自動車用ブレーキブースターとマスターシリンダー市場の機会、成長促進要因、産業動向分析、2025~2034年の予測

Automotive Brake Booster and Master Cylinder Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1665025

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

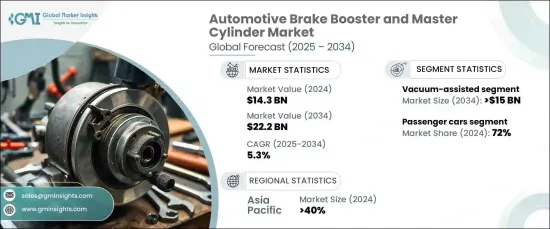

自動車用ブレーキブースターとマスターシリンダーの世界市場は、2024年に143億米ドルと評価され、2025年から2034年にかけてCAGR 5.3%で拡大すると予測され、大きな成長が見込まれています。

この市場成長は、高度なブレーキシステムを必要とする電気自動車や自律走行車の採用が増加していることが大きな要因となっています。電気自動車(EV)は、電動ブレーキブースターの需要急増に寄与しています。従来のブレーキシステムはエンジンの真空に依存しているが、EVにはこの機能がないためです。

同時に、世界各国の政府が安全規制を強化しているため、高度なブレーキ・ソリューションの需要がさらに高まっています。こうした規制は、安全性を高め、事故を減らし、死者を最小限に抑えるために、新車と後付けモデルの両方に高度なブレーキ・システムを組み込むことを後押ししています。北米、欧州、アジア太平洋の一部などの主要地域で規制遵守が重視されていることが、こうした技術の採用を促進する主な要因となっており、市場の成長を後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 143億米ドル |

| 予測金額 | 222億米ドル |

| CAGR | 5.3% |

ブレーキ・ブースター市場は、真空アシスト、油圧アシスト、電子ブレーキの3つの主要技術に分類されます。真空アシスト・ブレーキ・ブースターは、2024年に最大シェアを占め、市場の65%を占める。この技術は2034年までに150億米ドルに達すると予想されています。バキュームアシスト・ブースターは、費用対効果と効率性から乗用車や小型商用車に好んで使用されています。エンジンの真空を利用して制動力を高めることで、これらのブースターは信頼性と内燃エンジンとの互換性を提供し、従来の車種にとって理想的な選択肢となっています。

車種別では、乗用車が自動車用ブレーキブースターとマスターシリンダー市場を独占しており、2024年の市場シェア全体の72%を占めています。このリーダーシップは、世界的に乗用車の生産・販売台数が多いことに起因しています。乗用車セグメントには、セダン、SUV、ハッチバックなど幅広い乗用車が含まれ、これらすべてが市場全体の成長に重要な役割を果たしています。

アジア太平洋地域は2024年に市場シェアの40%を占め、2034年までに95億米ドルを生み出すと予想されています。この地域の主要国である中国は、2034年までに40億米ドルの市場貢献が見込まれています。乗用車と商用車の膨大な生産と消費により、中国は世界の自動車産業において支配的な役割を担っており、先進的なブレーキ技術に対する大きな需要を引き続き牽引しています。中国とアジア太平洋地域の自動車市場が拡大するにつれ、高品質で効率的なブレーキ・システムへのニーズはますます高まっていくと思われます。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- 原材料サプライヤー

- 部品メーカー

- ブレーキブースターおよびマスターシリンダーメーカー

- 自動車部品サプライヤー

- 相手先商標製品メーカー(OEM)

- 利益率分析

- コスト内訳分析

- 技術革新の展望

- 主要ニュース&イニシアティブ

- 規制状況

- 影響要因

- 促進要因

- EVと自律走行車の普及拡大

- 交通安全に対する意識の高まりと先進ブレーキシステムに対する規制の義務化

- 電動ブレーキブースターなどの技術革新の進展

- 新興市場における自動車生産の増加

- 業界の潜在的リスク&課題

- 先端技術の高コスト

- 新興経済諸国における市場の飽和

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ブレーキブースター

- 真空ブレーキブースター

- 油圧式ブレーキブースター

- マスターシリンダー

- タンデムマスターシリンダー

- シングルマスターシリンダー

第6章 市場推計・予測:推進力別、2021年~2034年

- 主要動向

- ICE

- 電気自動車

- バッテリー電気自動車(BEV)

- プラグインハイブリッド車(PHEV)

- ハイブリッド電気自動車(HEV)

第7章 市場推計・予測:2021~2034年、車両別

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV

- 商用車

- 小型商用車(LCV)

- 大型商用車(HCV)

第8章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 真空アシスト

- 油圧アシスト

- 電子式ブレーキブースター

第9章 市場推計・予測:販売チャネル別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第10章 市場推計・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- ADVICS Co.

- Aisin

- Akebono Brake Industry

- Brembo

- Cardone Industries

- Continental

- DENSO

- Federal-Mogul Holdings Corporation

- Haldex

- Hitachi Astemo

- Hyundai Mobis

- Knorr-Bremse

- KYB

- Magneti Marelli

- Mando

- Nissin Kogyo

- Robert Bosch

- Tenneco

- TRW Automotive

- ZF Friedrichshafen

目次

The Global Automotive Brake Booster And Master Cylinder Market was valued at USD 14.3 billion in 2024 and is expected to experience significant growth, projected to expand at a CAGR of 5.3% from 2025 to 2034. This market growth is largely driven by the increasing adoption of electric and autonomous vehicles, which require advanced braking systems. Electric vehicles (EVs) are contributing to a surge in demand for electric brake boosters, as traditional braking systems rely on engine vacuum-a feature that EVs do not have.

At the same time, governments worldwide are tightening safety regulations, which is further boosting the demand for sophisticated braking solutions. These regulations are pushing the integration of advanced braking systems in both new vehicles and retrofitted models to enhance safety, reduce accidents, and minimize fatalities. The emphasis on regulatory compliance in key regions such as North America, Europe, and parts of Asia-Pacific is a major factor driving the adoption of these technologies, thereby fueling market growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $14.3 Billion |

| Forecast Value | $22.2 Billion |

| CAGR | 5.3% |

The market is divided into three primary brake booster technologies: vacuum-assisted, hydraulic-assisted, and electronic brake boosters. Vacuum-assisted brake boosters held the largest share in 2024, accounting for 65% of the market. This technology is expected to reach USD 15 billion by 2034. Vacuum-assisted boosters are the preferred choice for passenger and light commercial vehicles due to their cost-effectiveness and efficiency. By utilizing the engine's vacuum to enhance braking force, these boosters offer reliability and compatibility with internal combustion engines, making them an ideal option for traditional vehicle models.

In terms of vehicle type, passenger cars dominate the automotive brake booster and master cylinder market, representing 72% of the total market share in 2024. This leadership is attributed to the high production and sales volumes of passenger vehicles globally. The passenger car segment includes a wide range of personal vehicles, including sedans, SUVs, and hatchbacks, all of which play a vital role in the market's overall growth.

The Asia-Pacific region accounted for 40% of the market share in 2024 and is expected to generate USD 9.5 billion by 2034. China, as the leading country in this region, is forecast to contribute USD 4 billion to the market by 2034. China's dominant role in the global automotive industry, with its vast production and consumption of both passenger and commercial vehicles, continues to drive substantial demand for advanced braking technologies. As the automotive market in China and the Asia-Pacific region expands, the need for high-quality, efficient braking systems will only continue to grow.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material suppliers

- 3.2.2 Component manufacturers

- 3.2.3 Brake booster and master cylinder manufacturers

- 3.2.4 Tier-1 automotive suppliers

- 3.2.5 Original equipment manufacturers (OEMs)

- 3.3 Profit margin analysis

- 3.4 Cost breakdown analysis

- 3.5 Technology & innovation landscape

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 The rising adoption of EVs and autonomous vehicles

- 3.8.1.2 Growing awareness about road safety and regulatory mandates for advanced braking systems

- 3.8.1.3 Technological advancements in innovations such as electric brake boosters

- 3.8.1.4 Growing vehicle production in emerging markets

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High cost of advanced technologies

- 3.8.2.2 Market saturation in developed economies

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter’s analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Brake booster

- 5.2.1 Vacuum brake booster

- 5.2.2 Hydraulic brake booster

- 5.3 Master cylinder

- 5.3.1 Tandem master cylinder

- 5.3.2 Single master cylinder

Chapter 6 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 ICE

- 6.3 Electric vehicles

- 6.3.1 Battery electric vehicles (BEV)

- 6.3.2 Plug-in hybrid electric vehicles (PHEV)

- 6.3.3 Hybrid electric vehicles (HEV)

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 Light commercial vehicles (LCV)

- 7.3.2 Heavy commercial vehicles (HCV)

Chapter 8 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Vacuum-assisted

- 8.3 Hydraulic-assisted

- 8.4 Electronic brake boosters

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEMs

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 ADVICS Co.

- 11.2 Aisin

- 11.3 Akebono Brake Industry

- 11.4 Brembo

- 11.5 Cardone Industries

- 11.6 Continental

- 11.7 DENSO

- 11.8 Federal-Mogul Holdings Corporation

- 11.9 Haldex

- 11.10 Hitachi Astemo

- 11.11 Hyundai Mobis

- 11.12 Knorr-Bremse

- 11.13 KYB

- 11.14 Magneti Marelli

- 11.15 Mando

- 11.16 Nissin Kogyo

- 11.17 Robert Bosch

- 11.18 Tenneco

- 11.19 TRW Automotive

- 11.20 ZF Friedrichshafen

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日