance systems. Automakers are adopting predictive technologies at an accelerating pace to enhance vehicle safety, prevent accidents, and improve overall driving experiences by analyzing real-time data such as traffic patterns, driver behavior, and vehicle performance. Predictive maintenance has also gained significant traction, allowing for early detection of potential issues to prevent unexpected breakdowns and ensure greater vehicle reliability.

A key factor fueling market expansion is the rise in electric vehicle (EV) adoption. As the automotive industry moves toward greater sustainability, predictive technologies are becoming essential for optimizing EV performance and extending battery life. These technologies use advanced analytics to forecast battery wear, monitor charging habits, and enhance energy efficiency, ensuring optimal performance and longevity of EVs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $48.1 Billion |

| Forecast Value | $118.6 Billion |

| CAGR | 9.9% |

The hardware segment of the market includes ADAS components, OBD devices, and telematics systems. In 2024, ADAS components accounted for 35% of the market share and are expected to generate USD 48 billion by 2034. The increasing demand for automation and safer driving solutions has led to the integration of ADAS features such as adaptive cruise control, lane assist, and collision detection. By leveraging sensors, cameras, radar, and artificial intelligence, these technologies enable vehicles to predict and mitigate risks in real-time, significantly enhancing road safety.

The market is also segmented by applications, including predictive maintenance, vehicle health monitoring, safety and security, and driving pattern analysis. In 2024, the safety and security segment held 32% of the market share, driven by the global focus on reducing traffic fatalities. With human error being a major factor in road accidents, predictive technologies have become crucial in anticipating hazards and improving overall road safety.

The U.S. automotive predictive technology market led the global market with a dominant 70% share in 2024. The country's leadership in developing autonomous vehicles (AVs) and advanced predictive systems has attracted significant investments from automakers and tech companies alike. Predictive technology is crucial for AVs, enabling them to process data from sensors and cameras to navigate complex environments, avoid collisions, and make quick, precise decisions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Automotive OEMs

- 3.1.2 Technology providers

- 3.1.3 Data analytics & cloud service providers

- 3.1.4 End use

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Case study

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing demand for vehicle safety & efficiency

- 3.9.1.2 Demand for personalized & connected experiences

- 3.9.1.3 Rapid integration of Artificial Intelligence (AI) and Machine Learning (ML)

- 3.9.1.4 Rising adoption of connected cars

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Data privacy & security concerns

- 3.9.2.2 High implementation costs

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

CHAPTER 4 : Competitive Landscape

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Predictive maintenance

- 5.3 Vehicle health monitoring

- 5.4 Safety & security

- 5.5 Driving pattern analysis

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Deployment, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 On-premise

- 6.3 Cloud

Chapter 7 Market Estimates & Forecast, By Hardware, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 ADAS component

- 7.3 OBD

- 7.4 Telematics

Chapter 8 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Passenger vehicle

- 8.2.1 Hatchback

- 8.2.2 Sedan

- 8.2.3 SUVs

- 8.3 Commercial vehicles

- 8.3.1 Light Commercial Vehicles (LCVs)

- 8.3.2 Heavy Commercial Vehicles (HCVs)

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 94.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Aisin

- 10.2 Aptiv

- 10.3 Bosch

- 10.4 Continental

- 10.5 Garrett Motion

- 10.6 HARMAN

- 10.7 Honeywell

- 10.8 Infineon

- 10.9 Intel

- 10.10 Lear

- 10.11 Magna

- 10.12 Mobileye

- 10.13 NVIDIA

- 10.14 NXP

- 10.15 Qualcomm

- 10.16 Renesas

- 10.17 Siemens

- 10.18 Valeo

- 10.19 Visteon

- 10.20 ZF Friedrichshafen