軌道上衛星サービス市場の市場機会、成長促進要因、産業動向分析、2025~2034年予測

On-orbit Satellite Servicing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1665218

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

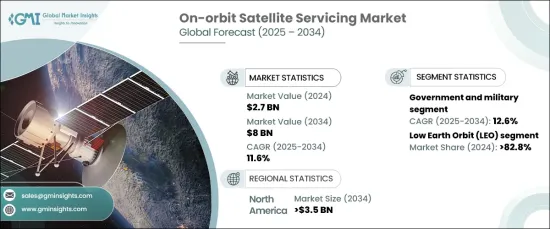

軌道上衛星サービスの世界市場は大幅な成長を遂げ、2024年には27億米ドルに達し、2025~2034年のCAGRは11.6%という驚異的な予測が示されています。

この急拡大の背景には、運用寿命の延長、打ち上げコストの削減、性能の向上を目的とした衛星の保守、修理、アップグレードに対する需要の増加があります。通信、地球観測、防衛などの主要用途への衛星配備の増加は、市場の成長軌道をさらに加速させています。

軌道タイプ別に市場を分析すると、低軌道(LEO)がリードしており、2024年の市場シェアの82.8%を占めています。LEOの優位性は、特に世界のブロードバンド放送とリモートセンシングに焦点を当てた衛星コンステレーションの爆発的増加に起因しています。この軌道に衛星が密集しているため、ロボットによる燃料補給、修理、デブリ除去などの革新的なソリューションが必要となります。さらに、LEOは地球に近いため、頻繁で費用対効果の高いサービスミッションを実施しやすく、衛星運用の持続可能性と効率性が確保されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034 |

| 開始金額 | 27億米ドル |

| 予測金額 | 80億米ドル |

| CAGR | 11.6% |

エンドユーザー別に見ると、軌道上衛星サービス市場は政府・軍事機関と商業事業者に区分されます。2025~2034年の予測CAGRは12.6%で、政府・軍需セグメントが最も急成長が見込まれています。政府が重要な宇宙資産の機能を維持し、国家安全保障を強化し、交換コストを削減しようとしているため、衛星インフラへの投資が増加しており、この需要に拍車をかけています。さらに、官民の協力が技術進歩を促進し、このセグメントの成長を加速する上で重要な役割を果たしています。

北米は世界の軌道上衛星サービス市場を独占することになり、2034年までに35億米ドルに達する見込みです。この地域の強い地位は、宇宙技術への多額の投資と、この産業の主要参入企業の確立された存在感から生じています。技術革新を支援する政府プログラムは、衛星通信と防衛ソリューションの需要増加と相まって、このセグメントにおける北米のリーダーシップを確固たるものにしています。さらに、この地域のサステイナブル宇宙開発への取り組みと軌道上サービス技術の躍進が、市場での地位をさらに高めています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 1次データ

- 二次資料

- 有料情報源

- 公的情報源

第2章 エグゼクティブサマリー

第3章 産業洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 変革

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 促進要因

- 衛星コンステレーションと宇宙トラフィックの急増

- 衛星のライフサイクル延長によるコスト削減

- 宇宙ロボット工学と自動化におけるブレークスルー

- 政府と民間企業の投資拡大

- スペースデブリ管理への注目の高まり

- 産業の潜在的リスク・課題

- 高い開発・運用コスト

- 技術的複雑性と運用リスク

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推定・予測:サービス別、2021~2034年

- 主要動向

- アクティブ・デブリ除去(ADR)と軌道調整

- ロボットサービス

- 燃料補給

- 組立

第6章 市場推定・予測:軌道タイプ別、2021~2034年

- 主要動向

- 地球低軌道(LEO)

- 中軌道(MEO)

- 静止軌道(GEO)

第7章 市場推定・予測:衛星タイプ別、2021~2034年

- 主要動向

- 小型衛星(500Kg以下)

- 中型衛星(501~1,000Kg)

- 大型衛星(1,000Kg以上)

第8章 市場推定・予測:最終用途別、2021~2034年

- 主要動向

- 政府・軍事機関

- 民間事業者

第9章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Airbus SE

- Altius Space Machines, Inc.

- Astroscale Holdings Inc.

- Atomos Space

- ClearSpace

- Future Space Industries

- High Earth Orbit Robotics

- Hyoristic Innovations

- Infinite Orbits

- Lunasa Ltd.

- Maxar Technologies

- Momentus, Inc.

- Nanoracks(Voyager Space)

- Obruta Space Solutions Corp

- Orbit Fab, Inc.

- Orbitaid Aerospace Private Limited

- Orion AST

- Rogue Space Systems

- Scout Aerospace LLC

- Space Machines Company Pty Ltd

- Tethers Unlimited, Inc.

- Thales Alenia Space

- Turion Space

目次

The Global On-Orbit Satellite Servicing Market is poised for significant growth, reaching USD 2.7 billion in 2024, with projections pointing to an impressive CAGR of 11.6% from 2025 to 2034. This rapid expansion is driven by the increasing demand for satellite maintenance, repair, and upgrades aimed at extending operational lifespans, cutting launch costs, and boosting performance. The rising deployment of satellites for key applications such as communications, Earth observation, and defense further accelerates the market's growth trajectory.

When analyzing the market by orbit type, Low Earth Orbit (LEO) takes the lead, commanding 82.8% of the market share in 2024. LEO's dominance can be attributed to the explosion of satellite constellations, particularly those focused on global broadband coverage and remote sensing. The dense satellite presence in this orbit necessitates innovative solutions, including robotic refueling, repair, and debris removal. Additionally, the proximity of LEO to Earth makes it easier to conduct frequent and cost-effective servicing missions, ensuring the sustainability and efficiency of satellite operations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.7 Billion |

| Forecast Value | $8 Billion |

| CAGR | 11.6% |

In terms of end users, the on-orbit satellite servicing market is segmented into government and military entities and commercial operators. The government and military segment is expected to experience the fastest growth, with a forecasted CAGR of 12.6% during the 2025-2034 period. Increased investments in satellite infrastructure are fueling this demand as governments seek to preserve the functionality of critical space assets, enhance national security, and reduce replacement costs. Furthermore, collaborations between the public and private sectors are driving technological advancements, which will play a crucial role in accelerating the growth of this segment.

North America is set to dominate the global on-orbit satellite servicing market, with expectations to reach USD 3.5 billion by 2034. The region's strong position stems from substantial investments in space technologies and a well-established presence of key players in the industry. Government programs supporting innovation, coupled with increasing demand for satellite communication and defense solutions, are solidifying North America's leadership in this space. Additionally, the region's commitment to sustainable space practices and breakthroughs in in-orbit servicing technologies further enhances its market position.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Surge in satellite constellations and space traffic

- 3.6.1.2 Cost savings through satellite lifecycle extension

- 3.6.1.3 Breakthroughs in space robotics and automation

- 3.6.1.4 Growing government and private sector investment

- 3.6.1.5 Enhanced focus on space debris management

- 3.6.2 Industry pitfalls & challenges

- 3.6.3 High development and operational costs

- 3.6.4 Technical complexity and operational risks

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Service, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Active Debris Removal (ADR) and Orbit Adjustment

- 5.3 Robotic servicing

- 5.4 Refueling

- 5.5 Assembly

Chapter 6 Market Estimates & Forecast, By Orbit Type, 2021 – 2034 (USD Million)

- 6.1 Key trends

- 6.2 Low Earth Orbit (LEO)

- 6.3 Medium Earth Orbit (MEO)

- 6.4 Geostationary Orbit (GEO)

Chapter 7 Market Estimates & Forecast, By Satellite Type, 2021 – 2034 (USD Million)

- 7.1 Key trends

- 7.2 Small satellite (<500 Kg)

- 7.3 Medium satellite (501-1,000 Kg)

- 7.4 Large satellite (>1,000 Kg)

Chapter 8 Market Estimates & Forecast, By End Use, 2021 – 2034 (USD Million)

- 8.1 Key trends

- 8.2 Government and military

- 8.3 Commercial operators

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Airbus SE

- 10.2 Altius Space Machines, Inc.

- 10.3 Astroscale Holdings Inc.

- 10.4 Atomos Space

- 10.5 ClearSpace

- 10.6 Future Space Industries

- 10.7 High Earth Orbit Robotics

- 10.8 Hyoristic Innovations

- 10.9 Infinite Orbits

- 10.10 Lúnasa Ltd.

- 10.11 Maxar Technologies

- 10.12 Momentus, Inc.

- 10.13 Nanoracks (Voyager Space)

- 10.14 Obruta Space Solutions Corp

- 10.15 Orbit Fab, Inc.

- 10.16 Orbitaid Aerospace Private Limited

- 10.17 Orion AST

- 10.18 Rogue Space Systems

- 10.19 Scout Aerospace LLC

- 10.20 Space Machines Company Pty Ltd

- 10.21 Tethers Unlimited, Inc.

- 10.22 Thales Alenia Space

- 10.23 Turion Space

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日