|

市場調査レポート

商品コード

1665313

非凝縮式低温産業用ボイラーの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Non-Condensing Low Temperature Industrial Boiler Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 非凝縮式低温産業用ボイラーの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2024年12月20日

発行: Global Market Insights Inc.

ページ情報: 英文 140 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

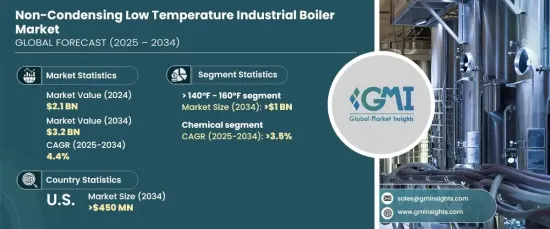

世界の非凝縮式低温産業用ボイラー市場は、2024年に21億米ドルと評価され、2025~2034年にかけてCAGR 4.4%で成長すると予測されています。

この成長の原動力となっているのは、老朽化した産業システムの近代化とボイラーインフラの戦略的アップグレードです。エネルギー効率の高い技術への投資と、耐久性と耐腐食性に優れた部品の統合が、産業の楽観的な展望に寄与しています。

140~160°Fの温度範囲は、2034年までに10億米ドルの売上になると予測されています。このセグメントの成長を牽引しているのは、精製所、食品加工、化学製造など、精密な温度制御を必要とするセグメントでの使用です。この範囲の非凝縮ボイラーは、厳しい条件下で最適な運転効率と安定した性能を発揮するように設計されています。メーカー各社は、製品の寿命を延ばすために先進的な材料や革新的な設計を活用し、耐久性を高めることにますます力を注いでいます。モノのインターネット(IoT)対応の遠隔モニタリングと予知保全システムの統合により、ダウンタイムの削減、運用の最適化、産業全体におけるこれらのシステムの採用拡大がさらに期待されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 21億米ドル |

| 予測金額 | 32億米ドル |

| CAGR | 4.4% |

化学部門は、2034年まで3.5%の成長率を維持する展望です。この成長の原動力となっているのは、排出量の削減とエネルギー管理の改善を目的とした、厳しい環境規制の導入の増加です。最新の産業用ボイラーは現在、先進的安全技術、自動シャットダウン機能、リアルタイムモニタリング機能を備え、厳しい規制基準への準拠を保証しています。特に医薬品、農薬、特殊化学品などの産業における化学製品の需要拡大も、このセグメントの拡大に寄与しています。このことは、化学産業における効率的でエコフレンドリー加熱ソリューションへの依存度が高まっていることを示しています。

米国では、非凝縮式低温産業用ボイラー市場は2034年までに4億5,000万米ドルを創出すると予測されています。信頼性が高く費用対効果の高い暖房システムに対する需要の高まりが、進行中の産業拡大と相まって、市場展望を後押ししています。米国環境保護庁(EPA)や州レベルの当局が定める厳しい排出規制は、熱伝達効率を向上させ排出を削減する、より先進的システムの採用を産業に促しています。さらに、従来の暖房システムの近代化と、低メンテナンスで長持ちするソリューションの重視が相まって、米国の市場成長はさらに強まると予想されます。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 市場推定・予測パラメータ

- 予測計算

- データソース

- 一次データ

- 二次データ

- 有料

- 公的

第2章 エグゼクティブサマリー

第3章 産業洞察

- エコシステム分析

- 規制状況

- 産業への影響要因

- 促進要因

- 産業の潜在的リスク・課題

- 成長ポテンシャル分析

- ポーター分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的展望

- イノベーションと持続可能性の展望

第5章 市場規模・予測:温度別、2021~2034年

- 主要動向

- 120°F以下

- 120~140°F

- 140~160°F

- 160~180°F

第6章 市場規模・予測:製品別、2021~2034年

- 主要動向

- 火管

- 水管

第7章 市場規模・予測:容量別、2021~2034年

- 主要動向

- 10MMBTU/時以下

- 10~25MMBTU/時

- 25~50MMBTU/時

- 50~75MMBTU/時

- 75~100MMBTU/時

- 100~175MMBTU/時

- 175~250MMBTU/時

- 250MMBTU/時以上

第8章 市場規模・予測:燃料別、2021~2034年

- 主要動向

- 天然ガス

- 石油

- 石炭

- その他

第9章 市場規模・予測:用途別、2021~2034年

- 主要動向

- 食品加工

- パルプ・製紙

- 化学

- 精製

- 一次金属

- その他

第10章 市場規模・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- フランス

- 英国

- ポーランド

- イタリア

- スペイン

- オーストリア

- ドイツ

- スウェーデン

- ロシア

- アジア太平洋

- 中国

- インド

- フィリピン

- 日本

- 韓国

- オーストラリア

- インドネシア

- 中東・アフリカ

- サウジアラビア

- イラン

- アラブ首長国連邦

- ナイジェリア

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

- チリ

第11章 企業プロファイル

- Babcock Wanson

- Bosch Industriekessel

- Cleaver-Brooks

- Cochran

- Ferroli

- Fulton

- Hurst Boiler & Welding

- IHI

- Maxima Boilers

- Miura America

- Parker Boiler

- Precision Boilers

- Thermax

- Vaillant

- Viessmann

The Global Non-Condensing Low Temperature Industrial Boiler Market was valued at USD 2.1 billion in 2024 and is expected to grow at a CAGR of 4.4% from 2025 to 2034. This growth is being driven by the modernization of outdated industrial systems and strategic upgrades to boiler infrastructure. Investments in energy-efficient technologies, along with the integration of durable and corrosion-resistant components, are contributing to an optimistic outlook for the industry.

The segment for temperatures ranging from >140°F to 160°F is projected to generate USD 1 billion in revenue by 2034. The segment growth is driven by its use in sectors that require precise temperature control, such as refineries, food processing, and chemical manufacturing. Non-condensing boilers in this range are engineered to deliver optimal operational efficiency and consistent performance under demanding conditions. Manufacturers are increasingly focusing on enhancing durability by utilizing advanced materials and innovative designs to extend the lifespan of their products. The integration of Internet of Things (IoT)-enabled remote monitoring and predictive maintenance systems is further expected to reduce downtime, optimize operations, and increase the adoption of these systems across industries.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.1 Billion |

| Forecast Value | $3.2 Billion |

| CAGR | 4.4% |

The chemical sector is poised to grow at a rate of 3.5% through 2034. This growth is fueled by the increasing implementation of strict environmental regulations aimed at reducing emissions and improving energy management. Modern industrial boilers now come equipped with advanced safety technologies, automated shutdown functions, and real-time monitoring capabilities to ensure compliance with stringent regulatory standards. The growing demand for chemical products, particularly in industries such as pharmaceuticals, agrochemicals, and specialty chemicals, is also contributing to the sector's expansion. This demonstrates the rising dependence on efficient and environmentally friendly heating solutions within the chemical industry.

In the United States, the non-condensing low-temperature industrial boiler market is projected to generate USD 450 million by 2034. The growing demand for reliable, cost-effective heating systems, coupled with ongoing industrial expansion, is boosting market prospects. The stringent emission regulations set by the U.S. Environmental Protection Agency (EPA) and state-level authorities are driving industries to adopt more advanced systems that improve heat transfer efficiency and reduce emissions. Additionally, the modernization of legacy heating systems, combined with a greater focus on low-maintenance, long-lasting solutions, is expected to further strengthen market growth in the U.S.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Temperature, 2021 – 2034 (Units, MMBTU/hr & USD Million)

- 5.1 Key trends

- 5.2 ≤ 120°F

- 5.3 > 120°F - 140°F

- 5.4 > 140°F - 160°F

- 5.5 > 160°F - 180°F

Chapter 6 Market Size and Forecast, By Product, 2021 – 2034 (Units, MMBTU/hr & USD Million)

- 6.1 Key trends

- 6.2 Fire-tube

- 6.3 Water-tube

Chapter 7 Market Size and Forecast, By Capacity, 2021 – 2034 (Units, MMBTU/hr & USD Million)

- 7.1 Key trends

- 7.2 < 10 MMBTU/hr

- 7.3 10 - 25 MMBTU/hr

- 7.4 25 - 50 MMBTU/hr

- 7.5 50 - 75 MMBTU/hr

- 7.6 75 - 100 MMBTU/hr

- 7.7 100 - 175 MMBTU/hr

- 7.8 175 - 250 MMBTU/hr

- 7.9 > 250 MMBTU/hr

Chapter 8 Market Size and Forecast, By Fuel, 2021 – 2034 (Units, MMBTU/hr & USD Million)

- 8.1 Key trends

- 8.2 Natural gas

- 8.3 Oil

- 8.4 Coal

- 8.5 Others

Chapter 9 Market Size and Forecast, By Application, 2021 – 2034 (Units, MMBTU/hr & USD Million)

- 9.1 Key trends

- 9.2 Food processing

- 9.3 Pulp & paper

- 9.4 Chemical

- 9.5 Refinery

- 9.6 Primary metal

- 9.7 Others

Chapter 10 Market Size and Forecast, By Region, 2021 – 2034 (Units, MMBTU/hr & USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 France

- 10.3.2 UK

- 10.3.3 Poland

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Austria

- 10.3.7 Germany

- 10.3.8 Sweden

- 10.3.9 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Philippines

- 10.4.4 Japan

- 10.4.5 South Korea

- 10.4.6 Australia

- 10.4.7 Indonesia

- 10.5 Middle East & Africa

- 10.5.1 Saudi Arabia

- 10.5.2 Iran

- 10.5.3 UAE

- 10.5.4 Nigeria

- 10.5.5 South Africa

- 10.6 Latin America

- 10.6.1 Brazil

- 10.6.2 Argentina

- 10.6.3 Chile

Chapter 11 Company Profiles

- 11.1 Babcock Wanson

- 11.2 Bosch Industriekessel

- 11.3 Cleaver-Brooks

- 11.4 Cochran

- 11.5 Ferroli

- 11.6 Fulton

- 11.7 Hurst Boiler & Welding

- 11.8 IHI

- 11.9 Maxima Boilers

- 11.10 Miura America

- 11.11 Parker Boiler

- 11.12 Precision Boilers

- 11.13 Thermax

- 11.14 Vaillant

- 11.15 Viessmann