|

市場調査レポート

商品コード

1665331

凝固分析装置の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Coagulation Analyzers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 凝固分析装置の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2024年12月23日

発行: Global Market Insights Inc.

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

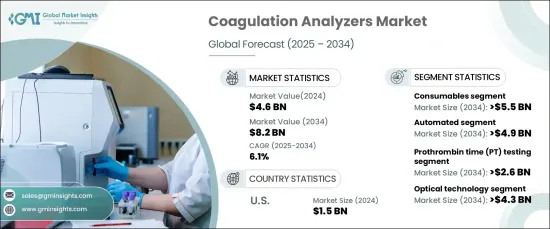

凝固分析装置の世界市場は、2024年に46億米ドルに達し、2025~2034年にかけてCAGR 6.1%で力強く成長する展望です。

この成長の原動力となっているのは、血友病や血栓症などの血液疾患の有病率の上昇に加え、座りがちなライフスタイルや高齢化、肥満が原因となる心血管合併症の増加です。予防医療への意識が高まり、早期診断検査が普及するにつれて、医療施設での凝固分析装置の採用が加速しています。

市場は製品タイプ別に消耗品と機器に区分され、消耗品が主流を占めると予想されます。CAGR6.3%で成長すると予測される消耗品セグメントは、2034年までに55億米ドルを創出すると予測されます。診断センターや検査室がルーチンと専門的な凝固検査にこれらの製品を多用しているためです。試薬技術の進歩は自動化システムとの適合性を高め、高性能検査環境における効率と精度を向上させ、需要をさらに促進しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 46億米ドル |

| 予測金額 | 82億米ドル |

| CAGR | 6.1% |

検査タイプ別では、プロトロンビン時間(PT)検査、活性化部分トロンボプラスチン時間(aPTT)検査、Dダイマー検査、フィブリノゲン検査、その他の検査が含まれます。PT検査はCAGR 6.6%を達成し、2034年までに26億米ドルに達すると予測されています。この検査は、凝固障害の診断、抗凝固療法のモニタリング、肝機能の評価、出血異常の検出に不可欠です。日常的な診断手順と先進的診断手順の両方において重要な役割を果たすことが、市場成長への大きな貢献を裏付けています。

米国では、凝固分析装置市場は2024年に15億米ドルに達し、2034年までCAGR 5.3%の安定した成長が予測されています。米国は北米市場をリードしており、先進的医療インフラ、多額の医療費、心房細動のような慢性疾患の高い有病率などの恩恵を受けています。抗凝固療法の効果的なモニタリングがますます不可欠になるにつれ、凝固検査、特にPTとaPTTの需要は増加の一途をたどっています。さらに、臨床検査室における完全自動化システムの統合は、ワークフローの効率を高め、大量検査のニーズを満たし、国内市場の優位性を強化しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 産業洞察

- エコシステム分析

- 産業への影響要因

- 促進要因

- 心血管と血液関連疾患の有病率の増加

- ポイントオブケア診断機器に対する需要の高まり

- 凝固分析装置の技術的進歩

- 疾患の早期診断に対する意識の高まり

- 産業の潜在的リスク・課題

- 機器承認のための厳しい規制要件

- 先進的分析装置の操作に熟練した専門家の不足

- 促進要因

- 成長可能性分析

- 規制状況

- 技術

- ギャップ分析

- ポーター分析

- PESTEL分析

- 今後の市場動向

- バリューチェーン分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 企業マトリックス分析

- 主要市場参入企業の競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推定・予測:製品タイプ別、2021~2034年

- 主要動向

- 消耗品

- 機器

第6章 市場推定・予測:モード別、2021~2034年

- 主要動向

- 自動化

- 半自動

- 手動

第7章 市場推定・予測:検査タイプ別、2021~2034年

- 主要動向

- プロトロンビン時間(PT)検査

- 活性化部分トロンボプラスチン時間(aPTT)検査

- Dダイマー検査

- フィブリノゲン検査

- その他

第8章 市場推定・予測:技術別、2021~2034年

- 主要動向

- 光学技術

- 電気化学技術

- 機械技術

- その他

第9章 市場推定・予測:最終用途別、2021~2034年

- 主要動向

- 病院

- 診断ラボ

- 学術・研究機関

- その他

第10章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Abbott

- DiaSys

- Erba Mannheim

- HELENA LABORATORIES

- HemoSonics

- HORIBA

- iLine

- mindray

- RANDOX

- Roche

- SEKISUI

- SIEMENS Healthineers

- Stago

- sysmex

- werfen

The Global Coagulation Analyzers Market reached USD 4.6 billion in 2024 and is poised to grow at a robust CAGR of 6.1% from 2025 to 2034. This growth is fueled by a rising prevalence of blood disorders such as hemophilia and thrombosis, alongside an increase in cardiovascular complications driven by sedentary lifestyles, aging populations, and obesity. As awareness of preventive healthcare expands and early diagnostic testing gains traction, the adoption of coagulation analyzers across healthcare facilities is accelerating.

The market is segmented by product type into consumables and instruments, with consumables expected to dominate. Projected to grow at a CAGR of 6.3%, the consumables segment is anticipated to generate USD 5.5 billion by 2034. The consistent demand for reagents, calibrators, and other essential consumables underpins this growth, as diagnostic centers and laboratories rely heavily on these products for routine and specialized coagulation testing. Advancements in reagent technology are enhancing compatibility with automated systems, driving efficiency and precision in high-throughput testing environments, further fueling demand.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.6 Billion |

| Forecast Value | $8.2 Billion |

| CAGR | 6.1% |

By test type, the market encompasses prothrombin time (PT) testing, activated partial thromboplastin time (aPTT) testing, D-dimer testing, fibrinogen testing, and other tests. PT testing is forecasted to achieve a CAGR of 6.6%, reaching USD 2.6 billion by 2034. This test is vital for diagnosing clotting disorders, monitoring anticoagulant therapies, assessing liver function, and detecting bleeding abnormalities. Its critical role in both routine and advanced diagnostic procedures underscores its significant contribution to market growth.

In the United States, the coagulation analyzers market reached USD 1.5 billion in 2024 and is projected to grow at a steady CAGR of 5.3% through 2034. The U.S. leads the North American market, benefiting from advanced healthcare infrastructure, substantial healthcare spending, and a high prevalence of chronic conditions like atrial fibrillation. The demand for coagulation tests, particularly PT and aPTT, continues to rise as effective monitoring of anticoagulant therapies becomes increasingly essential. Moreover, the integration of fully automated systems in clinical laboratories is enhancing workflow efficiency, meeting the needs of high-volume testing, and reinforcing the country's market dominance.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of cardiovascular and blood-related disorders

- 3.2.1.2 Growing demand for point-of-care diagnostic devices

- 3.2.1.3 Technological advancements in coagulation analyzers

- 3.2.1.4 Rising awareness about early disease diagnosis

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory requirements for device approval

- 3.2.2.2 Lack of skilled professionals for operating advanced analyzers

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Gap analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Future market trends

- 3.10 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Consumables

- 5.3 Instruments

Chapter 6 Market Estimates and Forecast, By Mode, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Automated

- 6.3 Semi-automated

- 6.4 Manual

Chapter 7 Market Estimates and Forecast, By Test Type, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Prothrombin time (PT) testing

- 7.3 Activated partial thromboplastin time (aPTT) testing

- 7.4 D-dimer testing

- 7.5 Fibrinogen testing

- 7.6 Other test types

Chapter 8 Market Estimates and Forecast, By Technology, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Optical technology

- 8.3 Electrochemical technology

- 8.4 Mechanical technology

- 8.5 Other technologies

Chapter 9 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Diagnostic laboratories

- 9.4 Academic and research institutes

- 9.5 Other end users

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Abbott

- 11.2 DiaSys

- 11.3 Erba Mannheim

- 11.4 HELENA LABORATORIES

- 11.5 HemoSonics

- 11.6 HORIBA

- 11.7 iLine

- 11.8 mindray

- 11.9 RANDOX

- 11.10 Roche

- 11.11 SEKISUI

- 11.12 SIEMENS Healthineers

- 11.13 Stago

- 11.14 sysmex

- 11.15 werfen