クラウドネイティブアプリケーション保護プラットフォーム市場の機会、成長促進要因、業界動向分析、2025年~2034年の予測

Cloud-native Application Protection Platform (CNAPP) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1666894

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

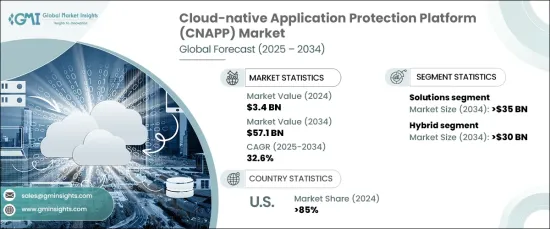

クラウドネイティブアプリケーション保護プラットフォームの世界市場は、2024年に34億米ドルと評価され、2025年から2034年にかけて驚異的なCAGR 32.6%で拡大すると予測されています。

この成長は主に、クラウドインフラストラクチャを標的としたフィッシングの試みやサイバー攻撃の巧妙化によってもたらされます。企業がコンテナ化されたアプリケーションや複雑なクラウド構成を備えたクラウドネイティブ環境を採用するにつれ、新たなセキュリティ課題が浮上しています。これには、設定の誤りや複雑化する攻撃対象といった問題が含まれ、企業は高度な脅威にさらされやすくなっています。これに対応するため、CNAPPソリューションは最新のクラウドインフラストラクチャの要求に応えるべく進化しており、進化するサイバーリスクに対する待望のシールドを提供しています。

市場はソリューションとサービスに区分され、ソリューションが最大のシェアを占め、2024年には市場の70%を占めています。このセグメントは、2034年までに350億米ドルを生み出すと予想されています。脅威がエスカレートし続ける中、CNAPPソリューションは世界データベースと集合的インテリジェンスを統合することで、最先端の脅威インテリジェンスを取り入れています。これらのプラットフォームは、脆弱性を予測し、新たな脅威が被害をもたらす前にプロアクティブに対処するのに役立つ予測セキュリティ・モデルへと移行しつつあります。コンテクストを認識するツールは、リスク評価を強化し、セキュリティ侵害により機敏に対応するために、クロスドメインの脅威相関を提供し、人気を集めています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 34億米ドル |

| 予測金額 | 571億米ドル |

| CAGR | 32.6% |

導入タイプ別に見ると、市場はハイブリッド環境とマルチクラウド環境に分かれます。ハイブリッド・セグメントは、オンプレミスとクラウドの両インフラで一貫したセキュリティ・ガバナンスの必要性が高まっていることを背景に、2034年までに300億米ドルに達すると予測されます。企業がマルチクラウド戦略を採用するにつれ、統合セキュリティ管理ツールの需要が急増しています。これらのツールは一元的な可視性を確保し、企業がコンプライアンスを実施し、多様なシステムにわたるリスクを効果的に管理することを可能にします。CNAPPプラットフォームは、従来のデータセンター・セキュリティと最新のクラウド・ネイティブ・アーキテクチャのギャップを埋めるために進化しており、コンプライアンスやリスク管理基準を損なうことなく、セキュリティ対策のシームレスな統合を実現しています。

米国がCNAPP市場を独占し、2024年にはシェアの85%を占めています。これはサイバー脅威の増大と連邦政府の厳しい規制が後押ししています。このような規制の厳しい環境では、組織は継続的な検証、最小権限アクセス、きめ細かな可視性を重視するセキュリティフレームワークを優先する傾向が強まっています。企業が潜在的なサイバー攻撃から分散型クラウドエコシステムを保護するために、適応型認証ツールやリアルタイムのリスク評価機能への投資が一般的になりつつあります。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- クラウドサービスプロバイダー

- テクノロジープロバイダー

- アプリケーション開発者

- システム・インテグレーター

- 最終用途

- 利益率分析

- テクノロジーの差別化要因

- 統一プラットフォーム・アプローチ

- DevSecOpsの統合

- ゼロ・トラスト・セキュリティ・モデル

- ランタイム・アプリケーション・セルフプロテクション(RASP)

- その他

- 主なニュースと取り組み

- 特許分析

- 規制状況

- 影響要因

- 促進要因

- クラウドベースのプラットフォームの採用拡大

- サイバーセキュリティの脅威の高まり

- 厳しいデータ保護規制

- DevSecOpsプラクティスの採用

- 業界の潜在的リスク&課題

- 複雑なクラウド環境

- パフォーマンスのオーバーヘッド

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ソリューション

- アイデンティティベースのセキュリティとクラウドインフラのエンタイトルメント管理(CIEM)

- クラウドワークロード保護CWPP

- コードとしてのインフラストラクチャ(IAC)

- Kubernetesセキュリティポスチャ管理(KSPM)

- クラウド・セキュリティ・ポスチャ管理(CSPM)

- サービス

- プロフェッショナル・サービス

- マネージドサービス

第6章 市場推計・予測:クラウド別、2021年~2034年

- 主要動向

- ハイブリッドクラウド

- マルチクラウド

第7章 市場推計・予測:組織規模別、2021年~2034年

- 主要動向

- 中小企業

- 大企業

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 小売

- BFSI

- ヘルスケア

- 政府機関

- IT &テレコム

- 製造業

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Aqua Security

- Checkpoint Security

- CrowdStrike

- Data Theorem

- Fortinet

- LaceWorks

- McAfee

- Orca Security

- Palo Alto Networks

- Qualys

- Runecast Solutions

- Skyhigh Security

- Sonrai

- Sysdig

- Tenable

- Tigera

- Trend Micro

- Uptycs

- Wiz.io

- Zscaler

- Others

目次

The Global Cloud-Native Application Protection Platform Market, valued at USD 3.4 billion in 2024, is projected to expand at a staggering CAGR of 32.6% from 2025 to 2034. This growth is primarily driven by the increasing sophistication of phishing attempts and cyberattacks targeting cloud infrastructure. As businesses adopt cloud-native environments with containerized applications and complex cloud configurations, new security challenges are emerging. These include issues like misconfigurations and increasingly intricate attack surfaces, leaving organizations vulnerable to advanced threats. In response, CNAPP solutions are evolving to meet the demands of modern cloud infrastructures, offering a much-needed shield against evolving cyber risks.

The market is segmented into solutions and services, with solutions commanding the largest share, accounting for 70% of the market in 2024. This segment is expected to generate USD 35 billion by 2034. As threats continue to escalate, CNAPP solutions are incorporating cutting-edge threat intelligence by integrating global databases and collective intelligence. These platforms are shifting towards predictive security models, which help anticipate vulnerabilities and proactively address emerging threats before they can cause damage. Context-aware tools are gaining traction, offering cross-domain threat correlation for enhanced risk assessments and more agile responses to security breaches.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.4 Billion |

| Forecast Value | $57.1 Billion |

| CAGR | 32.6% |

By deployment type, the market is divided between hybrid and multi-cloud environments. The hybrid segment is set to reach USD 30 billion by 2034, driven by the increasing need for consistent security governance across both on-premises and cloud infrastructures. As enterprises adopt multi-cloud strategies, the demand for unified security management tools is surging. These tools ensure centralized visibility, enabling businesses to enforce compliance and manage risk across diverse systems effectively. CNAPP platforms are evolving to bridge the gap between traditional data center security and modern cloud-native architectures, ensuring a seamless integration of security measures without compromising on compliance or risk management standards.

The U.S. dominates the CNAPP market, capturing 85% of the share in 2024, bolstered by growing cyber threats and stringent federal regulations. In this highly regulated environment, organizations are increasingly prioritizing security frameworks that emphasize continuous verification, least-privilege access, and granular visibility. Investments in adaptive authentication tools and real-time risk assessment capabilities are becoming more common as organizations look to protect their distributed cloud ecosystems from potential cyberattacks.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Cloud service providers

- 3.2.2 Technology providers

- 3.2.3 Application developers

- 3.2.4 System integrators

- 3.2.5 End use

- 3.3 Profit margin analysis

- 3.4 Technology differentiators

- 3.4.1 Unified platform approach

- 3.4.2 DevSecOps integration

- 3.4.3 Zero-trust security models

- 3.4.4 Runtime Application Self-Protection (RASP)

- 3.4.5 Others

- 3.5 Key news & initiatives

- 3.6 Patent analysis

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Growing adoption of cloud-based platforms

- 3.8.1.2 Rising cybersecurity threats

- 3.8.1.3 Stringent data protection regulations

- 3.8.1.4 Adoption of DevSecOps practices

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 Complex cloud environments

- 3.8.2.2 Performance overhead

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter’s analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Solution

- 5.2.1 Identity-Based Security and Cloud Infrastructure Entitlement Management (CIEM)

- 5.2.2 cloud workload protection CWPP

- 5.2.3 Infrastructure as a Code (IAC)

- 5.2.4 Kubernetes Security Posture Management (KSPM)

- 5.2.5 Cloud Security Posture Management (CSPM)

- 5.3 Services

- 5.3.1 Professional services

- 5.3.2 Managed services

Chapter 6 Market Estimates & Forecast, By Cloud, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Hybrid cloud

- 6.3 Multi-cloud

Chapter 7 Market Estimates & Forecast, By Organization Size, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 SME

- 7.3 Large Enterprise

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Retail

- 8.3 BFSI

- 8.4 Healthcare

- 8.5 Government

- 8.6 IT & Telecom

- 8.7 Manufacturing

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Aqua Security

- 10.2 Checkpoint Security

- 10.3 CrowdStrike

- 10.4 Data Theorem

- 10.5 Fortinet

- 10.6 LaceWorks

- 10.7 McAfee

- 10.8 Orca Security

- 10.9 Palo Alto Networks

- 10.10 Qualys

- 10.11 Runecast Solutions

- 10.12 Skyhigh Security

- 10.13 Sonrai

- 10.14 Sysdig

- 10.15 Tenable

- 10.16 Tigera

- 10.17 Trend Micro

- 10.18 Uptycs

- 10.19 Wiz.io

- 10.20 Zscaler

- 10.21 Others

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日