|

|

市場調査レポート

商品コード

1666544

マテリアルハンドリング機器の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Material Handling Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| マテリアルハンドリング機器の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2024年12月03日

発行: Global Market Insights Inc.

ページ情報: 英文 242 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

マテリアルハンドリング機器の世界市場は、2024年の1,782億米ドルから成長し、2025年から2034年にかけてCAGR6%で拡大すると予測されています。

eコマースの台頭が主要な推進力となっており、迅速な配送に対する消費者の期待の高まりが、オンライン小売業者に在庫管理、製品仕分け、注文処理などの効率的なソリューションの導入を促しています。ロボットピッカー、コンベア、自動搬送車(AGV)などの自動化システムは、当日配送や翌日配送の需要を満たすためにますます不可欠になっています。

倉庫インフラや配送センターへの投資は、先進的なマテリアルハンドリング機器の必要性を煽っています。eコマースや小売の需要増に対応するために事業を拡大する企業は、大量の商品を効率的に処理する革新的なシステムを必要としています。近代的な倉庫は急速に自動化へと移行しており、ロボットソリューション、AGV、その他の先進技術を活用して業務効率を最適化し、市場力学に対応しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 1,782億米ドル |

| 予測金額 | 3,110億米ドル |

| CAGR | 6% |

市場はタイプ別にメーカーとディストリビューターに分類され、メーカーは2024年に1,264億米ドルの収益を上げました。製造業者セグメントの成長は、生産プロセスにおける自動化と効率化への注目の高まりを反映しています。サプライチェーンのダイナミクスが進化するにつれて、製造業者は生産性の向上とオペレーションの合理化のために洗練されたマテリアルハンドリングソリューションにますます依存するようになり、現代産業におけるこれらのシステムの重要な役割が強化されています。

用途別に見ると、市場はeコマース、3PL、食品・飲料、製造業、医薬品、雑貨などのセクターに広がっています。3PL分野は、ロジスティクスのアウトソーシング傾向の高まりに牽引され、2024年には市場の20%を占めました。中核となる強みに集中する企業は第三者物流プロバイダーに目を向け、シームレスで効率的なオペレーションを確保するための高度なハンドリングシステムへの需要を高めています。

中国のマテリアルハンドリング機器市場は2024年に41%のシェアを占めました。同国の堅調な工業化、拡大するインフラプロジェクト、活況を呈するeコマース活動が、この成長の主な要因となっています。さらに、この地域の製造業部門は繁栄しており、業務上の需要を満たすために高度なロジスティクスとサプライチェーン技術への依存度が高まっていることを裏付けています。

マテリアルハンドリング機器市場は、自動化、進化する消費者の期待、部門を超えた産業の継続的な拡大が原動力となり、大幅な成長を示すことになると思われます。企業が効率性と拡張性を追求する中、革新的なマテリアルハンドリングソリューションの採用は、世界市場の進展において極めて重要な要素であり続けると予想されます。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 一次調査と検証

- 一次ソース

- データマイニングソース

- 市場定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- サプライヤーの状況

- 原材料サプライヤー

- 予備部品サプライヤー

- 部品サプライヤー

- メーカー

- 技術プロバイダー

- サービスプロバイダー

- システムインテグレーター

- 最終用途

- 利益率分析

- コスト内訳分析

- テクノロジーとイノベーションの展望

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 成長促進要因

- eコマースとロジスティクス産業の拡大

- 人件費の上昇と手作業による雇用の不便さ

- 倉庫や配送センターへの投資の増加

- 製造活動における技術革新と自動化の導入の増加

- 業界の潜在的リスク・課題

- マテリアルハンドリング機器の高い初期コスト

- 機器操作の認識不足

- 成長促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業市場シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- 保管・ハンドリング機器

- ラック

- スタッキングフレーム

- 棚、ビン、引き出し

- メザニン

- 産業用トラック

- 無人搬送車

- ハンドトラック、プラットフォームトラック、パレットトラック

- オーダーピッカー

- パレット・ジャッキ

- サイドローダー

- ウォーキー・スタッカー

- バルクマテリアルハンドリング機器

- コンベアベルト

- ケースコンベヤ

- パレットコンベヤ

- スタッカー

- リクレーマー

- エレベーター

- その他

- コンベアベルト

- ロボット

- 自律移動ロボット

- コボット

- スカラロボット

- 産業用ロボット

- その他

- AS/RS

- ユニットロードAS/RS

- ミニロードAS/RS

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 3PL

- eコマース

- 一般雑貨

- 食品小売

- 食品・飲料

- 製造業

- 耐久財

- 非耐久

- 医薬品/ヘルスケア

第7章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- メーカー

- 流通業者

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- 東南アジア

- ラテンアメリカ

- ブラジル

- アルゼンチン

- メキシコ

- 中東・アフリカ

- UAE

- サウジアラビア

- 南アフリカ

第9章 企業プロファイル

- Beumer Group GmbH & Co. KG

- Clark Material Handling Company

- Columbus McKinnon

- Crown Equipment

- Daifuku Co.

- Dearborn Mid-West Company

- Fives Group

- Flexlink

- Godrej & Boyce Manufacturing Company

- Grenzebach Maschinenbau

- Honeywell Intelligrated

- Hyster-Yale Materials Handling

- JBT

- Jungheinrich

- Kardex

- KION GROUP

- Knapp

- KUKA

- Mecalux, S.A

- Mitsubishi Caterpillar Forklift America

- Murata Machinery

- Siemens

- SSI Schaefer Group

- System Logistics

- TGW Logistics Group

- Toyota Industries

- Viastore Systems

- Witron Logistik+Informatik

The Global Material Handling Equipment Market is projected to grow from USD 178.2 billion in 2024, expanding at a CAGR of 6% between 2025 and 2034. The rise of e-commerce is a key driver, with growing consumer expectations for rapid delivery pushing online retailers to adopt efficient solutions for inventory management, product sorting, and order fulfillment. Automated systems such as robotic pickers, conveyors, and automated guided vehicles (AGVs) are increasingly essential to meet the demand for same-day and next-day deliveries.

Investments in warehouse infrastructure and distribution centers fuel the need for advanced material handling equipment. Companies scaling their operations to meet increased e-commerce and retail demands require innovative systems to handle high volumes of goods efficiently. Modern warehouses are rapidly transitioning to automation, leveraging robotic solutions, AGVs, and other advanced technologies to optimize operational efficiency and keep pace with market dynamics.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $178.2 Billion |

| Forecast Value | $311 Billion |

| CAGR | 6% |

The market is categorized by type into manufacturers and distributors, with manufacturers generating USD 126.4 billion in revenue in 2024. The manufacturer segment's growth reflects the rising focus on automation and efficiency in production processes. As supply chain dynamics evolve, manufacturers increasingly rely on sophisticated material handling solutions to enhance productivity and streamline operations, reinforcing the critical role of these systems in modern industries.

By application, the market spans sectors including e-commerce, 3PL, food and beverage, manufacturing, pharmaceutical, and general merchandise. The 3PL segment accounted for 20% of the market in 2024, driven by the growing trend of outsourcing logistics. Businesses focusing on their core strengths are turning to third-party logistics providers, heightening the demand for advanced handling systems to ensure seamless and efficient operations.

China material handling equipment market held a 41% share in 2024. The country's robust industrialization, expanding infrastructure projects, and booming e-commerce activities are major contributors to this growth. Additionally, the region's manufacturing sector thrives, underscoring the increasing reliance on advanced logistics and supply chain technologies to meet operational demands.

The material handling equipment market is set to witness substantial growth, driven by automation, evolving consumer expectations, and the continuous expansion of industries across sectors. As companies strive for efficiency and scalability, the adoption of innovative material handling solutions is expected to remain a pivotal factor in the global market's progression.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

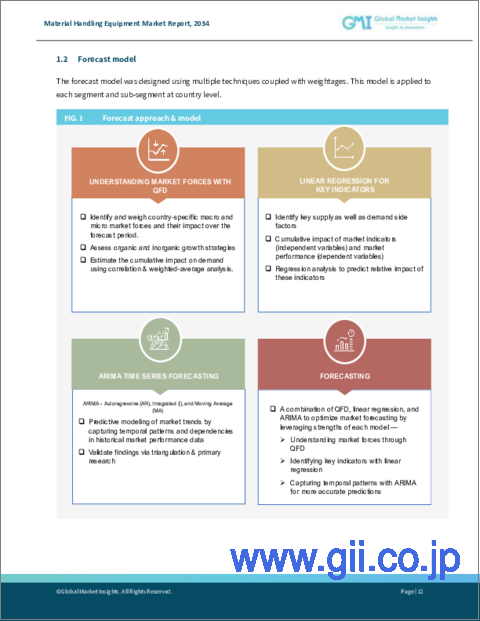

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material supplier

- 3.2.2 Spare part supplier

- 3.2.3 Component supplier

- 3.2.4 Manufacturer

- 3.2.5 Technology provider

- 3.2.6 Service provider

- 3.2.7 System Integrators

- 3.2.8 End use

- 3.3 Profit margin analysis

- 3.4 Cost breakdown analysis

- 3.5 Technology & innovation landscape

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Expanding e-commerce and logistics industries

- 3.8.1.2 Rising labor costs and the inconvenience of employing a manual workforce

- 3.8.1.3 Increased warehouse and distribution center investments

- 3.8.1.4 Increasing technological innovations and the adoption of automation in manufacturing activities

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High initial costs of material handling equipment

- 3.8.2.2 Lack of awareness of equipment operation

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter’s analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Storage and handling equipment

- 5.2.1 Racks

- 5.2.2 Stacking frames

- 5.2.3 Shelves, bins and drawers

- 5.2.4 Mezzanines

- 5.3 Industrial trucks

- 5.3.1 AGVs

- 5.3.2 Hand, platform and pallet trucks

- 5.3.3 Order pickers

- 5.3.4 Pallet jacks

- 5.3.5 Side-loaders

- 5.3.6 Walkie stackers

- 5.4 Bulk material handling equipment

- 5.4.1 Conveyor belts

- 5.4.1.1 Case conveyors

- 5.4.1.2 Pallet conveyors

- 5.4.2 Stackers

- 5.4.3 Reclaimers

- 5.4.4 Elevators

- 5.4.5 Others

- 5.4.1 Conveyor belts

- 5.5 Robotics

- 5.5.1 Autonomous mobile robots

- 5.5.2 Cobots

- 5.5.3 Scara robots

- 5.5.4 Industrial robots

- 5.5.5 Others

- 5.6 AS/RS

- 5.6.1 Unit-load AS/RS

- 5.6.2 Mini-load AS/RS

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 3PL

- 6.3 E-commerce

- 6.4 General merchandise

- 6.5 Food retail

- 6.6 Food & beverage

- 6.7 Manufacturing

- 6.7.1 Durable

- 6.7.2 Non-Durable

- 6.8 Pharmaceutical/healthcare

Chapter 7 Market Estimates & Forecast, By Type, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.1.1 Manufacturers

- 7.1.2 Distributors

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Nordics

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Argentina

- 8.5.3 Mexico

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 Saudi Arabia

- 8.6.3 South Africa

Chapter 9 Company Profiles

- 9.1 Beumer Group GmbH & Co. KG

- 9.2 Clark Material Handling Company

- 9.3 Columbus McKinnon

- 9.4 Crown Equipment

- 9.5 Daifuku Co.

- 9.6 Dearborn Mid-West Company

- 9.7 Fives Group

- 9.8 Flexlink

- 9.9 Godrej & Boyce Manufacturing Company

- 9.10 Grenzebach Maschinenbau

- 9.11 Honeywell Intelligrated

- 9.12 Hyster-Yale Materials Handling

- 9.13 JBT

- 9.14 Jungheinrich

- 9.15 Kardex

- 9.16 KION GROUP

- 9.17 Knapp

- 9.18 KUKA

- 9.19 Mecalux, S.A

- 9.20 Mitsubishi Caterpillar Forklift America

- 9.21 Murata Machinery

- 9.22 Siemens

- 9.23 SSI Schaefer Group

- 9.24 System Logistics

- 9.25 TGW Logistics Group

- 9.26 Toyota Industries

- 9.27 Viastore Systems

- 9.28 Witron Logistik + Informatik