|

市場調査レポート

商品コード

1664899

自動車用連続可変容量オイルポンプの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Automotive Continuously Variable Capacity (CVC) Oil Pump Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用連続可変容量オイルポンプの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2024年12月05日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

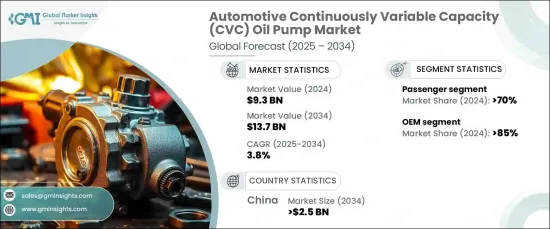

自動車用連続可変容量オイルポンプの世界市場は、2024年には93億米ドルとなり、2025年から2034年にかけてCAGR3.8%で成長すると予測されています。

この成長は、燃費の向上とますます厳しくなる排ガス規制への対応に重点が置かれていることが主な要因です。世界各国の政府がより環境に優しい輸送ソリューションを提唱する中、自動車メーカーはCVCオイルポンプなどの先進コンポーネントを急速に採用しています。これらのポンプは、燃料効率の向上、エンジン性能の最適化、ハイブリッドおよび電気パワートレインのサポートにおいて極めて重要な役割を果たしています。

また、消費者や産業界がエネルギー効率の高い技術を求める中、電気自動車の導入が急増していることも、この市場の追い風となっています。変化するエンジン負荷に適応する能力で知られるCVCオイルポンプは、持続可能性と性能を優先する自動車の標準装備になりつつあります。この分野での技術革新は加速しており、メーカーは世界基準を満たし、進化する消費者の期待に応えるため、ポンプ設計の改善に注力しています。さらに、これらのポンプにスマートシステムと先端材料を統合することで、全体的な効率と寿命が向上し、最新の自動車システムに不可欠なものとなっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 93億米ドル |

| 予測金額 | 137億米ドル |

| CAGR | 3.8% |

車両タイプ別では、乗用車と商用車に分類されます。2024年には、乗用車が市場全体の70%を占め、収益に大きく貢献します。このセグメントは2034年までに80億米ドルに成長すると予測されています。乗用車の優位性は、生産台数の増加と燃費の良い車に対する消費者の選好の高まりに起因しています。自動車メーカーは、厳しい環境規制を遵守し、環境意識の高い消費者の性能要求を満たすために、CVCオイルポンプのような先進技術を取り入れています。こうした努力は、規制遵守を確実にするだけでなく、メーカーが市場で競争優位に立つことにも役立っています。

販売チャネルに基づき、市場はOEMとアフターマーケットに区分されます。2024年には、OEM部門が市場シェアの85%を占め、予測期間を通じて主導的地位を維持すると予想されます。OEMは、CVCオイルポンプのような先進システムの採用に不可欠であり、製造工程でこれらの技術を統合するリソースを持っているからです。研究開発への投資能力により、進化する排出基準を満たしながら車両性能を向上させる最先端システムの採用が保証されます。大規模な製造能力と持続可能性を重視したパートナーシップは、市場におけるOEMセグメントの優位性をさらに高めています。

地域別力学では、中国が2024年の自動車用CVCオイルポンプ市場で60%の圧倒的シェアを占めました。同地域は2034年までに25億米ドルを生み出すと予想され、自動車製造の世界的リーダーとしての地位を固めています。環境問題に対処するため、中国がハイブリッド車や電気自動車の生産に力を入れていることが、効率的なオイルポンプ技術に対する需要の大きな原動力となっています。中国の自動車メーカーは、排ガスに関する規制ガイドラインを遵守しながら、最新のパワートレインの性能要件をサポートする先進システムを採用しています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 一次調査と検証

- 一次ソース

- データマイニングソース

- 市場定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- サプライヤーの状況

- OEM CVCオイルポンプメーカー

- アフターマーケットプロバイダー

- 流通業者

- エンドユーザー

- 利益率分析

- 価格分析

- 特許情勢

- コスト内訳分析

- 技術革新の状況

- 主要ニュース・イニシアチブ

- 規制状況

- 影響要因

- 成長促進要因

- 燃費と排出ガスに関する政府の厳しい規制

- ハイブリッド車と電気自動車(HEVとEV)の需要の増加

- 車両性能の最適化と熱管理への注目の高まり

- 自動車パワートレインシステムの技術進歩

- 業界の潜在的リスク・課題

- 連続可変容量オイルポンプの初期コストの高さと複雑さ

- 市場競争激化による価格圧力

- 成長促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業市場シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 可変容量オイルポンプ

- 電動オイルポンプ

- 機械式オイルポンプ

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- エンジン潤滑

- トランスミッション

- ハイブリッドパワートレイン

第7章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV車

- 商用車

- 小型商用車(LCV)

- 大型商用車(HCV)

第8章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 油圧制御

- 電子制御

第9章 市場推計・予測:販売チャネル別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- Aisin Seiki

- BorgWarner

- Bosch

- Continental

- Cummins

- Denso

- FTE Automotive

- Hanon Systems

- Hitachi Astemo

- Johnson Electric

- Magna International

- Mahle GmbH

- Melling Tool Company

- Mikuni

- Pierburg

- Rheinmetall Automotive

- Shw Automotive

- SKF Group

- Stackpole

- Yamada Manufacturing

The Global Automotive Continuously Variable Capacity Oil Pump Market was valued at USD 9.3 billion in 2024 and is projected to grow at a CAGR of 3.8% between 2025 and 2034. This growth is largely driven by a heightened focus on improving fuel efficiency and meeting increasingly stringent emission regulations. As governments worldwide advocate for greener transportation solutions, automakers are rapidly adopting advanced components such as CVC oil pumps. These pumps play a pivotal role in enhancing fuel efficiency, optimizing engine performance, and supporting hybrid and electric powertrains.

The market is also benefitting from a surge in electric vehicle adoption, with consumers and industries alike demanding energy-efficient technologies. CVC oil pumps, known for their ability to adapt to varying engine loads, are becoming a standard feature in vehicles that prioritize sustainability and performance. Innovation in this sector is accelerating, with manufacturers focusing on improving pump designs to meet global standards and address evolving consumer expectations. Furthermore, the integration of smart systems and advanced materials in these pumps is enhancing their overall efficiency and lifespan, making them indispensable in modern automotive systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.3 Billion |

| Forecast Value | $13.7 Billion |

| CAGR | 3.8% |

By vehicle type, the market is categorized into passenger and commercial vehicles. In 2024, passenger vehicles dominated the market, capturing 70% of the overall share and contributing significantly to revenue. This segment is forecasted to grow to USD 8 billion by 2034. The dominance of passenger vehicles can be attributed to higher production volumes and a growing consumer preference for fuel-efficient vehicles. Automakers are incorporating advanced technologies like CVC oil pumps to comply with stringent environmental regulations and meet the performance demands of environmentally conscious consumers. These efforts not only ensure regulatory compliance but also help manufacturers gain a competitive edge in the market.

Based on sales channels, the market is segmented into OEMs and aftermarket. In 2024, the OEM segment accounted for 85% of the market share and is expected to maintain its leading position throughout the forecast period. OEMs are integral to the adoption of advanced systems like CVC oil pumps as they have the resources to integrate these technologies during the manufacturing process. Their ability to invest in research and development ensures the adoption of cutting-edge systems that enhance vehicle performance while meeting evolving emission standards. Large-scale manufacturing capabilities and sustainability-focused partnerships further bolster the OEM segment's dominance in the market.

In terms of regional dynamics, China held a commanding 60% share of the automotive CVC oil pump market in 2024. The region is anticipated to generate USD 2.5 billion by 2034, cementing its position as a global leader in automotive manufacturing. China's emphasis on producing hybrid and electric vehicles to address environmental concerns is a significant driver of demand for efficient oil pump technologies. Automakers in China are adopting advanced systems to support the performance requirements of modern powertrains while adhering to regulatory guidelines on emissions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 OEM CVC oil pump manufacturers

- 3.2.2 Aftermarket providers

- 3.2.3 Distributors

- 3.2.4 End users

- 3.3 Profit margin analysis

- 3.4 Pricing analysis

- 3.5 Patent Landscape

- 3.6 Cost Breakdown analysis

- 3.7 Technology & innovation landscape

- 3.8 Key news & initiatives

- 3.9 Regulatory landscape

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Stringent government regulations on fuel efficiency and emissions

- 3.10.1.2 Increasing demand for hybrid and electric vehicles (HEVs and EVs)

- 3.10.1.3 Rising focus on vehicle performance optimization and thermal management

- 3.10.1.4 Technological advancements in automotive powertrain systems

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High initial cost and complexity of continuously variable capacity oil pumps

- 3.10.2.2 Intense competition among market players leading to pricing pressures

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter’s analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Variable displacement oil pumps

- 5.3 Electric oil pumps

- 5.4 Mechanical oil pumps

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Engine lubrication

- 6.3 Transmission systems

- 6.4 Hybrid powertrains

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger vehicles

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 Light Commercial Vehicles (LCV)

- 7.3.2 Heavy Commercial Vehicles (HCV)

Chapter 8 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Hydraulic control

- 8.3 Electronic control

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Aisin Seiki

- 11.2 BorgWarner

- 11.3 Bosch

- 11.4 Continental

- 11.5 Cummins

- 11.6 Denso

- 11.7 FTE Automotive

- 11.8 Hanon Systems

- 11.9 Hitachi Astemo

- 11.10 Johnson Electric

- 11.11 Magna International

- 11.12 Mahle GmbH

- 11.13 Melling Tool Company

- 11.14 Mikuni

- 11.15 Pierburg

- 11.16 Rheinmetall Automotive

- 11.17 Shw Automotive

- 11.18 SKF Group

- 11.19 Stackpole

- 11.20 Yamada Manufacturing