ペッサリー市場の市場機会、成長促進要因、産業動向分析、2025~2034年予測

Pessary Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 1665292

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

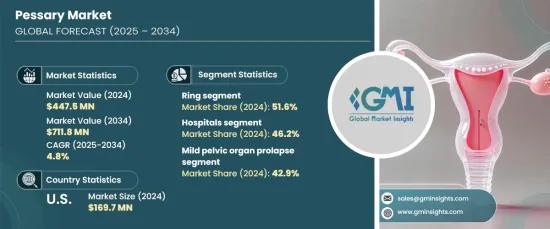

ペッサリーの世界市場は、2024年に4億4,750万米ドルと評価され、2025~2034年にかけてCAGR 4.8%で安定した成長を遂げると予測されています。

この成長は主に、骨盤臓器脱(POP)と尿失禁の有病率の増加、タイムリーな診断と治療の重要性に対する意識の高まり、非侵襲的な治療オプションへの嗜好の高まり、女性の健康プログラムを支援する政府のイニシアチブの強化によってもたらされます。

市場はタイプ別に区分され、リングペッサリーが2024年の市場シェアの51.6%を占めてリードしています。リングペッサリーが優位を維持している理由は、汎用性、使いやすさ、軽量の快適性にあり、軽度から中等度の脱肛やストレス性尿失禁に悩む人に最適です。そのデザインは刺激を軽減し、長時間の使用を可能にするため、臨床現場で好まれ、広く受け入れられる要因となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034 |

| 開始金額 | 4億4,750万米ドル |

| 予測金額 | 7億1,180万米ドル |

| CAGR | 4.8% |

エンドユーザー別では、病院が主要セグメントとして浮上し、2024年の市場シェアの46.2%を獲得しました。病院は、POPやストレス性尿失禁などの骨盤底障害の診断、管理、治療において極めて重要な役割を果たしています。これらの医療機関は、外科的と非外科的ペッサリー治療の両方を提供し、さまざまな重症度の患者に対応しています。複雑な症例に対応し、必要不可欠なフォローアップケアを提供する能力は、ペッサリー市場における優位性をさらに強めています。

米国では、ペッサリー市場は2024年に1億6,970万米ドルと評価され、引き続き力強い成長の可能性を示しています。肥満のような生活習慣に関連した健康状態とともに、骨盤障害の増加が、効果的で非侵襲的な治療ソリューションとしてのペッサリー需要の増加を促しています。医療へのアクセスが拡大し、骨盤の健康問題に対する意識を高める努力が続けられていることが、国内全域で市場の継続的成長に寄与しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 産業洞察

- エコシステム分析

- 産業への影響要因

- 促進要因

- 骨盤臓器脱と尿失禁の有病率の増加

- タイムリーな診断と治療に対する意識の高まり

- 非侵襲的治療オプションの採用増加

- 女性の健康プログラムにおける政府支援の増加

- 産業の潜在的リスク・課題

- 社会的スティグマと心理的障壁

- 長期使用による感染リスクに関する懸念

- 促進要因

- 成長可能性分析

- 特許分析

- ギャップ分析

- 規制状況

- 技術的展望

- 今後の市場動向

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 主要市場参入企業の競合分析

- 競合のポジショニングマトリックス

- 戦略展望

第5章 市場推定・予測:タイプ別、2021~2034年

- 主要動向

- リング

- ドーナツ

- ゲルホーン

- その他

第6章 市場推定・予測:用途別、2021~2034年

- 主要動向

- 軽度の骨盤臓器脱

- ストレス性尿失禁

- 重度の骨盤臓器脱

- その他

第7章 市場推定・予測:最終用途別、2021~2034年

- 主要動向

- 病院

- 外来手術センター

- クリニック

- その他

第8章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Artisan Medical

- BIoTeque America

- Bliss GVS Pharma

- Bray Group(Ethos Partners)

- Coloplast Group

- Contiform International

- CooperSurgical

- Dr. Arabin

- Integra Lifesciences

- MedGyn Products

- Novomed group(Gyneas)

- Panpac Medical

- Personal Medical

- Smiths Group

- Sugar International

目次

The Global Pessary Market was valued at USD 447.5 million in 2024 and is projected to experience steady growth at a CAGR of 4.8% from 2025 to 2034. This growth is primarily driven by the increasing prevalence of pelvic organ prolapse (POP) and urinary incontinence, heightened awareness about the importance of timely diagnosis and treatment, growing preference for non-invasive therapy options, and strengthened government initiatives supporting women's health programs.

The market is segmented by type, with the ring pessary leading the way, accounting for 51.6% of the market share in 2024. The ring pessary's continued dominance can be attributed to its versatility, ease of use, and lightweight comfort, making it ideal for individuals suffering from mild to moderate prolapse and stress urinary incontinence. Its design reduces irritation and allows for prolonged use, making it a favored choice in clinical settings and contributing to its widespread acceptance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $447.5 Million |

| Forecast Value | $711.8 Million |

| CAGR | 4.8% |

By end user, hospitals emerged as the leading segment, capturing 46.2% of the market share in 2024. Hospitals play a pivotal role in diagnosing, managing, and treating pelvic floor disorders such as POP and stress urinary incontinence. These institutions offer both surgical and non-surgical pessary treatments, catering to patients with varying levels of severity. Their ability to handle complex cases and provide essential follow-up care further reinforces their dominance in the pessary market.

In the United States, the pessary market was valued at USD 169.7 million in 2024 and continues to show strong growth potential. The rise in pelvic disorders, alongside lifestyle-related health conditions like obesity, is driving the increasing demand for pessaries as effective, non-invasive treatment solutions. The expansion of healthcare access and ongoing efforts to raise awareness about pelvic health issues are contributing to the continued market growth across the country.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of pelvic organ prolapse and urinary incontinence

- 3.2.1.2 Growing awareness towards timely diagnosis and treatment

- 3.2.1.3 Increasing adoption of non-invasive treatment options

- 3.2.1.4 Growing government support in women health programs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Social stigma and psychological barrier

- 3.2.2.2 Concerns related to risk of infections due to prolonged use

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Patent analysis

- 3.5 Gap analysis

- 3.6 Regulatory landscape

- 3.7 Technological landscape

- 3.8 Future market trends

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy outlook

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Ring

- 5.3 Donut

- 5.4 Gellhorn

- 5.5 Other types

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Mild pelvic organ prolapse

- 6.3 Stress urinary incontinence

- 6.4 Severe pelvic organ prolapse

- 6.5 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Clinics

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Artisan Medical

- 9.2 Bioteque America

- 9.3 Bliss GVS Pharma

- 9.4 Bray Group (Ethos Partners)

- 9.5 Coloplast Group

- 9.6 Contiform International

- 9.7 CooperSurgical

- 9.8 Dr. Arabin

- 9.9 Integra Lifesciences

- 9.10 MedGyn Products

- 9.11 Novomed group (Gyneas)

- 9.12 Panpac Medical

- 9.13 Personal Medical

- 9.14 Smiths Group

- 9.15 Sugar International

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日