|

市場調査レポート

商品コード

1959561

自動車向けV2X(Vehicle-to-Everything)の市場機会、成長要因、業界動向分析、および2026年から2035年までの予測Automotive Vehicle-to-Everything (V2X) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 自動車向けV2X(Vehicle-to-Everything)の市場機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2026年02月11日

発行: Global Market Insights Inc.

ページ情報: 英文 270 Pages

納期: 2~3営業日

|

概要

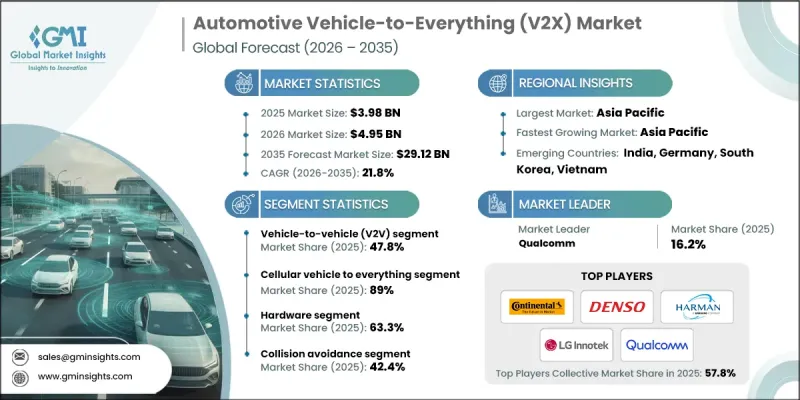

世界の自動車向けV2X(Vehicle-to-Everything)市場は、2025年に39億8,000万米ドルと評価され、2035年までにCAGR21.8%で成長し、291億2,000万米ドルに達すると予測されています。

道路安全への懸念の高まりと、車両自動化への移行加速が、自動車用V2X通信技術の採用を大きく推進しております。世界各国の政府は、交通流管理と緊急対応効率の向上を図るため、インテリジェント交通インフラやデジタル料金徴収システムを導入しております。主要経済圏の公共機関は、戦略的なモビリティ回廊に沿った協調型インテリジェント交通システムの導入を推進しており、接続された交差点における渋滞の顕著な軽減が実証されております。コネクテッドカーおよび電気自動車の普及拡大は、V2Xエコシステム全体をさらに強化しております。超低遅延通信規格の進歩により、V2Xソリューションの商業的実現可能性が向上しています。第5世代移動通信システム(5G)はエンドツーエンドの遅延を10ミリ秒未満に抑え、衝突回避、車両隊列走行、混合交通環境における協調自律走行のためのリアルタイム意思決定を可能にします。同時に、接続車両が1時間あたり25ギガバイト以上のデータを生成する中、サイバーセキュリティとデータガバナンスが重要な優先事項となっており、自動車メーカーや規制当局は、公共道路ネットワーク全体での信頼性の高い通信を確保するため、堅牢な本人認証、暗号化プロトコル、安全なアクセス制御システムの実装を推進しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 39億8,000万米ドル |

| 予測金額 | 291億2,000万米ドル |

| CAGR | 21.8% |

車両間通信(V2V)セグメントは2025年に47.8%のシェアを占め、2026年から2035年にかけてCAGR20.8%で成長すると予測されています。V2V通信は、速度、位置、制動動作に関する情報を含む、車両間の直接的なデータ交換を可能にします。安全当局は、コネクテッド安全技術の広範な導入により、複数車両が関与する事故のかなりの割合を防止できると推定しており、乗用車および商用車プラットフォーム全体でのOEMによるより広範な統合を促進しています。車両とインフラ間の通信(V2I)は、車両と道路システム間の相互作用を可能にし、交通の最適化と協調的なモビリティ管理を支援することで、このエコシステムをさらに強化します。

セルラーV2Xセグメントは2025年に89%のシェアを占め、2035年までCAGR22.7%で成長すると予測されています。セルラーV2Xアーキテクチャは、車両、インフラ、ネットワーク事業者、クラウドプラットフォームを連携させる統合通信フレームワークを提供します。この接続性は、継続的なソフトウェア更新、遠隔診断、段階的な車両自動化機能をサポートします。セルラーV2Xは、車両、歩行者、路側システム、バックエンドネットワークを単一の通信エコシステム内に統合することで、自家用車、商用車両、公共交通システム間の相互運用性を強化し、スケーラブルな展開を加速します。

中国自動車V2X(Vehicle-to-Everything)市場は63.8%のシェアを占め、2025年には12億米ドルの規模に達すると予測されています。強力な国家レベルの調整、大規模な知能化交通イニシアチブ、統合されたスマートシティ戦略により、中国はV2X導入の重要な環境として位置づけられています。国内自動車メーカーは、通信事業者やデジタルサービスプロバイダーと連携しながら、プロトコルの標準化と都市部・高速道路インフラを横断する全国的な接続性の拡大を進めるとともに、車両プラットフォーム全体にV2X機能を組み込んでいます。

よくあるご質問

目次

第1章 調査手法

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 強化される道路安全規制

- コネクテッドカーおよび自動運転車の成長

- スマートシティプログラムの拡大

- 第5世代ネットワークの導入

- 業界の潜在的リスク&課題

- インフラ導入コストの高さ

- 相互運用性と標準化に関する課題

- 市場機会

- 自動運転システムとの統合

- 車両からインフラプロジェクトへの拡大

- 電気自動車およびコネクテッドカーの車両台数の増加

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 米国におけるコネクテッドカーおよび高度道路交通システム(ITS)規制

- 連邦通信および周波数割当ガイドライン

- 車両安全性とコネクテッドモビリティ基準

- カナダにおける協調型高度道路交通システム(ITS)規制

- 欧州

- 欧州連合協調型高度道路交通システム(ITS)フレームワーク

- V2X向けETSIおよびCEN通信規格

- 国レベルにおけるコネクテッドカーの規制要件

- コネクテッドモビリティ向けデータ保護およびサイバーセキュリティ規則

- アジア太平洋地域

- 中国におけるスマートコネクテッドカー規制

- インドにおけるコネクテッド・トランスポートおよび自動車通信規格

- 日本における協調運転および車両間通信ガイドライン

- 韓国のスマートモビリティとV2X(車両間通信)の適合性

- ASEAN地域におけるコネクテッド・トランスポート枠組み

- ラテンアメリカ

- ブラジルにおける高度道路交通システム(ITS)及びコネクテッドカー規制

- アルゼンチンにおける自動車通信規制への適合

- メキシコのコネクテッドモビリティおよび交通デジタル化政策

- 地域別コネクテッドカー規制枠組み

- 中東・アフリカ

- アラブ首長国連邦(UAE)におけるスマートモビリティ及びコネクテッドカー規制

- サウジアラビアにおける高度交通システム(ITS)の適合性

- 南アフリカのコネクテッドカーおよび道路安全基準

- 地域別スマート交通規制枠組み

- 北米

- ポーターの分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- コスト内訳分析

- 特許分析

- 持続可能性と環境面

- 持続可能な実践

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- カーボンフットプリントに関する考慮事項

- OEMおよびインフラ投資分析

- 自動車メーカーの投資優先順位

- 公共部門および自治体資金調達動向

- 民間セクターおよび通信投資

- 展開経済性と投資利益率(ROI)評価

- OEM向け費用便益分析

- 公共機関向けインフラ投資対効果(ROI)

- アプリケーション別回収期間

- 周波数割当と通信信頼性分析

- ライセンシングと免許不要制スペクトラムの比較検討

- ネットワークの混雑と性能リスク

- 国境を越えたスペクトラム調和の課題

- 収益化とビジネスモデル分析

- OEM主導の収益化モデル

- サブスクリプションおよびサービスベースの収益源

- データ駆動型およびプラットフォームベースの収益化

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画と資金調達

第5章 市場推計・予測:タイプ別、2022-2035

- 車両とインフラ間の通信(V2I)

- 車両間通信(V2V)

- 車両から歩行者への通信(V2P)

- その他

第6章 市場推計・予測:技術別、2022-2035

- 専用短距離通信(DSRC)

- C-V2X(Cellular Vehicle-To-Everything)

第7章 市場推計・予測:コンポーネント別、2022-2035

- ハードウェア

- 追跡および位置特定

- GNSS/GPSモジュール(標準)

- 高精度GNSS(DGPS/RTK)

- 安全性および認識

- レーダーセンサー

- カメラ

- LiDAR

- 超音波センサー

- 熱式および飛行時間式センサー

- 制御および処理

- V2X電子制御ユニット(V2X ECU)

- ADAS ECU

- ドメインコントローラー

- 通信および接続性

- C-V2Xモデム

- DSRC無線機

- 5G NR-V2Xモジュール

- 車載ユニット(OBU)

- テレマティクス制御ユニット(TCU)

- V2Xアンテナ

- ヒューマンマシンインターフェース

- V2Xディスプレイ

- ヘッドアップディスプレイ(HUD)

- 計器クラスターのアラート

- 音声および触覚アラートモジュール

- その他

- 追跡および位置特定

- ソフトウェア

- サービス

- コンサルティングおよび統合サービス

- サイバーセキュリティおよびデータ保護サービス

- 交通管理および道路安全サービス

- その他

第8章 市場推計・予測:用途別、2022-2035

- フリート管理

- 自動運転

- 衝突回避

- 高度道路交通システム(ITS)

- 駐車場管理システム

- その他

第9章 市場推計・予測:展開別、2022-2035

- クラウドベース

- オンプレミス

第10章 市場推計・予測:車両別、2022-2035

- 乗用車

- セダン

- SUV

- ハッチバック

- 商用車

- 小型商用車(LCV)

- 中型商用車(MCV)

- 大型商用車(HCV)

第11章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- ノルウェー

- オランダ

- スウェーデン

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- シンガポール

- タイ

- インドネシア

- ベトナム

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ地域

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

第12章 企業プロファイル

- 世界プレイヤー

- AT&T

- Bosch

- Continental

- Denso

- Harman

- LG Innotek

- Nokia

- NXP

- Qualcomm

- 地域別プレーヤー

- Fujitsu

- Huawei Technologies

- Hyundai Mobis

- NEC Corporation

- Panasonic Automotive Systems

- Renesas Electronics

- Toyota Connected

- ZTE Corporation

- 新興企業および破壊的企業

- Autotalks

- Cohda Wireless

- Commsignia

- Danlaw

- Kapsch TrafficCom