|

市場調査レポート

商品コード

1665402

自動車用ベルトスターター発電機の市場機会、成長促進要因、産業動向分析、2025~2034年予測Automotive Belt Starter Generator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用ベルトスターター発電機の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2024年12月27日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

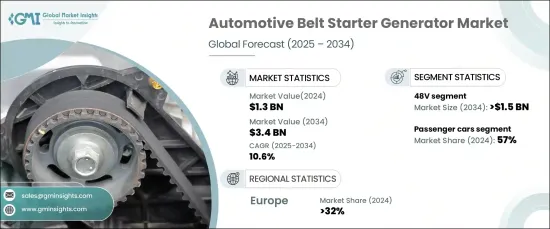

自動車用ベルトスターター発電機の世界市場は、2024年には13億米ドルとなり、2025~2034年にかけてCAGR 10.6%で成長すると予測されています。

優れた性能と手頃な価格で知られる48Vシステムに対する需要の高まりが、特にマイルドハイブリッド車でのBSGシステムの採用を後押ししています。これらのシステムは、より高い出力を提供することで従来の12Vシステムを凌駕し、マイルドハイブリッドパワートレインの効率を高めています。また、回生ブレーキ機能を強化し、ブレーキング時に多くのエネルギーを回収・蓄積して燃料効率を最適化します。エンジンの仕事量を減らし、より優れたエネルギー管理を可能にすることで、これらのシステムは輸送における持続可能性に大きく貢献します。

ハイブリッド車や電気自動車へのシフトも、BSG市場の推進に重要な役割を果たしています。自動車メーカーは、より厳しい排ガス規制に対応し、エコフレンドリーモビリティソリューションへの需要の高まりに応えるため、これらのシステムを統合しています。スターターモーターと発電機機能を組み合わせたBSGシステムは、ハイブリッド車や電気自動車のパワートレインに不可欠なコンポーネントです。エネルギー利用を改善し、回生ブレーキをサポートし、全体的な車両性能を向上させるため、エコフレンドリー自動車技術への移行における重要な技術革新となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 13億米ドル |

| 予測金額 | 34億米ドル |

| CAGR | 10.6% |

市場は製品別に12Vシステムと48Vシステムに区分されます。2024年には、48Vセグメントが市場シェアの58%以上を占め、2034年には15億米ドルを超えると予測されています。これらのシステムは、電動パワーステアリング、エアコン、回生ブレーキなどの重要な車両機能のために追加電力を供給する能力により、好まれています。これらのシステムは、よりスムーズな加速、燃費の向上、より効果的なエネルギー回収を実現し、厳しい排出ガス規制に対応する自動車メーカーにとって理想的な選択肢となります。

車種別では、市場は乗用車、オフハイウェイ車、商用車に分類されます。乗用車は2024年の市場シェアの約57%を占めています。これらの車両は48V BSGシステムを活用して燃費向上と排出ガス削減を達成し、電気自動車に完全に移行しなくても費用対効果の高いソリューションを求める消費者に対応しています。スタート・ストップ機能、回生ブレーキ、内燃エンジンの追加トルクなどの特徴は、これらのシステムを乗用車セグメントにとって非常に魅力的なものとし、市場浸透をさらに促進しています。

欧州は2024年に世界市場シェアの32%以上を占める主要地域に浮上し、ドイツが大きく貢献しています。主要企業がハイブリッド車や電気自動車技術に多額の投資を行っている同国の堅調な自動車部門が、この優位性を支えています。CO2排出を抑制するための厳しい規制とサステイナブル輸送への注目が、自動車メーカーに48V BSGシステムを広く採用させ、市場におけるドイツのリーダーシップを強化しています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推定の主要動向

- 予測モデル

- 一次調査と検証

- 一次情報

- データマイニングソース

- 市場定義

第2章 エグゼクティブサマリー

第3章 産業洞察

- エコシステム分析

- サプライヤーの状況

- 自動車OEM

- 技術プロバイダー

- アフターマーケットとサービスプロバイダー

- エンドユーザー

- 利益率分析

- コスト内訳分析

- 技術とイノベーションの展望

- 主要ニュースと取り組み

- 価格分析

- 規制状況

- 影響要因

- 促進要因

- 排出ガス規制の強化

- 燃料効率に対する需要の高まり

- ハイブリッド車と電気自動車の採用増加

- 促進要因

3.9.1.4.48Vシステムの性能と費用対効果の向上

- ベルトスターター発電機設計の技術的進歩

- 産業の潜在的リスク・課題

- 技術的・統合的課題

- フルハイブリッドや電気パワートレインとの競合

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推定・予測:技術別、2021~2034年

- 主要動向

- マイルドハイブリッド

- マイクロハイブリッド

第6章 市場推定・予測:製品別、2021~2034年

- 主要動向

- 12V

- 48V

第7章 市場推定・予測:車両別、2021~2034年

- 主要動向

- 乗用車

- セダン

- SUV

- ハッチバック

- 商用車

- LCV

- HCV

- オフハイウェイ車

第8章 市場推定・予測:コンポーネント別、2021~2034年

- 主要動向

- モーター/発電機

- パワーエレクトロニクス

- 機械式カップリング

- 制御システム

第9章 市場推定・予測:冷却タイプ別、2021~2034年

- 主要動向

- 空冷

- 液冷

- ハイブリッド冷却

第10章 市場推定・予測:流通チャネル別、2021~2034年

- 主要動向

- OEM

- アフターマーケット

第11章 市場予測:地域別市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第12章 企業プロファイル

- Bosch

- Continental

- Dayco

- Hyundai

- Infineon

- Magneti Marelli

- MTA

- Nexteer

- Onsemi

- Schaeffler Group

- SEG Automotive

- Sona Comstar

- Syensqo

- Valeo

- Vitesco Technologies

- ZF Friedrichshafen

The Global Automotive Belt Starter Generator Market was valued at USD 1.3 billion in 2024 and is anticipated to grow at a CAGR of 10.6% from 2025 to 2034. The increasing demand for 48V systems, known for their superior performance and affordability, is propelling the adoption of BSG systems, particularly in mild-hybrid vehicles. These systems outperform traditional 12V counterparts by delivering higher power output, which boosts the efficiency of mild-hybrid powertrains. They also enhance regenerative braking capabilities, capturing and storing more energy during braking to optimize fuel efficiency. By reducing the engine's workload and enabling better energy management, these systems contribute significantly to sustainability in transportation.

The shift towards hybrid and electric vehicles also plays a critical role in driving the BSG market. Automakers are integrating these systems to align with stricter emissions regulations and meet the growing demand for eco-friendly mobility solutions. BSG systems, which combine starter motor and generator functions, are vital components in hybrid and electric powertrains. They improve energy utilization, support regenerative braking, and enhance overall vehicle performance, making them a key innovation in the transition to greener automotive technologies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.3 Billion |

| Forecast Value | $3.4 Billion |

| CAGR | 10.6% |

The market is segmented by product into 12V and 48V systems. In 2024, the 48V segment accounted for over 58% of the market share and is projected to surpass USD 1.5 billion by 2034. These systems are preferred due to their ability to deliver additional electrical power for critical vehicle functions like electric power steering, air conditioning, and regenerative braking. They ensure smoother acceleration, improved fuel economy, and more effective energy recovery, positioning themselves as the ideal choice for automakers addressing stringent emissions standards.

In terms of vehicle type, the market is categorized into passenger cars, off-highway vehicles, and commercial vehicles. Passenger cars held approximately 57% of the market share in 2024. These vehicles leverage 48V BSG systems to achieve better fuel efficiency and reduced emissions, catering to consumers seeking cost-effective solutions without transitioning fully to electric vehicles. Features like start-stop functionality, regenerative braking, and additional torque for internal combustion engines make these systems highly attractive for the passenger car segment, further driving their market penetration.

Europe emerged as the leading region, capturing more than 32% of the global market share in 2024, with Germany being a significant contributor. The country's robust automotive sector, featuring key players heavily investing in hybrid and electric vehicle technologies, supports this dominance. Strict regulations to curb CO2 emissions and a focus on sustainable transportation have led to widespread adoption of 48V BSG systems among automakers, reinforcing Germany's leadership in the market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Automotive OEMs

- 3.2.2 Technology providers

- 3.2.3 Aftermarket and service providers

- 3.2.4 End users

- 3.3 Profit margin analysis

- 3.4 Cost breakdown analysis

- 3.5 Technology & innovation landscape

- 3.6 Key news & initiatives

- 3.7 Pricing analysis

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rising implementation of stringent emission regulations

- 3.9.1.2 Growing demand for fuel efficiency

- 3.9.1.3 Increasing adoption of hybrid and electric vehicles

- 3.9.1 Growth drivers

3.9.1.4. Improved performance and cost-effectiveness of 48 V systems

- 3.9.1.5 Technological advancements in belt starter generator design

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Technological and integration challenges

- 3.9.2.2 Competition from full hybrid and electric powertrains

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Mild hybrid

- 5.3 Micro hybrid

Chapter 6 Market Estimates & Forecast, By Product, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 12V

- 6.3 48V

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Sedan

- 7.2.2 SUV

- 7.2.3 Hatchback

- 7.3 Commercial vehicle

- 7.3.1 LCV

- 7.3.2 HCV

- 7.4 Off highway vehicle

Chapter 8 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Motor/generator

- 8.3 Power electronics

- 8.4 Mechanical coupling

- 8.5 Control systems

Chapter 9 Market Estimates & Forecast, By Cooling Type, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Air-cooled

- 9.3 Liquid-cooled

- 9.4 Hybrid-cooled

Chapter 10 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 OEM

- 10.3 Aftermarket

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 ANZ

- 11.4.6 Southeast Asia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 South Africa

- 11.6.3 Saudi Arabia

Chapter 12 Company Profiles

- 12.1 Bosch

- 12.2 Continental

- 12.3 Dayco

- 12.4 Hyundai

- 12.5 Infineon

- 12.6 Magneti Marelli

- 12.7 MTA

- 12.8 Nexteer

- 12.9 Onsemi

- 12.10 Schaeffler Group

- 12.11 SEG Automotive

- 12.12 Sona Comstar

- 12.13 Syensqo

- 12.14 Valeo

- 12.15 Vitesco Technologies

- 12.16 ZF Friedrichshafen