|

市場調査レポート

商品コード

1665297

神経痛治療市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Neuralgia Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 神経痛治療市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2024年12月19日

発行: Global Market Insights Inc.

ページ情報: 英文 135 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

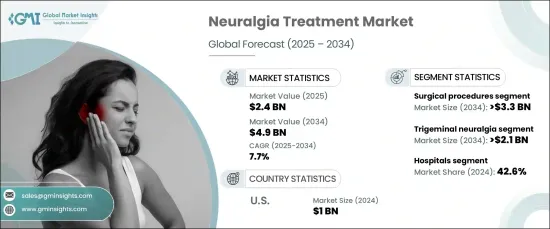

世界の神経痛治療市場は、2024年に24億米ドルと評価され、2025~2034年のCAGRは7.7%と予測され、大幅な成長を遂げる見込みです。

この成長は主に、神経疾患の有病率の増加と、認知、診断、治療オプションの進歩によってもたらされます。

神経疾患、特に様々な形態の神経痛の罹患率の上昇は、市場拡大を後押しする重要な要因です。これらの疾患を取り巻く認識が高まるにつれ、早期診断と治療を求める人が増えています。国民の意識向上キャンペーンや診断能力の向上は、神経痛の早期発見に重要な役割を果たしており、三叉神経痛、帯状疱疹後神経痛、その他の神経関連疼痛のような疾患を対象とする治療法に対する需要を促進しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 24億米ドル |

| 予測金額 | 49億米ドル |

| CAGR | 7.7% |

市場は、三叉神経痛、帯状疱疹後神経痛、後頭神経痛など、さまざまな神経痛の症状別に区分されます。中でも三叉神経痛が最も高い成長が見込まれ、CAGRは7.9%と予測され、2034年には21億米ドルに達します。三叉神経痛は、最も一般的な神経痛の一つであり、特に高齢者層に影響を及ぼし、日常生活や生活の質全体に深刻な影響を与える可能性があります。このため、より良い治療オプションに対する需要が高まり、市場の成長をさらに後押ししています。

エンドユーザーの観点からは、病院が神経痛治療市場の大幅な成長を牽引すると予測されています。MRIやCTスキャンのような先進的診断ツールがあるため、病院は総合的な診断と治療の場として依然として好まれています。これらの最先端技術により、医療プロバイダーはさまざまなタイプの神経痛を正確に特定することができ、患者が最も効果的で的を絞った治療を受けられるようになります。正確な診断能力を提供できる病院は、複雑な神経疾患の治療において最も信頼され信頼できる環境であり、市場における優位性を確保しています。

米国では、神経痛治療市場は予測期間中に力強い成長が見込まれます。最先端の画像技術、手術手技、薬理学的革新を特徴とする同国の高度医療インフラが、引き続き市場の主導権を支えています。三叉神経痛や帯状疱疹後神経痛のような症状に特に罹りやすい高齢化社会では、効果的な治療に対する需要が高まっています。さらに、好意的な償還施策や大手製薬企業による研究開発への多額の投資が市場開拓に貢献しており、米国が世界の神経痛治療において重要な地位を占めています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 産業洞察

- エコシステム分析

- 産業への影響要因

- 促進要因

- 神経疾患の有病率の上昇

- 疼痛管理技術の進歩

- 認知度と診断率の向上

- 産業の潜在的リスク・課題

- 先進治療の高コスト

- 促進要因

- 成長可能性分析

- 規制状況

- 技術

- 償還シナリオ

- ギャップ分析

- ポーター分析

- PESTEL分析

- 今後の市場動向

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業シェア分析

- 主要市場企業の競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推定・予測:治療タイプ別、2021~2034年

- 主要動向

- 外科手術

- 高周波熱病変治療

- 定位放射線手術

- 微小血管減圧術

- その他の外科手術

- 薬剤療法

- 抗けいれん薬

- 抗うつ薬

- その他の薬剤

第6章 市場推定・予測:用途別、2021~2034年

- 主要動向

- 三叉神経痛

- 帯状疱疹後神経痛

- 後頭神経痛

- その他

第7章 市場推定・予測:最終用途別、2021~2034年

- 主要動向

- 病院

- クリニック

- 外来手術センター

- その他

第8章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- AA pharma

- astellas

- Biogen

- Eli Lilly

- Johnson & Johnson

- Medtronic

- NOVARTIS

- PACIRA BIOSCIENCES

- Pfizer

- Siemens Healthineers

The Global Neuralgia Treatment Market, valued at USD 2.4 billion in 2024, is set to experience substantial growth, with a projected CAGR of 7.7% from 2025 to 2034. This growth is primarily driven by the increasing prevalence of neurological disorders and advancements in awareness, diagnosis, and treatment options.

The rising incidence of neurological conditions, particularly various forms of neuralgia, is a key factor fueling market expansion. As awareness surrounding these disorders grows, more individuals are seeking early diagnosis and treatment. Public awareness campaigns and improved diagnostic capabilities have played a significant role in detecting neuralgia at earlier stages, driving demand for therapies that target conditions like trigeminal neuralgia, postherpetic neuralgia, and other forms of nerve-related pain.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.4 Billion |

| Forecast Value | $4.9 Billion |

| CAGR | 7.7% |

The market is segmented by various neuralgia conditions, including trigeminal neuralgia, postherpetic neuralgia, occipital neuralgia, and others. Among these, trigeminal neuralgia is expected to see the highest growth, with a projected CAGR of 7.9%, reaching USD 2.1 billion by 2034. Trigeminal neuralgia, one of the most common types of neuralgia, especially affects older populations and can severely impact daily activities and overall quality of life. This has led to increased demand for better treatment options, further propelling market growth.

From the perspective of end-users, hospitals are projected to drive substantial growth in the neuralgia treatment market. With advanced diagnostic tools like MRI and CT scans, hospitals remain the preferred setting for comprehensive diagnosis and treatment. These cutting-edge technologies enable healthcare providers to accurately identify different types of neuralgia, ensuring that patients receive the most effective and targeted treatments. The ability to offer precise diagnostic capabilities makes hospitals the most trusted and reliable environments for treating complex neurological conditions, thus securing their dominance in the market.

In the U.S., the neuralgia treatment market is expected to see robust growth during the forecast period. The country's advanced healthcare infrastructure, featuring state-of-the-art imaging technologies, surgical techniques, and pharmacological innovations, continues to support its market leadership. With an aging population that is particularly vulnerable to conditions like trigeminal and postherpetic neuralgia, the demand for effective treatments is escalating. Furthermore, favorable reimbursement policies and significant investments in research and development by major pharmaceutical companies are contributing to the market's expansion, ensuring that the U.S. remains a key player in the global neuralgia treatment landscape.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of neurological disorders

- 3.2.1.2 Advancements in pain management technologies

- 3.2.1.3 Increase in awareness and diagnosis rates

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced therapies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Reimbursement scenario

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Future market trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Treatment Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Surgical procedures

- 5.2.1 Radiofrequency thermal lesioning

- 5.2.2 Stereotactic radiosurgery

- 5.2.3 Microvascular decompression

- 5.2.4 Other surgical procedures

- 5.3 Medications

- 5.3.1 Anticonvulsants

- 5.3.2 Antidepressants

- 5.3.3 Other medications

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Trigeminal neuralgia

- 6.3 Postherpetic neuralgia

- 6.4 Occipital neuralgia

- 6.5 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Clinics

- 7.4 Ambulatory surgical centers

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AA pharma

- 9.2 astellas

- 9.3 Biogen

- 9.4 Eli Lilly

- 9.5 Johnson & Johnson

- 9.6 Medtronic

- 9.7 NOVARTIS

- 9.8 PACIRA BIOSCIENCES

- 9.9 Pfizer

- 9.10 Siemens Healthineers