|

市場調査レポート

商品コード

1665351

自動車用三元触媒コンバーターの市場機会、成長促進要因、産業動向分析、2025~2034年予測Automotive Three-Way Catalytic Converter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用三元触媒コンバーターの市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2024年12月23日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

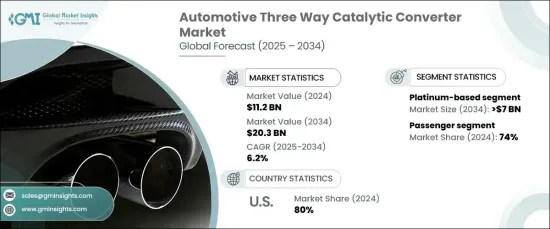

自動車用三元触媒コンバータの世界市場は、2024年には112億米ドルとなり、2025~2034年にかけてCAGR 6.2%で堅調に拡大する展望です。

この成長は、触媒コンバータのような自動車部品の需要が急増し続け、世界中で自動車の生産と販売が増加していることが要因となっています。内燃機関車(ICE)の普及により、厳しい環境基準を満たすための先進的排出ガス制御システムの必要性が高まっています。さらに、パーソナルモビリティと輸送サービスへの嗜好の高まりが、市場の需要をさらに押し上げています。

世界的に厳しい排出ガス規制が市場成長の主要要因となっています。各国政府は、大気汚染と闘い、温室効果ガスの排出を抑制するために、より厳しい施策を実施しています。これらの指令は、一酸化炭素、窒素酸化物、炭化水素のような有害汚染物質の大幅な削減を要求しています。その結果、メーカーはますます厳しくなる性能基準に適合する、革新的で効率的かつ耐久性のある触媒コンバータに注力しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 112億米ドル |

| 予測金額 | 203億米ドル |

| CAGR | 6.2% |

材料タイプ別に見ると、市場はプラチナベース、パラジウムベース、ロジウムベースのコンバータに分類されます。2024年には、プラチナベースの触媒コンバータが40%の大きなシェアを占め、2034年までに70億米ドルを生み出すと予測されています。プラチナの卓越した触媒特性により、プラチナは効果的な排ガス規制システムに不可欠なものとなり、厳しい規制要件への適合が可能になります。排ガス処理におけるプラチナの高性能と、環境維持への関心の高まりが、主要市場でのプラチナの採用を後押ししています。

車種別では、乗用車が2024年の市場の74%を占め、圧倒的なシェアを占めています。低燃費でエコフレンドリー自動車に対する消費者の需要の高まりが、このセグメント成長の主要因となっています。排出ガスと持続可能性に対する意識の高まりが自動車メーカーに低排出ガス技術の開発を促し、乗用車用の触媒コンバータのクリーン化と効率化につながっています。

米国の自動車用三元触媒コンバータ市場は、2024年に80%という驚異的なシェアを獲得しました。自動車の排出ガス削減に重点を置く規制が、メーカーに最先端の触媒技術の採用を促しています。材料、基材設計、耐熱部品の革新により、コンバータの効率と耐久性が向上し、進化する環境基準への適合が確実になっています。クリーン技術に対する連邦政府の優遇措置と投資は、この地域の成長をさらに加速させています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推定の主要動向

- 予測モデル

- 一次調査と検証

- 一次情報

- データマイニングソース

- 市場スコープと定義

第2章 エグゼクティブサマリー

第3章 産業洞察

- エコシステム分析

- 原料サプライヤー

- 部品サプライヤー

- メーカー

- 流通チャネル

- エンドユーザー

- サプライヤーの状況

- 利益率分析

- 技術革新の状況

- 特許分析

- 主要ニュース&イニシアチブ

- 規制状況

- コスト分析

- 影響要因

- 促進要因

- 研究開発と新製品開発への急速な投資

- 環境規制の増加

- 触媒コンバータの技術進歩

- 低燃費車に対する需要の高まり

- 新興市場における自動車需要の高まり

- 産業の潜在的リスク・課題

- 高い製造コスト

- 規制上のハードルとコンプライアンスの問題

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推定・予測:材料別、2021~2034年

- 主要動向

- プラチナベース

- パラジウムベース

- ロジウムベース

第6章 市場推定・予測:車両別、2021~2034年

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV車

- 商用車

- 小型商用車(LCV)

- 大型商用車(HCV)

第7章 市場推定・予測:推進力別、2021~2034年

- 主要動向

- ガソリン

- ディーゼル

- その他

第8章 市場推定・予測:流通チャネル別、2021~2034年

- 主要動向

- OEM

- アフターマーケット

第9章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- ニュージーランド

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- BASF SE

- Benteler

- BorgWarner

- Bosal

- Calsonic

- Corning

- Delphi

- Denso

- Eberspacher

- Faurecia

- Haldex

- Johnson Matthey

- Magna

- Marelli

- Sango

- Tenneco

- Umicore

- Valeo

- Walker Exhaust Systems

- Yutaka

The Global Automotive Three-Way Catalytic Converter Market, valued at USD 11.2 billion in 2024, is set to expand at a robust CAGR of 6.2% from 2025 to 2034. This growth is fueled by increasing vehicle production and sales worldwide as demand for automotive components such as catalytic converters continues to soar. The widespread use of internal combustion engine (ICE) vehicles has intensified the need for advanced emission control systems to meet stringent environmental standards. Moreover, the rising preference for personal mobility and transportation services is further propelling market demand.

Stringent emissions regulations globally are a major driver behind market growth. Governments are implementing tougher policies to combat air pollution and curb greenhouse gas emissions. These mandates require significant reductions in harmful pollutants like carbon monoxide, nitrogen oxides, and hydrocarbons. As a result, manufacturers are focusing on innovative, efficient, and durable catalytic converters that comply with increasingly rigorous performance standards.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $11.2 Billion |

| Forecast Value | $20.3 Billion |

| CAGR | 6.2% |

By material type, the market is categorized into platinum-based, palladium-based, and rhodium-based converters. In 2024, platinum-based catalytic converters held a significant 40% share, with projections to generate USD 7 billion by 2034. The exceptional catalytic properties of platinum make it integral to effective emission control systems, enabling compliance with stringent regulatory requirements. Platinum's high-performance capabilities in treating exhaust gases and the growing focus on environmental sustainability are driving its adoption in key markets.

In terms of vehicle type, passenger vehicles dominated the market in 2024 with a commanding 74% share. Increasing consumer demand for fuel-efficient and environmentally friendly vehicles is a key factor in the segment growth. Rising awareness of emissions and sustainability is encouraging automakers to develop low-emission technologies, leading to cleaner and more efficient catalytic converters for passenger vehicles.

The U.S. market for automotive three-way catalytic converters captured an impressive 80% share in 2024. Regulatory mandates focused on reducing vehicle emissions are spurring manufacturers to adopt cutting-edge catalyst technologies. Innovations in materials, substrate designs, and heat-resistant components are enhancing the efficiency and durability of converters, ensuring compliance with evolving environmental standards. Federal incentives and investments in clean technologies are further accelerating growth in the region.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material providers

- 3.1.2 Component suppliers

- 3.1.3 Manufacturers

- 3.1.4 Distribution channel

- 3.1.5 End users

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Cost analysis

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rapid investment in R&D and new product development

- 3.9.1.2 Increasing environmental regulations

- 3.9.1.3 Technological advancements in catalytic converters

- 3.9.1.4 Rising demand for fuel-efficient vehicles

- 3.9.1.5 Growing vehicle demand in emerging markets

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High manufacturing costs

- 3.9.2.2 Regulatory hurdles and compliance issues

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Material, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Platinum-based

- 5.3 Palladium-based

- 5.4 Rhodium-based

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger vehicles

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUVs

- 6.3 Commercial vehicles

- 6.3.1 Light Commercial Vehicles (LCVs)

- 6.3.2 Heavy Commercial Vehicles (HCVs)

Chapter 7 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Gasoline

- 7.3 Diesel

- 7.4 Others

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 ANZ

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 BASF SE

- 10.2 Benteler

- 10.3 BorgWarner

- 10.4 Bosal

- 10.5 Calsonic

- 10.6 Corning

- 10.7 Delphi

- 10.8 Denso

- 10.9 Eberspächer

- 10.10 Faurecia

- 10.11 Haldex

- 10.12 Johnson Matthey

- 10.13 Magna

- 10.14 Marelli

- 10.15 Sango

- 10.16 Tenneco

- 10.17 Umicore

- 10.18 Valeo

- 10.19 Walker Exhaust Systems

- 10.20 Yutaka