|

市場調査レポート

商品コード

1665390

三相ストリングインバータ市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Three Phase String Inverter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 三相ストリングインバータ市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2024年12月26日

発行: Global Market Insights Inc.

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

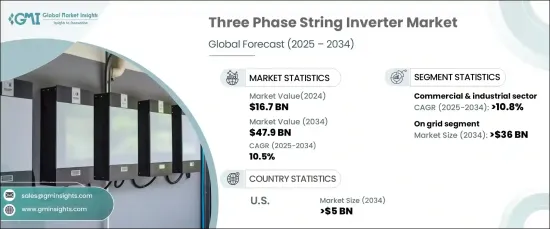

世界の三相ストリングインバータ市場は、2024年に167億米ドルと評価され、2025~2034年にかけて10.5%のCAGRで成長すると予測されています。

これらのインバータは、太陽光発電ソーラーパネルによって生成された直流電力を、三相電力システムに適合する交流電力に変換するために特別に設計されています。より高い出力に対応できるため、これらのインバータは業務用、産業用、公共施設規模の太陽光発電設備で広く使用されています。三相グリッドシステムとの統合が重要な大規模セットアップにおいて、優れた性能を発揮します。

産業が再生可能エネルギーソリューションにシフトするにつれ、三相ストリングインバータの需要は増加しています。高出力を効率的に処理し、多相にわたってバランスの取れた配電を確保する能力が、採用増加の主要要因となっています。堅牢な三相配電システムを持つ地域が成長を続ける中、グリッドとシームレスに統合するソリューションのニーズも拡大しています。これが製品の需要を牽引しています。さらに、電圧と周波数の変動を管理するこれらのインバータの能力は、今日の近代的な電力ネットワークにおける重要な要素である送電網の安定性の維持に役立っており、市場の成長を後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 167億米ドル |

| 予測金額 | 479億米ドル |

| CAGR | 10.5% |

費用対効果が高く、拡大性の高いインバータへの嗜好が高まっていることも、市場促進要因のひとつです。これらのインバータは、設置の複雑さや配線要件を最小限に抑えるため、大規模なエネルギープロジェクトにとってより魅力的なものとなっています。再生可能エネルギー導入の奨励に重点を置く政府の取り組みが、ネット・ゼロ・カーボン目標の達成を目指す施策とともに増加していることも、産業の成長をさらに後押しします。これらの施策は、環境の持続可能性を支援するだけでなく、クリーンエネルギー源に投資する企業のインセンティブにもなり、市場全体の展望を向上させています。

オングリッドセグメントは、急速な都市化と、特に商業・産業部門におけるエネルギー需要の増加に牽引され、2034年までに360億米ドルを超えると予測されています。オングリッドシステムは、信頼性と拡大性に優れたエネルギー変換ソリューションを提供し、増大するエネルギー需要を満たすと同時に、設置コストとメンテナンス・コストを低減します。脱炭素化とクリーンエネルギー導入に向けた世界の推進力は、このセグメントの成長を補完します。

商業・産業部門は着実に成長し、2034年のCAGRは10.5%を超えると予想されます。企業が持続可能性と二酸化炭素排出量の削減にますます重点を置くようになるにつれて、太陽光発電システムの需要が拡大しています。政府の奨励策や有利な規制は、特にこうしたセグメントでの太陽光発電導入の加速に大きな役割を果たしています。

米国では、三相ストリングインバータ市場は2034年までに52億米ドルに達すると見られています。投資税額控除(ITC)のような政府の優遇措置により、太陽光発電設備に対して最大26%の税額控除が提供されるため、効率的なインバータに対する需要は拡大すると予想されます。さらに、太陽光発電システムの継続的なコスト低下が、頻繁な停電や自然災害とともに市場拡大の原動力となっています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 基本推定と計算

- 予測モデル

- 一次調査と検証

- 一次情報

- データマイニングソース

- 市場定義

第2章 エグゼクティブサマリー

第3章 産業洞察

- 産業エコシステム

- 規制状況

- 産業への影響要因

- 促進要因

- 産業の潜在的リスク・課題

- 成長可能性分析

- ポーター分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- PESTEL分析

第4章 競争情勢

- イントロダクション

- 戦略ダッシュボード

- イノベーションと技術の展望

第5章 市場規模・予測:接続性別、2021~2034年

- 主要動向

- スタンドアロン

- オングリッド

第6章 市場規模・予測:用途別、2021~2034年

- 主要動向

- 住宅用

- 商業・産業

- 公益事業

第7章 市場規模・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- イタリア

- オランダ

- 英国

- フランス

- アジア太平洋

- 中国

- オーストラリア

- インド

- 日本

- 韓国

- 中東・アフリカ

- イスラエル

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ラテンアメリカ

- ブラジル

- メキシコ

- チリ

第8章 企業プロファイル

- APsystems

- Canadian Solar

- Chint Power Systems

- Fimer

- Goldi Solar

- Huawei Technologies

- INVTSolar

- LEDVANCE

- NingBo Deye Inverter Technology

- SUNGROW

- UTL Solar

- Veichi Electric

The Global Three Phase String Inverter Market was valued at USD 16.7 billion in 2024 and is projected to grow at a CAGR of 10.5% from 2025 to 2034. These inverters are specifically designed to convert the DC electricity generated by photovoltaic solar panels into AC electricity that is compatible with three-phase power systems. Due to their ability to handle higher power outputs, these inverters are widely used in commercial, industrial, and utility-scale solar installations. They offer excellent performance in large-scale setups, where the integration with three-phase grid systems is critical.

The demand for three-phase string inverters is increasing as industries shift towards renewable energy solutions. Their ability to efficiently handle high power outputs and ensure balanced electricity distribution across multiple phases is a key factor in their rising adoption. As regions with robust three-phase electricity distribution systems continue to grow, the need for solutions that seamlessly integrate with the grid is also expanding. This drives the product's demand. Furthermore, the ability of these inverters to manage voltage and frequency fluctuations is helping maintain grid stability, a crucial factor in today's modern power networks, and boosting market growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $16.7 Billion |

| Forecast Value | $47.9 Billion |

| CAGR | 10.5% |

The growing preference for cost-effective and scalable inverters is another key driver for the market. These inverters minimize installation complexities and cabling requirements, making them more attractive to large-scale energy projects. The increasing government initiatives focused on encouraging renewable energy adoption, along with policies aimed at achieving net-zero carbon goals, will further propel the industry's growth. These policies not only support environmental sustainability but also incentivize businesses to invest in clean energy sources, enhancing the overall market outlook.

The on-grid segment is projected to surpass USD 36 billion by 2034, driven by rapid urbanization and rising energy demand, particularly in commercial and industrial sectors. On-grid systems provide reliable, scalable energy conversion solutions that help meet growing energy needs while offering lower installation and maintenance costs. The global push toward decarbonization and clean energy adoption will complement the growth of this segment.

The commercial and industrial sectors are expected to experience a steady rise, with the market growing at a CAGR of over 10.5% through 2034. As businesses increasingly focus on sustainability and reducing their carbon footprints, the demand for solar photovoltaic systems is expanding. Government incentives and favorable regulations are playing a significant role in accelerating solar adoption, particularly in these sectors.

In the U.S., the three-phase string inverter market is set to reach USD 5.2 billion by 2034. With government incentives such as the Investment Tax Credit (ITC), offering up to 26% tax credits for solar installations, the demand for efficient inverters is expected to grow. Additionally, the continued decline in solar energy system costs, along with frequent power outages and natural disasters, is driving the market's expansion.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Connectivity, 2021 – 2034 (USD Billion & MW)

- 5.1 Key trends

- 5.2 Standalone

- 5.3 On grid

Chapter 6 Market Size and Forecast, By Application, 2021 – 2034 (USD Billion & MW)

- 6.1 Key trends

- 6.2 Residential

- 6.3 Commercial & industrial

- 6.4 Utility

Chapter 7 Market Size and Forecast, By Region, 2021 – 2034 (USD Billion & MW)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 Italy

- 7.3.3 Netherlands

- 7.3.4 UK

- 7.3.5 France

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 India

- 7.4.4 Japan

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Israel

- 7.5.2 Saudi Arabia

- 7.5.3 UAE

- 7.5.4 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Mexico

- 7.6.3 Chile

Chapter 8 Company Profiles

- 8.1 APsystems

- 8.2 Canadian Solar

- 8.3 Chint Power Systems

- 8.4 Fimer

- 8.5 Goldi Solar

- 8.6 Huawei Technologies

- 8.7 INVTSolar

- 8.8 LEDVANCE

- 8.9 NingBo Deye Inverter Technology

- 8.10 SUNGROW

- 8.11 UTL Solar

- 8.12 Veichi Electric