|

市場調査レポート

商品コード

1665240

単極電気手術器具の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Monopolar Electrosurgery Instrument Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 単極電気手術器具の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2024年12月17日

発行: Global Market Insights Inc.

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

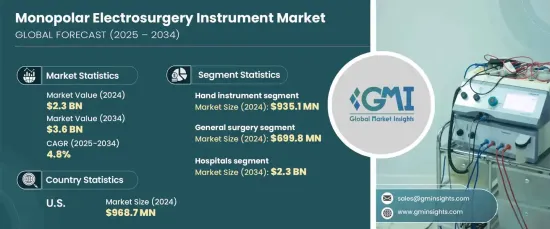

世界の単極電気手術器具市場は、2024年に23億米ドルに達し、2025~2034年のCAGRは4.8%と予測され、力強い成長が見込まれています。

この成長の原動力は、低侵襲手術に対する需要の高まり、慢性疾患の有病率の上昇、世界の医療投資の拡大です。さらに、技術の進歩と精密な手術器具に対するニーズの高まりが、市場の上昇軌道に拍車をかけています。

低侵襲手術は、一般手術、婦人科、泌尿器科、消化器科など、さまざまな医療専門セグメントで標準的な手法となっています。単極電気手術器具は、その精度、効率、手術手術中の組織損傷を最小限に抑える能力により、これらのセグメントで重要な役割を果たしています。組織の切断、凝固、乾燥において汎用性があるため、日常的な手術にも複雑な手術にも不可欠です。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034 |

| 開始金額 | 23億米ドル |

| 予測金額 | 36億米ドル |

| CAGR | 4.8% |

市場は、手用器具、電気手術用ジェネレーター、分散電極、付属品を含む製品タイプに区分されます。手用器具セグメントは、2024年の売上高が9億3,510万米ドルで市場をリードしています。これらの器具は、多くの手術セグメントで広く使用されており、繊細な手技に必要な精度とコントロールを提供しています。開腹手術と低侵襲手術の両方に適応できるため、幅広い医療ニーズに対応し、依然として支配的なセグメントです。

用途別では、一般手術、心臓血管手術、婦人科、神経手術、その他に分けられます。一般手術は2024年に6億9,980万米ドルを占め、予測期間中にCAGR 4.6%で成長すると予測されています。単極電気手術器具は、軟部組織の管理、止血、手術時間の短縮において効率的であるため、このセグメントで高く評価されています。手術結果を向上させ、患者の回復を早めるその能力は、病院や手術センター全体の需要を牽引し続けています。

米国の単極電気手術器具市場は、2024年に9億6,870万米ドルを生み出しました。この市場は2034年までCAGR 4.2%で成長すると予想され、大手メーカーの存在と確立された医療インフラに支えられています。慢性疾患の有病率の増加や低侵襲手術の採用の増加が、これらの器具に対する需要の持続に寄与しています。さらに、先進的医療訓練と専門知識の利用が可能であることが、単極電気手術器具の採用をさらに加速させ、米国が世界市場における主導的地位を強化しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 産業洞察

- エコシステム分析

- 産業への影響要因

- 促進要因

- 低侵襲手術に対する需要の高まり

- 電気手術技術の進歩

- 慢性疾患の有病率の増加

- 世界の医療支出の増加

- 産業の潜在的リスク・課題

- 熱損傷の高いリスク

- 促進要因

- 成長可能性分析

- 規制状況

- 償還シナリオ

- 技術

- 今後の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業シェア分析

- 主要市場参入企業の競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推定・予測:製品タイプ別、2021~2034年

- 主要動向

- 手用器具

- 電気手術用ジェネレーター

- 分散電極

- 付属品

第6章 市場推定・予測:用途別、2021~2034年

- 主要動向

- 一般手術

- 心臓血管手術

- 婦人科手術

- 脳神経手術

- その他

第7章 市場推定・予測:最終用途別、2021~2034年

- 主要動向

- 病院

- 外来手術センター

- その他

第8章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Apyx Medical

- B.Braun

- BOWA MEDICAL

- CONMED

- Encision

- Erbe Elektromedizin

- Johnson & Johnson

- KLS Martin Group

- Medtronic

- Meyer-Haake

- Olympus

- Stryker

The Global Monopolar Electrosurgery Instrument Market reached USD 2.3 billion in 2024 and is expected to experience strong growth, with a projected CAGR of 4.8% from 2025 to 2034. This growth is driven by the increasing demand for minimally invasive procedures, the rising prevalence of chronic diseases, and expanding healthcare investments around the world. Additionally, technological advancements and the growing need for precise surgical instruments are fueling the market's upward trajectory.

Minimally invasive procedures have become standard practice across various medical specialties such as general surgery, gynecology, urology, and gastroenterology. Monopolar electrosurgery instruments play a crucial role in these fields due to their precision, efficiency, and ability to minimize tissue damage during surgical procedures. Their versatility in cutting, coagulating, and desiccating tissues makes them indispensable for both routine and complex surgeries.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.3 Billion |

| Forecast Value | $3.6 Billion |

| CAGR | 4.8% |

The market is segmented into product types, including hand instruments, electrosurgical generators, dispersive electrodes, and accessories. The hand instrument segment led the market with a revenue of USD 935.1 million in 2024. These instruments are widely used across numerous surgical disciplines, offering the precision and control required for delicate procedures. Their adaptability to both open and minimally invasive surgeries ensures they remain the dominant segment, addressing a wide array of medical needs.

In terms of application, the market is divided into general surgery, cardiovascular surgery, gynecology, neurosurgery, and others. General surgery accounted for USD 699.8 million in 2024 and is projected to grow at a CAGR of 4.6% during the forecast period. Monopolar electrosurgery instruments are highly regarded in this segment for their efficiency in managing soft tissues, providing hemostasis, and reducing surgical time. Their ability to enhance surgical outcomes and promote faster patient recovery continues to drive demand across hospitals and surgical centers.

The U.S. monopolar electrosurgery instrument market generated USD 968.7 million in 2024. This market is expected to grow at a CAGR of 4.2% through 2034, supported by the presence of leading manufacturers and a well-established healthcare infrastructure. The growing prevalence of chronic conditions and the increasing adoption of minimally invasive procedures contribute to sustained demand for these instruments. Additionally, the availability of advanced medical training and expertise further accelerates the adoption of monopolar electrosurgery instruments, reinforcing the U.S.'s leadership position in the global market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for minimally invasive procedures

- 3.2.1.2 Advancements in electrosurgical technologies

- 3.2.1.3 Growing prevalence of chronic diseases

- 3.2.1.4 Rising global healthcare expenditure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High risk of thermal injuries

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Reimbursement scenario

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Hand instrument

- 5.3 Electrosurgical generators

- 5.4 Dispersive electrodes

- 5.5 Accessories

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 General surgery

- 6.3 Cardiovascular surgery

- 6.4 Gynecology surgery

- 6.5 Neurosurgery

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Apyx Medical

- 9.2 B.Braun

- 9.3 BOWA MEDICAL

- 9.4 CONMED

- 9.5 Encision

- 9.6 Erbe Elektromedizin

- 9.7 Johnson & Johnson

- 9.8 KLS Martin Group

- 9.9 Medtronic

- 9.10 Meyer-Haake

- 9.11 Olympus

- 9.12 Stryker