|

市場調査レポート

商品コード

1665194

自動車用Eコンプレッサの市場機会、成長促進要因、産業動向分析、2025~2034年予測Automotive E-Compressor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用Eコンプレッサの市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2024年12月14日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

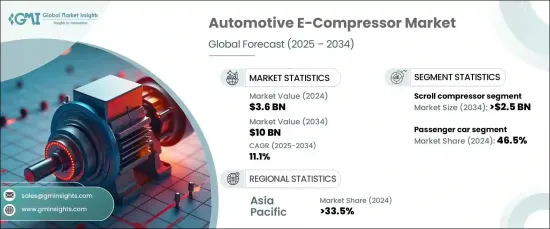

2024年の自動車用Eコンプレッサの世界市場規模は36億米ドルで、2025~2034年のCAGRは11.1%と予想され、著しい成長が見込まれています。

この成長は、最新の電気自動車(EV)やハイブリッド車に不可欠なコンポーネントとなりつつある、先進的熱管理システムに対する需要の増加によるところが大きいです。これらの自動車が進化を続けるにつれ、バッテリー、電気モーター、キャビン、パワーエレクトロニクスなどの重要部品の温度管理は、最適な性能を発揮するためにますます重要になっています。このシステムで重要な役割を果たす自動車用Eコンプレッサは、そのエネルギー効率と、内燃エンジン(ICE)を動力源とする従来の機械式コンプレッサへの依存度を大幅に低減する能力で高く評価されています。この技術シフトは、自動車産業における持続可能でエネルギー効率の高いソリューションへの幅広い後押しと一致し、市場の成長をさらに加速させています。

自動車用eコンプレッサ市場は、スクロール、ロータリー、レシプロ、スクリュー、その他など、コンプレッサタイプ別に区分されます。2024年には、スクロールコンプレッサセグメントが33%の市場シェアを占め、2034年までに25億米ドルを生み出すと予測されています。スクロールコンプレッサは、その信頼性、静かな動作、コンパクトな設計で特に好まれ、最新の自動車用途に最適です。これらの特長により、スペース効率と性能が最も重視される電気自動車やハイブリッド車での使用に特に適しています。スクロールコンプレッサの技術には、2つのらせん状のスクロールがあり、一方は静止したまま、もう一方が円を描くように動いて冷媒を圧縮します。このプロセスにより、EVやハイブリッド車の快適性と機能性を向上させるための重要な要素である、高効率と騒音レベルの低減が保証されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034 |

| 開始金額 | 36億米ドル |

| 予測金額 | 100億米ドル |

| CAGR | 11.1% |

市場を車種別に見ると、自動車用Eコンプレッサ市場は乗用車、商用車、オフハイウェイ車に分けられます。2024年には、乗用車が46.5%の市場シェアを占め、最大セグメントとなります。この優位性は、電気自動車とハイブリッド車の人気の高まりによるところが大きく、乗用車はより環境に優しい輸送ソリューションへの移行を主導しています。これらの自動車では、Eコンプレッサが従来のベルト駆動コンプレッサに代わるよりエネルギー効率の高い選択肢を提供し、エネルギー消費を最小限に抑えながら、より優れた熱管理を保証します。エンジンがエアコンを駆動する内燃機関車とは異なり、電気自動車は車両のバッテリーと電気モーターを動力源とするEコンプレッサに依存しています。

アジア太平洋は、2024年に自動車用Eコンプレッサの世界市場で33.5%のシェアを占め、同地域の電気自動車産業の急速な拡大に牽引されました。特に中国は、補助金、税制優遇措置、二酸化炭素排出量削減を目的とした施策など、政府の強力な取り組みに支えられ、電気自動車の最大の生産国・消費国となっています。BYD、NIO、XPeng、Geelyといった中国の大手自動車メーカーが電気自動車の開発と販売を主導しており、同地域の自動車用Eコンプレッサ市場は今後数年で継続的に成長する展望です。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推定の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場定義

第2章 エグゼクティブサマリー

第3章 産業洞察

- エコシステム分析

- サプライヤーの状況

- 原料サプライヤー

- 部品メーカー

- 技術プロバイダー

- エンドユーザー

- 利益率分析

- 技術とイノベーションの展望

- コスト内訳

- 主要ニュースと取り組み

- 規制状況

- 価格分析

- 影響要因

- 促進要因

- EV導入の急増

- コンプレッサ技術の進歩

- 先進的機能に対する消費者の需要

- 熱管理システムへの注目の高まり

- 産業の潜在的リスク・課題

- 電動コンプレッサの初期コストの高さ

- 技術的・統合的課題

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推定・予測:コンプレッサ別、2021~2034年

- 主要動向

- スクロール

- ロータリー

- レシプロ

- スクリュー

- その他

第6章 市場推定・予測:冷却能力別、2021~2034年

- 主要動向

- 低容量(5kW以下)

- 中容量(5~10 kW)

- 大容量(10kW以上)

第7章 市場推定・予測:用途別、2021~2034年

- 主要動向

- キャビン空調

- バッテリー熱管理

- パワートレイン冷却

- 電動ドライブトレイン冷却

- その他

第8章 市場推定・予測:推進力別、2021~2034年

- 主要動向

- 電気自動車

- ハイブリッド

第9章 市場推定・予測:車両別、2021~2034年

- 主要動向

- 乗用車

- セダン

- SUV

- ハッチバック

- 商用車

- LCV

- HCV

- オフハイウェイ車

第10章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- Bosch

- Boyard Compressor

- Denso

- Elgi Equipment

- Gardner Denver

- Garrett

- Guchen Industry

- Hanon Systems

- Highly Marelli

- Infineon

- Mahle

- Mitsubishi

- Novosense

- Sanden

- Siroco

- TCCI

- Toyota

- Valeo

- Vikas Group

- ZF Friedrichshafen

The Global Automotive E-Compressor Market, valued at USD 3.6 billion in 2024, is set to experience remarkable growth, with an expected CAGR of 11.1% from 2025 to 2034. This growth is largely driven by the increasing demand for advanced thermal management systems, which are becoming an essential component in modern electric vehicles (EVs) and hybrids. As these vehicles continue to evolve, managing the temperature of critical components such as batteries, electric motors, cabins, and power electronics has become increasingly important for optimal performance. Automotive e-compressors, which play a pivotal role in this system, are highly valued for their energy efficiency and their ability to significantly reduce reliance on traditional mechanical compressors powered by internal combustion engines (ICEs). This shift in technology aligns with the broader push towards sustainable and energy-efficient solutions in the automotive industry, further accelerating market growth.

The market for automotive e-compressors is segmented by compressor type, including scroll, rotary, reciprocating, screw, and others. In 2024, the scroll compressor segment commanded a substantial 33% market share and is projected to generate USD 2.5 billion by 2034. Scroll compressors are particularly favored for their reliability, quiet operation, and compact design, making them ideal for modern automotive applications. These features make them especially suitable for use in electric and hybrid vehicles, where space efficiency and performance are paramount. The technology behind scroll compressors involves two spiral-shaped scrolls, one of which remains stationary while the other moves in a circular motion to compress refrigerant. This process ensures high efficiency and reduced noise levels, critical factors for improving the comfort and functionality of EVs and hybrids.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.6 Billion |

| Forecast Value | $10 Billion |

| CAGR | 11.1% |

Looking at the market from a vehicle type perspective, the automotive e-compressor market is divided into passenger cars, commercial vehicles, and off-highway vehicles. In 2024, passenger cars represented the largest segment with a 46.5% market share. This dominance is largely due to the increasing popularity of electric and hybrid vehicles, with passenger cars leading the transition to more eco-friendly transportation solutions. In these vehicles, e-compressors offer a more energy-efficient alternative to traditional belt-driven compressors, ensuring better thermal management while minimizing energy consumption. Unlike ICE-powered vehicles, where the engine drives the air conditioning, electric vehicles rely on e-compressors powered by the vehicle's battery and electric motor.

Asia Pacific held a 33.5% share of the global automotive e-compressor market in 2024, driven by rapid expansion in the region's electric vehicle industry. China, in particular, has become the largest producer and consumer of electric vehicles, supported by strong government initiatives including subsidies, tax incentives, and policies aimed at reducing carbon emissions. With major Chinese automakers like BYD, NIO, XPeng, and Geely leading the charge in EV development and sales, the region's automotive e-compressor market is poised for continued growth in the coming years.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 360º synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material suppliers

- 3.2.2 Component manufacturers

- 3.2.3 Technology providers

- 3.2.4 End users

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Cost breakdown

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Pricing analysis

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Surge in EV adoption

- 3.9.1.2 Advancements in compressor technology

- 3.9.1.3 Consumer demand for advanced features

- 3.9.1.4 Increased focus on thermal management systems

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High initial cost of electric compressors

- 3.9.2.2 Technological and integration challenges

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Compressor, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Scroll

- 5.3 Rotary

- 5.4 Reciprocating

- 5.5 Screw

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Cooling Capacity, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Low capacity (Below 5 kW)

- 6.3 Medium capacity (5-10 kW)

- 6.4 High capacity (Above 10 kW)

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Cabin air conditioning

- 7.3 Battery thermal management

- 7.4 Powertrain cooling

- 7.5 Electric drivetrain cooling

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Electric

- 8.3 Hybrid

Chapter 9 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Passenger cars

- 9.2.1 Sedan

- 9.2.2 SUV

- 9.2.3 Hatchback

- 9.3 Commercial vehicle

- 9.3.1 LCV

- 9.3.2 HCV

- 9.4 Off highway vehicle

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Bosch

- 11.2 Boyard Compressor

- 11.3 Denso

- 11.4 Elgi Equipment

- 11.5 Gardner Denver

- 11.6 Garrett

- 11.7 Guchen Industry

- 11.8 Hanon Systems

- 11.9 Highly Marelli

- 11.10 Infineon

- 11.11 Mahle

- 11.12 Mitsubishi

- 11.13 Novosense

- 11.14 Sanden

- 11.15 Siroco

- 11.16 TCCI

- 11.17 Toyota

- 11.18 Valeo

- 11.19 Vikas Group

- 11.20 ZF Friedrichshafen