渋滞支援システム市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Traffic Jam Assist System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 175 Pages

- 納期

- 2~3営業日

- 商品コード

- 1665419

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

渋滞支援システムの世界市場規模は2024年に36億米ドルとなり、2025年から2034年にかけてCAGR 11.5%で成長すると予測されています。

この成長は、急速な人口増加と都市化による都市部の交通渋滞の悪化に起因します。自動車保有台数の増加と限られたインフラが交通問題をさらに悪化させ、通勤時間をより長くストレスの多いものにしています。渋滞支援システムは、渋滞時のアクセル、ブレーキ、ステアリングといった主要な運転機能を自動化することで、これを緩和することを目的としています。こうした機能はドライバーの疲労を軽減するだけでなく、スムーズな運転パターンによって燃費も向上させています。より安全で便利な都市型モビリティ・ソリューションに対する需要の高まりが、特に深刻な渋滞課題に直面している地域での採用を促進しています。自動車メーカーがADAS(先進運転支援システム)を自動車に組み込むにつれて、現代モビリティの重要な構成要素としてのTJAシステムの役割が顕著になってきています。

自動車メーカー各社は、アダプティブ・クルーズ・コントロールやレーン・キーピング・アシスタンスのような、TJA機能に不可欠な機能を搭載するようになってきています。これらのシステムは、ドライバーの安全性を確保しながら、低速で移動する交通に対応するためにさまざまな技術を組み合わせたものです。各国政府が安全規制を強化するなか、ADAS(先進運転支援システム)の採用が加速しています。よりスマートな半自律走行車に対する消費者の関心は、今日の市場におけるTJAシステムの重要性をさらに際立たせています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 36億米ドル |

| 予測金額 | 104億米ドル |

| CAGR | 11.5% |

市場は車種別に区分され、乗用車が2024年の市場シェアの70%以上を占めています。このセグメントは、自動車における高度な安全性と利便性機能への嗜好の高まりに後押しされ、2034年には65億米ドルを超えると予想されます。都市交通の激化に伴い、消費者は運転体験を向上させる技術を優先するようになっており、メーカー各社は中級モデルや高級モデルにTJAシステムを搭載するようになっています。半自動運転へのシフトにより、これらの機能は多くの高級車に標準装備されるようになり、技術に敏感な購入者にアピールしています。

コンポーネント別に分類すると、センサーは2024年に約39%の市場シェアを占めました。レーダー、LiDAR、カメラの技術進歩によりシステムの精度が向上し、車両が物体を検知して複雑な交通シナリオを正確にナビゲートできるようになっています。複数のソースからの入力を組み合わせるセンサー・フュージョン技術の統合により、リアルタイムでの意思決定が強化され、TJAシステムの信頼性が高まり、ユーザーにとって魅力的なものとなっています。

2024年の市場は北米がリードし、世界シェアの約35%を占めました。規制要件と、高度な機能を備えたプレミアム車に対する消費者の需要の高まりが、TJAシステムの採用を後押ししています。同地域の自動車メーカーは、安全性と利便性に対する期待の高まりに応えるため、高級車や中級車にこれらのシステムを積極的に組み込んでいます。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場範囲と定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 原材料サプライヤー

- 部品サプライヤー

- ソフトウェア開発企業

- 技術プロバイダー

- アフターマーケットプロバイダー

- エンドユーザー

- サプライヤーの状況

- 利益率分析

- 技術革新の状況

- コスト内訳分析

- 価格分析

- 特許分析

- 主要ニュース&イニシアティブ

- 規制状況

- 地域別渋滞統計

- 影響要因

- 促進要因

- 都市部の交通渋滞が自動運転システムの需要を促進。

- 政府の安全規制がADAS機能の採用を増加させています。

- センサー、カメラ、AIの進歩がTJAの信頼性を向上させています。

- 消費者は日々の通勤において快適性と利便性を優先しています。

- 業界の潜在的リスク&課題

- 高い統合コスト

- 悪天候や複雑な道路状況におけるシステム性能の問題

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- センサー

- レーダー

- LiDAR

- 超音波

- その他

- ECU

- アクチュエーター

- カメラ

- その他

第6章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- セダン

- ハッチバック

- SUV車

- 商用車

- 小型商用車(LCV)

- 大型商用車(HCV)

第7章 市場推計・予測:自動化レベル別、2021~2034年

- 主要動向

- レベル2

- レベル3

- レベル4

第8章 市場推計・予測:方式別、2021年~2034年

- 主要動向

- 車線追跡システム

- 車両検知・衝突回避システム

- 自動操舵・速度制御システム

- V2X通信統合

- その他

第9章 市場推計・予測:通信別、2021年~2034年

- 主要動向

- 車両間通信(V2V)

- 車車間通信(V2I)

- セルラーネットワークベース

- 専用近距離通信(DSRC)

第10章 市場推計・予測:販売チャネル別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第11章 市場推計・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第12章 企業プロファイル

- Aptiv PLC

- Bosch

- Continental

- Denso

- Harman

- Hitachi Astemo

- Hyundai Mobis

- Infineon Technologies

- Magna International

- Marelli

- Mercedes-Benz

- Mobileye

- NVIDIA

- NXP Semiconductors

- Renesas Electronics

- Texas Instruments

- Valeo

- Veoneer

- Volkswagen

- ZF Friedrichshafen

目次

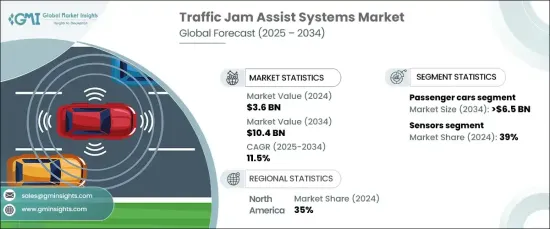

The Global Traffic Jam Assist System Market was valued at USD 3.6 billion in 2024 and is projected to grow at a CAGR of 11.5% from 2025 to 2034. This growth stems from worsening traffic congestion in urban areas due to rapid population growth and urbanization. Increasing vehicle ownership and limited infrastructure further exacerbate traffic problems, making commutes longer and more stressful. Traffic jam assist systems aim to alleviate this by automating key driving functions like acceleration, braking, and steering in heavy traffic. These features not only reduce driver fatigue but also enhance fuel efficiency through smoother driving patterns. The growing demand for safer and more convenient urban mobility solutions is driving adoption, particularly in regions facing severe congestion challenges. As manufacturers integrate advanced driver-assistance technologies into vehicles, the role of TJA systems as a key component of modern mobility is becoming more pronounced.

Automakers are increasingly incorporating features like adaptive cruise control and lane-keeping assistance, which are essential for TJA functionality. These systems combine various technologies to handle slow-moving traffic while ensuring driver safety. As governments enforce stricter safety regulations, the adoption of advanced driver-assistance systems is accelerating. Consumer interest in smarter, semi-autonomous vehicles further underscores the relevance of TJA systems in today's market.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.6 Billion |

| Forecast Value | $10.4 Billion |

| CAGR | 11.5% |

The market is segmented by vehicle type, with passenger cars accounting for over 70% of the market share in 2024. This segment is expected to exceed USD 6.5 billion by 2034, fueled by a growing preference for advanced safety and convenience features in vehicles. As urban traffic intensifies, consumers are prioritizing technologies that enhance driving experiences, prompting manufacturers to include TJA systems in mid-range and luxury models. The shift toward semi-autonomous driving has made these features standard in many high-end vehicles, appealing to tech-savvy buyers.

When categorized by components, sensors held a market share of approximately 39% in 2024. Technological advancements in radar, LiDAR, and cameras are improving system accuracy, enabling vehicles to detect objects and navigate complex traffic scenarios with precision. The integration of sensor fusion technologies, which combine inputs from multiple sources, enhances decision-making in real-time, making TJA systems more reliable and appealing to users.

North America led the market in 2024, capturing around 35% of the global share. Regulatory requirements and growing consumer demand for premium vehicles with advanced features have driven the adoption of TJA systems. Automakers in the region are actively integrating these systems into luxury and mid-range vehicles to meet evolving expectations for safety and convenience.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material suppliers

- 3.1.2 Component suppliers

- 3.1.3 Software developers

- 3.1.4 Technology providers

- 3.1.5 Aftermarket providers

- 3.1.6 End users

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Cost breakdown analysis

- 3.6 Price analysis

- 3.7 Patent analysis

- 3.8 Key news & initiatives

- 3.9 Regulatory landscape

- 3.10 Traffic congestion statistics, by region

- 3.11 Impact forces

- 3.11.1 Growth drivers

- 3.11.1.1 Urban traffic congestion is driving demand for automated driving systems

- 3.11.1.2 Government safety regulations are increasing the adoption of ADAS features

- 3.11.1.3 Advancements in sensors, cameras, and AI are improving the reliability of TJA

- 3.11.1.4 Consumers are prioritizing comfort and convenience in daily commutes

- 3.11.2 Industry pitfalls & challenges

- 3.11.2.1 High integration costs

- 3.11.2.2 System performance issues in adverse weather and complex road conditions

- 3.11.1 Growth drivers

- 3.12 Growth potential analysis

- 3.13 Porter’s analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Sensors

- 5.2.1 Radar

- 5.2.2 LiDAR

- 5.2.3 Ultrasonic

- 5.2.4 Others

- 5.3 ECUs

- 5.4 Actuators

- 5.5 Cameras

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Sedans

- 6.2.2 Hatchbacks

- 6.2.3 SUVs

- 6.3 Commercial vehicles

- 6.3.1 Light Commercial Vehicles (LCV)

- 6.3.2 Heavy Commercial Vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Level of Automation, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Level 2

- 7.3 Level 3

- 7.4 Level 4

Chapter 8 Market Estimates & Forecast, By Method, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Lane tracking system

- 8.3 Vehicle detection and collision avoidance system

- 8.4 Auto steering and speed control system

- 8.5 V2X communication integration

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Communication, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Vehicle-to-Vehicle (V2V)

- 9.3 Vehicle-to-Infrastructure (V2I)

- 9.4 Cellular network-based

- 9.5 Dedicated Short-Range Communication (DSRC)

Chapter 10 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 OEM

- 10.3 Aftermarket

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Southeast Asia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 South Africa

- 11.6.3 Saudi Arabia

Chapter 12 Company Profiles

- 12.1 Aptiv PLC

- 12.2 Bosch

- 12.3 Continental

- 12.4 Denso

- 12.5 Harman

- 12.6 Hitachi Astemo

- 12.7 Hyundai Mobis

- 12.8 Infineon Technologies

- 12.9 Magna International

- 12.10 Marelli

- 12.11 Mercedes-Benz

- 12.12 Mobileye

- 12.13 NVIDIA

- 12.14 NXP Semiconductors

- 12.15 Renesas Electronics

- 12.16 Texas Instruments

- 12.17 Valeo

- 12.18 Veoneer

- 12.19 Volkswagen

- 12.20 ZF Friedrichshafen

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 175 Pages

- 納期

- 2~3営業日