|

市場調査レポート

商品コード

1665437

低消費電力次世代ディスプレイ市場の機会、成長促進要因、産業動向分析、2025~2034年の予測Low Power Next Generation Display Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 低消費電力次世代ディスプレイ市場の機会、成長促進要因、産業動向分析、2025~2034年の予測 |

|

出版日: 2024年12月31日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

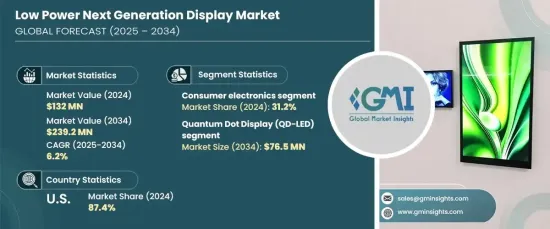

世界の低消費電力次世代ディスプレイ市場は、2024年に1億3,200万米ドルと評価され、2025年から2034年にかけてCAGR 6.2%で成長すると予測されています。

ディスプレイ技術の進歩がこの成長の原動力となっており、OLEDとMicroLEDシステムの著しい進歩により、ピクセル密度、色忠実度、応答性が向上し、同時にエネルギー需要が削減されています。これらの開発は、拡張現実(AR)や仮想現実(VR)などの用途における高解像度でエネルギー効率の高いディスプレイのニーズの高まりに対応しています。これらのシステムにAIとIoTを統合することで、イノベーションはさらに加速し、さまざまなデバイスにインテリジェントで適応性の高い機能を提供しています。環境意識の高まりとカーボンフットプリントの削減努力は、メーカーと消費者の双方にエネルギー効率の高いソリューションの採用を促しており、次世代ディスプレイはさまざまな分野で支持を集めています。

2024年には、民生用電子機器が市場の31.2%を占める主要用途分野に浮上しました。スマートフォン、タブレット、ラップトップ、ウェアラブルなどのデバイスは、バッテリ寿命の延長と優れたディスプレイ品質を優先するため、このセグメントの成長に大きく貢献しています。OLED、MicroLED、電子ペーパー技術は、エネルギー消費を最小限に抑えながら鮮やかなビジュアルを提供する上で極めて重要な役割を果たしています。折りたたみ可能でフレキシブルな設計へのシフトも需要を促進しており、革新的なフォーマットが携帯性と機能性に対する消費者の期待に応えています。5GネットワークとIoT対応デバイスの採用拡大により、この分野の継続的な拡大が確実視されています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 1億3,200万米ドル |

| 予測金額 | 2億3,920万米ドル |

| CAGR | 6.2% |

量子ドットディスプレイ(QD-LED)の技術的進歩により、QD-LEDは市場の有力なプレーヤーとして位置づけられています。2034年までに7,650万米ドルの売上が見込まれるこのディスプレイは、卓越した色精度、輝度、エネルギー効率を提供します。量子ドットは正確な発光を可能にし、色域と性能の点で従来のLCDやOLEDを凌駕します。これらの特徴により、QD-LEDディスプレイはテレビやモニターを含む高級電子機器に高い人気があり、また、その低エネルギー要件は持続可能なソリューションに対する需要の高まりに対応しています。

米国は2024年に北米の低消費電力次世代ディスプレイ市場をリードし、同地域の売上高の87.4%を占めました。この優位性は、堅調な家電産業と最先端の研究開発に起因します。OLEDやMicroLEDのような高度なディスプレイ技術は、スマートテレビ、スマートフォン、車載ディスプレイなどの用途に広く組み込まれています。自動車分野、特に電気自動車ではエネルギー効率の高いソリューションの採用が拡大しており、インフォテインメントやヘッドアップシステム用の低消費電力ディスプレイの重要性が強調されています。さらに、家電製品や産業用用途へのIoTとAIの統合が引き続き市場需要を促進しており、米国がイノベーションと技術進歩のリーダーであることを裏付けています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 1次データ

- 2次データ

- 有料情報源

- 公的情報源

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 破壊

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 促進要因

- ディスプレイ技術の進歩

- エネルギー効率の高い家電製品に対する需要

- ウェアラブル機器への応用拡大

- 産業用およびヘルスケア用途での採用拡大

- 業界の潜在的リスク&課題

- 高い製造コスト

- 限られた寿命と耐久性への懸念

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 量子ドットディスプレイ(QD-LED)

- フィールドエミッションディスプレイ(FED)

- レーザー蛍光体ディスプレイ(LPD)

- 有機発光ダイオード(OLED)

- 有機発光トランジスタ(OLET)

- 表面伝導型電子放出素子ディスプレイ(SED)

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 民生用電子機器

- 家庭用電化製品

- 広告

- 公共ディスプレイ

- オートメーション

- 航空

第7章 市場推計・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第8章 企業プロファイル

- AU Optronics Corporation

- AUO Corporation

- BOE Technology Group Co., Ltd.

- Doosan Group

- DuPont de Nemours, Inc.

- Futaba Corporation

- LG Display Co., Ltd.

- Nanosys, Inc.

- Novaled GmbH

- Panasonic Corporation

- Philips International B.V.

- Planar Systems, Inc.

- QUALCOMM Incorporated

- RitDisplay Corporation

- Samsung Electronics Co., Ltd.

- Sharp Corporation

- Sony Corporation

- Tianma Microelectronics Co., Ltd.

- Universal Display Corporation(UDC)

- Visionox Technology, Inc.

The Global Low Power Next Generation Display Market, valued at USD 132 million in 2024, is projected to grow at a CAGR of 6.2% from 2025 to 2034. Advancements in display technology are driving this growth, with significant progress in OLED and MicroLED systems enhancing pixel density, color fidelity, and responsiveness while reducing energy demands. These developments cater to the increasing need for high-resolution and energy-efficient displays in applications like augmented reality (AR) and virtual reality (VR). The integration of AI and IoT into these systems is further accelerating innovation, offering intelligent and adaptive features for a wide range of devices. Rising environmental consciousness and efforts to reduce carbon footprints are encouraging both manufacturers and consumers to adopt energy-efficient solutions, with next-generation displays gaining traction across various sectors.

Consumer electronics emerged as the leading application area in 2024, capturing 31.2% of the market. Devices such as smartphones, tablets, laptops, and wearables are key contributors to this segment's growth, as they prioritize extended battery life and superior display quality. OLED, MicroLED, and e-paper technologies play a pivotal role in delivering vibrant visuals while minimizing energy consumption. The shift toward foldable and flexible designs has also fueled demand, with innovative formats meeting consumer expectations for portability and functionality. The growing adoption of 5G networks and IoT-enabled devices ensures the continued expansion of this segment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $132 million |

| Forecast Value | $239.2 million |

| CAGR | 6.2% |

Technological advancements in Quantum Dot Displays (QD-LED) have positioned them as a prominent player in the market. Expected to generate USD 76.5 million in revenue by 2034, these displays offer exceptional color accuracy, brightness, and energy efficiency. Quantum dots enable precise light emission, outperforming traditional LCDs and OLEDs in terms of color range and performance. These features make QD-LED displays highly sought after in premium electronics, including televisions and monitors, while their low energy requirements address the rising demand for sustainable solutions.

The United States led the North American low-power next-generation display market in 2024, accounting for 87.4% of the region's revenue. This dominance stems from a robust consumer electronics industry and cutting-edge research and development. Advanced display technologies like OLED and MicroLED are widely integrated across applications such as smart TVs, smartphones, and automotive displays. The growing adoption of energy-efficient solutions in the automotive sector, particularly in electric vehicles, underscores the importance of low-power displays for infotainment and heads-up systems. Additionally, the integration of IoT and AI into home appliances and industrial applications continues to propel market demand, reinforcing the US as a leader in innovation and technological advancement.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Advancements in display technology

- 3.6.1.2 Demand for energy-efficient consumer electronics

- 3.6.1.3 Expanding application in wearable devices

- 3.6.1.4 Growing adoption in industrial and healthcare applications

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High production costs

- 3.6.2.2 Limited longevity and durability concerns

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Technology, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Quantum Dot Display (QD-LED)

- 5.3 Field Emission Display (FED)

- 5.4 Laser Phosphor Display (LPD)

- 5.5 Organic Light-Emitting Diode (OLED)

- 5.6 Organic Light-Emitting Transistor (OLET)

- 5.7 Surface-Conduction Electron-Emitter Display (SED)

Chapter 6 Market Estimates & Forecast, By Application, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Consumer electronics

- 6.3 Home appliances

- 6.4 Advertising

- 6.5 Public display

- 6.6 Automation

- 6.7 Aviation

Chapter 7 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 Germany

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Russia

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.6 MEA

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 AU Optronics Corporation

- 8.2 AUO Corporation

- 8.3 BOE Technology Group Co., Ltd.

- 8.4 Doosan Group

- 8.5 DuPont de Nemours, Inc.

- 8.6 Futaba Corporation

- 8.7 LG Display Co., Ltd.

- 8.8 Nanosys, Inc.

- 8.9 Novaled GmbH

- 8.10 Panasonic Corporation

- 8.11 Philips International B.V.

- 8.12 Planar Systems, Inc.

- 8.13 QUALCOMM Incorporated

- 8.14 RitDisplay Corporation

- 8.15 Samsung Electronics Co., Ltd.

- 8.16 Sharp Corporation

- 8.17 Sony Corporation

- 8.18 Tianma Microelectronics Co., Ltd.

- 8.19 Universal Display Corporation (UDC)

- 8.20 Visionox Technology, Inc.