ヒト免疫不全ウイルス治療薬市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Human Immunodeficiency Virus Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 145 Pages

- 納期

- 2~3営業日

- 商品コード

- 1665059

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

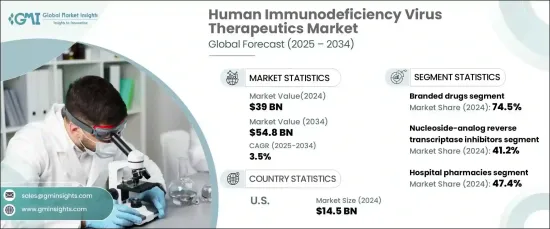

ヒト免疫不全ウイルス治療薬の世界市場は、2024年に390億米ドルの評価額に達し、2025年から2034年にかけてCAGR 3.5%で安定した成長を遂げると予測されています。

市場拡大の主な要因は、HIV感染率の上昇、治療法の大幅な進歩、政府の積極的な取り組み、有利な規制当局の承認などです。これらの要因が相まって、市場の継続的な成長軌道を促進する上で重要な役割を果たしています。

市場は主に薬剤の種類によってブランド薬とジェネリック医薬品に区分されます。2024年には、ブランド薬が74.5%という大幅なシェアで市場をリードしており、その理由は、有効性が実証されていること、長年の臨床的信頼性があること、HIV治療における実績が信頼されていることによるものです。合剤は、投与レジメンを簡略化し、患者の治療計画へのアドヒアランスを高めることから、広く普及しています。特にウイルス量を効果的に抑制するための併用療法における重要な役割は、市場の需要を引き続き牽引しており、今後数年間における市場の安定した成長を確実なものにしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 390億米ドル |

| 予測金額 | 548億米ドル |

| CAGR | 3.5% |

市場の流通チャネルは、HIV治療薬のリーチとアクセシビリティをさらに際立たせています。主な流通セグメントには、ドラッグストアや小売薬局、オンライン薬局、病院薬局が含まれます。2024年には、病院薬局が47.4%という特筆すべき市場最大シェアを占めています。病院薬局は、高度な抗レトロウイルス療法や慎重な投与が必要な注射治療など、より幅広い専門的なHIV治療薬を提供するための設備が整っています。医療専門家の監督の下、併用療法を含む最先端の治療を提供できることから、専門的なケアと配慮を必要とする患者にとって好ましい選択肢となっています。

米国では、HIV治療薬市場は2024年に145億米ドルを創出しました。同国は高度に発達した医療インフラの恩恵を受けており、臨床試験や長時間作用型注射療法など、先進的なHIV治療へのアクセスが広く確保されています。メディケイドやメディケアのような健康保険制度が広く普及しているため、患者は必要な救命治療を受けることができます。さらに、小売薬局、病院施設、オンライン・プラットフォームの広範なネットワークは、HIV治療薬のシームレスな流通と入手を促進し、患者が必要とする治療法に容易にアクセスできることを保証しています。

世界のヒト免疫不全ウイルス(HIV)治療薬市場は、2024年に390億米ドルの評価額に達し、2025年から2034年にかけてCAGR 3.5%で安定した成長を遂げると予測されています。市場拡大の主な要因は、HIV感染率の上昇、治療法の大幅な進歩、政府の支援策、有利な規制当局の承認です。これらの要因が相まって、市場の継続的な成長軌道を促進する上で重要な役割を果たしています。

市場は主に薬剤の種類によってブランド薬とジェネリック医薬品に区分されます。2024年には、ブランド薬が74.5%という大幅なシェアで市場をリードしており、その理由は、有効性が実証されていること、長年の臨床的信頼性があること、HIV治療における実績が信頼されていることによるものです。合剤は、投与レジメンを簡略化し、患者の治療計画へのアドヒアランスを高めることから、広く普及しています。特にウイルス量を効果的に抑制するという、併用療法における重要な役割は、引き続き市場の需要を牽引しており、今後も安定した市場成長が見込まれます。

市場の流通チャネルは、HIV治療薬のリーチとアクセシビリティをさらに際立たせています。主な流通経路は、ドラッグストアや小売薬局、オンライン薬局、病院薬局などです。2024年では、病院薬局が47.4%と最大のシェアを占めています。病院薬局は、高度な抗レトロウイルス療法や慎重な投与が必要な注射治療など、より幅広い専門的なHIV治療薬を提供するための設備が整っています。医療専門家の監督の下、併用療法を含む最先端の治療を提供できることから、専門的なケアと配慮を必要とする患者にとって好ましい選択肢となっています。

米国では、HIV治療薬市場は2024年に145億米ドルを創出しました。同国は高度に発達した医療インフラの恩恵を受けており、臨床試験や長時間作用型注射療法など、先進的なHIV治療へのアクセスが広く確保されています。メディケイドやメディケアのような健康保険制度が広く普及しているため、患者は必要な救命治療を受けることができます。さらに、小売薬局、病院施設、医療機関などの広範なネットワークは、患者を救命するために必要な治療法を提供することを可能にしています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- HIV感染率の高さ

- 治療オプションの進歩

- 政府のイニシアティブや保健プログラムによる支援の拡大

- 有利な規制当局の承認

- 業界の潜在的リスク&課題

- 高額な治療費

- 患者のアドヒアランスと治療の継続性に関する懸念

- 促進要因

- 成長可能性分析

- 規制状況

- ギャップ分析

- 特許分析

- 技術的展望

- 今後の市場動向

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略展望

第5章 市場推計・予測:薬剤タイプ別、2021年~2034年

- 主要動向

- ブランド医薬品

- ジェネリック医薬品

第6章 市場推計・予測:薬剤クラス別、2021年~2034年

- 主要動向

- ヌクレオシドアナログ系逆転写酵素阻害薬

- インテグラーゼ阻害薬

- 非ヌクレオシド系逆転写酵素阻害薬

- プロテアーゼ阻害剤

- 侵入・融合阻害剤

- コレセプター拮抗薬

第7章 市場推計・予測:流通チャネル別、2021~2034年

- 主要動向

- 病院薬局

- ドラッグストアおよび小売薬局

- オンライン薬局

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- AbbVie

- Aurobindo Pharma

- Boehringer Ingelheim International GmbH

- Bristol-Myers Squibb Company

- Cipla

- Dr. Reddy's Laboratories

- F. Hoffmann-La Roche

- Gilead Sciences

- Hetero Drugs

- Johnson &Johnson

- Merck &Co

- Mylan N.V.(Viatris)

- Sun Pharmaceutical Industries

- Teva Pharmaceutical Industries

- ViiV Healthcare

目次

The Global Human Immunodeficiency Virus Therapeutics Market reached a valuation of USD 39 billion in 2024 and is projected to experience steady growth at a CAGR of 3.5% from 2025 to 2034. The market expansion is largely driven by the rising rates of HIV infections, significant advancements in treatment options, supportive government initiatives, and favorable regulatory approvals. These factors combined are playing a crucial role in fostering the market's ongoing growth trajectory.

The market is primarily segmented by drug type into branded and generic drugs. In 2024, branded drugs led the market with a substantial share of 74.5%, attributed to their proven efficacy, long-standing clinical reliability, and trusted performance in HIV treatment. Fixed-dose combinations have been gaining widespread popularity, as they offer simplified dosing regimens that enhance patient adherence to treatment plans. Their key role in combination therapies, particularly for effectively suppressing viral loads, continues to drive demand in the market, ensuring consistent market growth in the years to come.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $39 Billion |

| Forecast Value | $54.8 Billion |

| CAGR | 3.5% |

The market's distribution channels further highlight the reach and accessibility of HIV therapeutics. The primary distribution segments include drug stores and retail pharmacies, online pharmacies, and hospital pharmacies. In 2024, hospital pharmacies held the largest share of the market, with a notable 47.4%. Hospital pharmacies are well-equipped to offer a broader selection of specialized HIV medications, including advanced antiretroviral therapies and injectable treatments that require careful administration. Their ability to provide cutting-edge treatments, including combination regimens, under the supervision of healthcare professionals makes them the preferred choice for patients who require specialized care and attention.

In the United States, the HIV therapeutics market generated USD 14.5 billion in 2024. The country benefits from a highly developed healthcare infrastructure that ensures widespread access to advanced HIV treatments, including clinical trials and long-acting injectable therapies. The widespread availability of health insurance programs, such as Medicaid and Medicare, further guarantees that patients can afford the life-saving therapies they need. Moreover, the extensive network of retail pharmacies, hospital facilities, and online platforms helps facilitate seamless distribution and availability of HIV therapeutics, ensuring that patients can easily access the treatments they require.

The global Human Immunodeficiency Virus (HIV) therapeutics market reached a valuation of USD 39 billion in 2024 and is projected to experience steady growth at a CAGR of 3.5% from 2025 to 2034. The market expansion is largely driven by the rising rates of HIV infections, significant advancements in treatment options, supportive government initiatives, and favorable regulatory approvals. These factors combined are playing a crucial role in fostering the market's ongoing growth trajectory.

The market is primarily segmented by drug type into branded and generic drugs. In 2024, branded drugs led the market with a substantial share of 74.5%, attributed to their proven efficacy, long-standing clinical reliability, and trusted performance in HIV treatment. Fixed-dose combinations have been gaining widespread popularity, as they offer simplified dosing regimens that enhance patient adherence to treatment plans. Their key role in combination therapies, particularly for effectively suppressing viral loads, continues to drive demand in the market, ensuring consistent market growth in the years to come.

The market's distribution channels further highlight the reach and accessibility of HIV therapeutics. The primary distribution segments include drug stores and retail pharmacies, online pharmacies, and hospital pharmacies. In 2024, hospital pharmacies held the largest share of the market, with a notable 47.4%. Hospital pharmacies are well-equipped to offer a broader selection of specialized HIV medications, including advanced antiretroviral therapies and injectable treatments that require careful administration. Their ability to provide cutting-edge treatments, including combination regimens, under the supervision of healthcare professionals makes them the preferred choice for patients who require specialized care and attention.

In the United States, the HIV therapeutics market generated USD 14.5 billion in 2024. The country benefits from a highly developed healthcare infrastructure that ensures widespread access to advanced HIV treatments, including clinical trials and long-acting injectable therapies. The widespread availability of health insurance programs, such as Medicaid and Medicare, further guarantees that patients can afford the life-saving therapies they need. Moreover, the extensive network of retail pharmacies, hospital facilities, and on

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates & calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 High incidence of HIV infections

- 3.2.1.2 Advances in therapeutic treatment options

- 3.2.1.3 Growing support through government initiatives and health programs

- 3.2.1.4 Favorable regulatory approvals

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High cost of treatment

- 3.2.2.2 Concerns related to patient adherence and treatment continuity

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Gap analysis

- 3.6 Patent analysis

- 3.7 Technological landscape

- 3.8 Future market trends

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy outlook

Chapter 5 Market Estimates and Forecast, By Drug Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Branded drugs

- 5.3 Generic drugs

Chapter 6 Market Estimates and Forecast, By Drug Class, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Nucleoside-analog reverse transcriptase inhibitors

- 6.3 Integrase inhibitors

- 6.4 Non-nucleoside reverse transcriptase inhibitors

- 6.5 Protease inhibitors

- 6.6 Entry and fusion inhibitors

- 6.7 Coreceptor antagonists

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospital pharmacies

- 7.3 Drugs stores and retail pharmacies

- 7.4 Online pharmacies

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AbbVie

- 9.2 Aurobindo Pharma

- 9.3 Boehringer Ingelheim International GmbH

- 9.4 Bristol-Myers Squibb Company

- 9.5 Cipla

- 9.6 Dr. Reddy's Laboratories

- 9.7 F. Hoffmann-La Roche

- 9.8 Gilead Sciences

- 9.9 Hetero Drugs

- 9.10 Johnson & Johnson

- 9.11 Merck & Co

- 9.12 Mylan N.V. (Viatris)

- 9.13 Sun Pharmaceutical Industries

- 9.14 Teva Pharmaceutical Industries

- 9.15 ViiV Healthcare

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 145 Pages

- 納期

- 2~3営業日