|

|

市場調査レポート

商品コード

1666618

有機ランキンサイクル市場の機会、成長促進要因、産業動向分析、2025~2034年の予測Organic Rankine Cycle (ORC) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 有機ランキンサイクル市場の機会、成長促進要因、産業動向分析、2025~2034年の予測 |

|

出版日: 2024年12月26日

発行: Global Market Insights Inc.

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

世界の有機ランキンサイクル市場は、2024年に188億米ドルとなり、2034年までのCAGRは15%と予測され、著しい成長が見込まれています。

この急拡大の背景には、環境に優しいエネルギーソリューションの採用が増加し、さまざまな分野で廃熱回収システムの需要が高まっていることがあります。ORC技術は、二酸化炭素排出量を大幅に削減しながらエネルギー利用を最適化する変革的ソリューションとして登場しました。地熱発電、バイオマスエネルギー発電、太陽熱システム、産業用アプリケーションなど、その汎用性の高さから、世界の再生可能エネルギー転換の要となっています。

市場力学は、持続可能なエネルギー導入を促進する有利な政府政策とインセンティブによってさらに形成されています。税額控除、補助金、助成金がORCシステムへの投資を奨励し、世界中の産業界にとってより身近で魅力的なものとなっています。この成長はまた、エネルギー効率を達成し、国際的な気候変動目標に沿うことを重視する産業界の高まりにも後押しされています。低温の熱源を利用可能な電力に変換する能力を持つORC技術は、持続可能な発電と廃熱管理において極めて重要な役割を果たしています。世界の産業界がカーボンニュートラルの優先順位を高めている中、ORC市場はグリーンエネルギー変革の不可欠なイネーブラーとして位置づけられています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 188億米ドル |

| 予測金額 | 767億米ドル |

| CAGR | 15% |

ORC市場は、廃熱回収、バイオマス、太陽熱、廃棄物発電、石油・ガス、地熱など、多様な産業における用途別に区分されます。特に地熱分野は、2034年までに407億米ドルを生み出すと予測されています。再生可能エネルギー源と持続可能な電力ソリューションが重視されるようになったことで、ORCアプリケーションにおける地熱エネルギーの役割が高まっています。カーボンニュートラルで知られる地熱エネルギーは、世界の気候変動問題への取り組みとシームレスに整合しており、政府や民間投資家の優先事項となっています。政府のインセンティブ、税制優遇、政策枠組みによる強力な支援が、地熱エネルギー・プロジェクトへの投資をさらに加速させ、ORC市場の成長軌道を後押ししています。

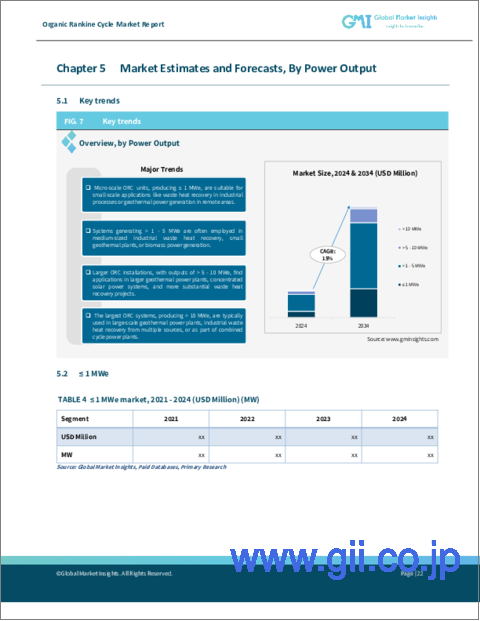

ORC市場の出力区分では、1~5 MWe以上のカテゴリーに大きな可能性があり、2034年までのCAGRは13.9%と予想されています。この成長は、中規模ORCプロジェクト、特に小規模地熱発電、産業廃熱回収、バイオマス発電所への導入が増加していることに起因しています。1~5 MWe以上のセグメントは、コスト効率が高く持続可能なエネルギー・ソリューションを提供し、運用コストとカーボンフットプリントを削減しながらエネルギー効率を高めようとする産業と共鳴しています。

米国では、再生可能エネルギー・プロジェクトとエネルギー効率向上対策への投資の増加により、ORC市場は2034年までに171億米ドルを生み出すと予想されています。廃熱回収と排出削減を目的としたORCシステムの統合は、連邦政府および州の持続可能性イニシアティブに合致しており、業界全体への普及を確実なものにしています。地熱発電は、豊富な資源と政府の支援プログラムに支えられ、米国ORC市場の主要な貢献者であり続けています。

目次

第1章 調査手法と調査範囲

- 市場の定義

- 基本推定と計算

- 予測計算

- データソース

- 1次データ

- 2次データ

- 有償

- 公的

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーターの分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- PESTEL分析

第4章 競合情勢

- 戦略ダッシュボード

- イノベーションと持続可能性の展望

第5章 市場規模・予測:出力別、2021年~2034年

- 主要動向

- 1 MWe以下

- 1~5 MWe超

- 5~10 MWe超

- 10 MWe超

第6章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 廃熱回収

- バイオマス

- 地熱

- 太陽熱

- 石油・ガス

- 廃棄物エネルギー化

第7章 市場規模・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- イタリア

- ロシア

- スペイン

- アジア太平洋

- 中国

- オーストラリア

- インド

- 日本

- 韓国

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

- 南アフリカ

- エジプト

- ラテンアメリカ

- ブラジル

- アルゼンチン

第8章 企業プロファイル

- ABB

- Alfa Laval

- Atlas Copco

- Calnetix Technologies

- Elvosolar

- Enertime

- Energia

- Exergy International

- General Electric

- Intec GMK

- Kaishan USA

- Mitsubishi Heavy Industries

- Orchan Energy

- Ormat Technologies

- Triogen

- Turboden

The Global Organic Rankine Cycle Market, valued at USD 18.8 billion in 2024, is poised for remarkable growth with a projected CAGR of 15% through 2034. This rapid expansion is fueled by the rising adoption of eco-friendly energy solutions and increasing demand for waste heat recovery systems across various sectors. ORC technology has emerged as a transformative solution for optimizing energy usage while significantly reducing carbon emissions. Its versatility in geothermal power, biomass energy generation, solar thermal systems, and industrial applications makes it a cornerstone of the global renewable energy transition.

Market dynamics are further shaped by favorable government policies and incentives promoting sustainable energy adoption. Tax credits, grants, and subsidies have incentivized investments in ORC systems, making them more accessible and appealing to industries worldwide. This growth is also driven by industries' rising focus on achieving energy efficiency and aligning with international climate change goals. With its ability to convert low-temperature heat sources into usable electricity, ORC technology plays a pivotal role in sustainable power generation and waste heat management. As global industries increasingly prioritize carbon neutrality, the ORC market is positioned as an integral enabler of green energy transformation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $18.8 Billion |

| Forecast Value | $76.7 Billion |

| CAGR | 15% |

The ORC market is segmented by application across diverse industries, including waste heat recovery, biomass, solar thermal, waste-to-energy, oil and gas, and geothermal energy. The geothermal segment, in particular, is projected to generate USD 40.7 billion by 2034. The growing emphasis on renewable energy sources and sustainable power solutions has elevated geothermal energy's role in ORC applications. Geothermal energy, known for its carbon-neutral characteristics, aligns seamlessly with global climate initiatives, making it a priority for governments and private investors alike. Robust support through government incentives, tax benefits, and policy frameworks has further accelerated investments in geothermal energy projects, bolstering the ORC market growth trajectory.

Power output segmentation within the ORC market reveals strong potential in the > 1 - 5 MWe category, which is anticipated to grow at a CAGR of 13.9% through 2034. This growth stems from the increasing deployment of medium-scale ORC projects, particularly in small-scale geothermal initiatives, industrial waste heat recovery, and biomass power plants. The > 1 - 5 MWe segment offers a cost-efficient and sustainable energy solution that resonates with industries seeking to enhance energy efficiency while reducing operational costs and carbon footprints.

In the United States, the ORC market is expected to generate USD 17.1 billion by 2034, driven by increased investments in renewable energy projects and enhanced energy efficiency measures. The integration of ORC systems for waste heat recovery and emissions reduction aligns with federal and state sustainability initiatives, ensuring widespread adoption across industries. Geothermal power remains a key contributor to the U.S. ORC market, supported by abundant resources and government-backed programs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's Analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL Analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Power Output, 2021 – 2034 (USD Million & MW)

- 5.1 Key trends

- 5.2 ≤ 1 MWe

- 5.3 > 1 - 5 MWe

- 5.4 > 5 - 10 MWe

- 5.5 > 10 MWe

Chapter 6 Market Size and Forecast, By Application, 2021 – 2034 (USD Million & MW)

- 6.1 Key trends

- 6.2 Waste heat recovery

- 6.3 Biomass

- 6.4 Geothermal

- 6.5 Solar thermal

- 6.6 Oil & gas

- 6.7 Waste to energy

Chapter 7 Market Size and Forecast, By Region, 2021 – 2034 (USD Million & MW)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 France

- 7.3.3 Germany

- 7.3.4 Italy

- 7.3.5 Russia

- 7.3.6 Spain

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 India

- 7.4.4 Japan

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Turkey

- 7.5.4 South Africa

- 7.5.5 Egypt

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 ABB

- 8.2 Alfa Laval

- 8.3 Atlas Copco

- 8.4 Calnetix Technologies

- 8.5 Elvosolar

- 8.6 Enertime

- 8.7 Energia

- 8.8 Exergy International

- 8.9 General Electric

- 8.10 Intec GMK

- 8.11 Kaishan USA

- 8.12 Mitsubishi Heavy Industries

- 8.13 Orchan Energy

- 8.14 Ormat Technologies

- 8.15 Triogen

- 8.16 Turboden