|

市場調査レポート

商品コード

1665225

セメントレス人工膝関節システムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Cementless Total Knee Systems (TKS) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| セメントレス人工膝関節システムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2024年12月17日

発行: Global Market Insights Inc.

ページ情報: 英文 140 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

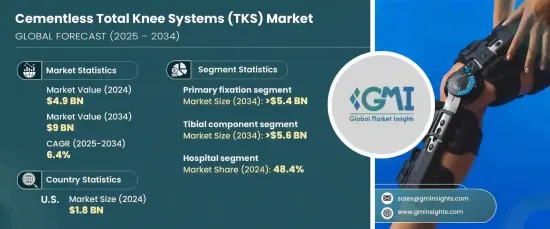

セメントレス人工膝関節システムの世界市場規模は、2024年に49億米ドルとなり、2025~2034年にかけてCAGR 6.4%で力強い成長を遂げると予測されています。

この成長には、世界の高齢化とともに変形性関節症や関節リウマチの有病率が上昇していることが背景にあります。セメントレス人工膝関節システムは、従来のセメントインプラントに比べて耐久性に優れ、回復が早く、合併症のリスクが少ないため、ますます支持されるようになっています。

特に高齢者における変形性人工膝関節症の罹患率の増加が、人工膝関節全置換術の需要を牽引し続けています。世界人口の高齢化に伴い、セメントレスシステムのような先進的で低侵襲なソリューションに対するニーズが高まっています。これらのインプラントは、骨結合の促進、長期安定性の向上、術後リスクの最小化といった利点があり、外科医と患者の双方にとって好ましい選択肢となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034 |

| 開始金額 | 49億米ドル |

| 予測金額 | 90億米ドル |

| CAGR | 6.4% |

市場は固定方法別に一次固定とハイブリッド固定に区分されます。なかでも一次固定は、骨セメントを使用せずに初期安定性を高め、オッセオインテグレーションを改善できることから、このセグメントをリードしています。このアプローチでは、インプラントと骨が直接結合するため、治癒が早まり、長期的な耐久性が確保されます。手術器具や手技における技術革新が、一次固定システムの採用をさらに後押ししています。

コンポーネントに関しては、市場は脛骨コンポーネントと大腿骨コンポーネントに分類されます。脛骨コンポーネントが大きな市場シェアを占めており、予測期間中は安定した成長が見込まれます。脛骨コンポーネントは、体重を支え関節の安定性を維持するという重要な役割を担っているため、人工膝関節システムには欠かせない要素となっています。最近のモジュール型設計の進歩により、脛骨コンポーネントの性能が向上し、インプラントのゆるみが減少し、患者の転帰が改善されています。

米国のセメントレス人工膝関節全置換システム市場は、2024年に18億米ドルを生み出しました。この成長の原動力となっているのは、人口の高齢化、人工膝関節置換術の増加、医療インフラの進歩です。より良い手術結果の達成と回復時間の短縮に重点を置くことで、セメントレスシステムの採用が国全体で促進され続けています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 産業洞察

- エコシステム分析

- 産業への影響要因

- 促進要因

- 世界の変形性関節症と関節リウマチの有病率の上昇

- 低侵襲手術手技の採用増加

- セメントレス固定法の技術的進歩

- 関節障害を起こしやすい高齢者の増加

- 産業の潜在的リスク・課題

- セメントレス膝システムの高コスト

- 促進要因

- 成長可能性分析

- 規制状況

- 償還シナリオ

- 技術

- ギャップ分析

- ポーター分析

- PESTEL分析

- 今後の市場動向

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業シェア分析

- 主要市場参入企業の競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推定・予測:固定方法別、2021~2034年

- 主要動向

- 一次固定

- ハイブリッド固定

第6章 市場推定・予測:コンポーネント別、2021~2034年

- 主要動向

- 脛骨コンポーネント

- 大腿骨コンポーネント

第7章 市場推定・予測:最終用途別、2021~2034年

- 主要動向

- 病院

- 整形外科センター

- その他

第8章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Aesculap

- Conformis

- Corin Group

- Dentsply Sirona

- DePuy Synthes

- Enovis

- Episurf Medical

- Exactech

- Medacta International

- MicroPort Orthopedics

- Smith &Nephew

- Stryker

- United Orthopedic

- Waldemar Link

- Zimmer Biomet

The Global Cementless Total Knee Systems Market was valued at USD 4.9 billion in 2024 and is projected to experience robust growth at a CAGR of 6.4% from 2025 to 2034. This growth is fueled by the rising prevalence of osteoarthritis and rheumatoid arthritis alongside an aging population worldwide. Cementless knee systems are increasingly favored due to their exceptional durability, faster recovery times, and reduced risk of complications compared to traditional cemented implants.

The growing incidence of osteoarthritis, particularly among older adults, continues to drive the demand for total knee replacements. As the global population ages, there is an escalating need for advanced and minimally invasive solutions such as cementless systems. These implants offer the advantage of promoting faster bone integration, enhancing long-term stability, and minimizing post-operative risks, making them the preferred choice for both surgeons and patients.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.9 Billion |

| Forecast Value | $9 Billion |

| CAGR | 6.4% |

The market is segmented by fixation type into primary fixation and hybrid fixation. Among these, primary fixation leads the segment due to its ability to provide enhanced initial stability and improved osseointegration without the need for bone cement. This approach allows the implant to bond directly with the bone, fostering faster healing and ensuring long-term durability. Technological innovations in surgical tools and techniques have further boosted the adoption of primary fixation systems.

In terms of components, the market is categorized into tibial and femoral components. The tibial component holds a significant market share and is expected to witness steady growth over the forecast period. Its vital role in supporting body weight and maintaining joint stability makes it an essential element in knee replacement systems. Recent advancements in modular designs have enhanced the performance of tibial components, reducing implant loosening and improving patient outcomes.

The U.S. cementless total knee systems market generated USD 1.8 billion in 2024. This growth is driven by a large aging population, an increasing number of knee replacement surgeries, and advancements in healthcare infrastructure. The focus on achieving better surgical outcomes and reducing recovery times continues to fuel the adoption of cementless systems across the country.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of osteoarthritis and rheumatoid arthritis globally

- 3.2.1.2 Increasing adoption of minimally invasive surgical techniques

- 3.2.1.3 Technological advancements in cementless fixation methods

- 3.2.1.4 Growing geriatric population prone to joint disorders

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with cementless knee systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Reimbursement scenario

- 3.6 Technology landscape

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Future market trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Fixation Method, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Primary fixation

- 5.3 Hybrid fixation

Chapter 6 Market Estimates and Forecast, By Component, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Tibial component

- 6.3 Femoral component

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Orthopedic centers

- 7.4 Other End Use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Aesculap

- 9.2 Conformis

- 9.3 Corin Group

- 9.4 Dentsply Sirona

- 9.5 DePuy Synthes

- 9.6 Enovis

- 9.7 Episurf Medical

- 9.8 Exactech

- 9.9 Medacta International

- 9.10 MicroPort Orthopedics

- 9.11 Smith & Nephew

- 9.12 Stryker

- 9.13 United Orthopedic

- 9.14 Waldemar Link

- 9.15 Zimmer Biomet