ディーゼルコモンレール噴射システムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Diesel Common Rail Injection System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1664886

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

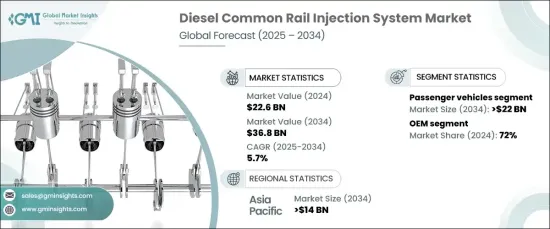

ディーゼルコモンレール噴射システムの世界市場は、2024年に226億米ドルとなり、2025年から2034年にかけてCAGR5.7%で力強い成長が見込まれています。

この成長は主に、窒素酸化物(NOx)や粒子状物質のような有害な汚染物質を削減するために設計された、ますます厳しくなる排出規制によってもたらされます。世界中の政府がより厳しい規制を実施しているため、メーカー各社は規制に対応するために高度な燃料噴射技術を採用するよう求められています。

燃料効率の高い高性能ディーゼルエンジンに対する需要の高まりは、市場の拡大をさらに加速させています。ディーゼルコモンレール噴射システムは、燃料供給を強化し、燃焼効率を最適化し、排出ガスを削減することで、進化する規制の枠組みに完全に適合しています。その結果、これらのシステムは最新のディーゼルエンジンに不可欠なものとなり、厳しい規格への適合だけでなく、エンジン出力と効率の向上も実現しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 226億米ドル |

| 予測金額 | 368億米ドル |

| CAGR | 5.7% |

市場は、乗用車と商用車の2つの主要カテゴリーに分けられます。現在は乗用車が主流で、2024年には60%のシェアを占め、2034年には220億米ドルに達すると予想されます。特に、長距離移動と優れた燃費効率のためにディーゼルエンジンが好まれる地域で広く普及していることが、この優位性を後押ししています。

市場の販売チャネルには、OEM(相手先ブランド製造)とアフターマーケットの両セグメントがあります。OEMは、自動車メーカーとの緊密な協力関係によって先進的な噴射システムを新車に直接組み込む恩恵を受けており、2024年のシェアは72%で市場をリードしています。厳しい排ガス規制への適合を優先し、エンジン性能の向上に注力することで、OEMは低燃費技術の革新の最前線にいます。

アジア太平洋地域では、ディーゼルコモンレール噴射システム市場が2024年の世界シェアの35%を占め、2034年には140億米ドルに達すると予測されています。この成長の原動力となっているのは、急速な工業化、活況を呈する自動車製造部門、商用車需要の増加です。この地域のメーカーは、厳しい環境規制を満たすために先進的な噴射システムの採用を増やしており、さらなる技術革新と普及を促進しています。

ディーゼルコモンレール噴射システム市場は、規制圧力と燃費要求の両方が高まり続けているため、今後数年間は安定した成長が見込まれます。よりクリーンな技術への継続的な投資と、自動車の排出ガス削減への世界の後押しが、ディーゼル噴射システムのさらなる進歩を促すと思われます。乗用車と商用車の両部門で旺盛な需要があることから、市場は2034年以降も大幅な拡大が見込まれます。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 一次調査と検証

- 一次ソース

- データマイニングソース

- 市場定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- サプライヤーの状況

- 部品サプライヤー

- システムインテグレーター

- エンジンメーカー

- 自動車メーカー

- アフターマーケットサプライヤー

- 利益率分析

- コスト内訳分析

- 特許状況

- 技術革新の状況

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 成長促進要因

- 世界の排ガス規制の強化

- 燃費と性能に対する需要の高まり

- 特にアジア太平洋・発展途上地域における自動車製造の開発

- ピエゾ式インジェクターなど、燃料噴射装置の技術進歩

- 自動車の安全性重視の高まり

- 業界の潜在的リスク・課題

- 電気自動車の人気上昇

- CRDIシステムは複雑で、精密なキャリブレーションとメンテナンスが必要

- 成長促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業市場シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:燃料噴射装置別、2021年~2034年

- 主要動向

- ソレノイド

- 圧電式

第6章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV車

- 商用車

- 小型商用車(LCV)

- 大型商用車(HCV)

第7章 市場推計・予測:燃料別、2021年~2034年

- 主要動向

- ディーゼル

- バイオディーゼル

第8章 市場推計・予測:販売チャネル別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- BorgWarner

- Continental

- Cummins

- Denso

- Federal-Mogul Powertrain

- FPT Industrial

- Hella KGaA

- Hitachi Automotive Systems

- Hyundai Kefico

- Isuzu Motors

- Liebherr Group

- Magneti Marelli

- Mahle

- Perkins Engines

- Robert Bosch

- Siemens

- Stanadyne

- Weichai Power

- Woodward

- Yanmar Co.

目次

The Global Diesel Common Rail Injection System Market, valued at USD 22.6 billion in 2024, is expected to experience robust growth at a CAGR of 5.7% from 2025 to 2034. This growth is primarily driven by increasingly stringent emission regulations designed to reduce harmful pollutants like nitrogen oxides (NOx) and particulate matter. Governments across the globe are enforcing stricter standards, urging manufacturers to adopt advanced fuel injection technologies to meet compliance.

The rising demand for fuel-efficient, high-performance diesel engines further accelerates market expansion. Diesel common rail injection systems enhance fuel delivery, optimize combustion efficiency, and reduce emissions, aligning perfectly with evolving regulatory frameworks. As a result, these systems have become essential in modern diesel engines, ensuring not only compliance with stringent standards but also improved engine power and efficiency.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $22.6 Billion |

| Forecast Value | $36.8 Billion |

| CAGR | 5.7% |

The market is divided into two key categories: passenger vehicles and commercial vehicles. Passenger vehicles currently dominate, holding a 60% share in 2024, and are expected to reach USD 22 billion by 2034. Their widespread adoption, particularly in regions where diesel engines are favored for long-distance travel and superior fuel efficiency, fuels this dominance.

Sales channels in the market include both OEM (Original Equipment Manufacturer) and aftermarket segments. OEMs led the market with a 72% share in 2024, benefiting from close collaborations with automakers to integrate advanced injection systems directly into new vehicles. By prioritizing compliance with stringent emission standards and focusing on enhancing engine performance, OEMs are at the forefront of innovation in fuel-efficient technologies.

In the Asia Pacific region, the diesel common rail injection system market accounted for 35% of the global share in 2024 and is projected to reach USD 14 billion by 2034. This growth is driven by rapid industrialization, a booming automotive manufacturing sector, and increasing demand for commercial vehicles. Manufacturers in this region are increasingly adopting advanced injection systems to meet rigorous environmental regulations, fostering further innovation and widespread adoption.

The diesel common rail injection system market is poised for steady growth in the coming years as both regulatory pressures and fuel efficiency demands continue to rise. Ongoing investments in cleaner technologies, along with the global push toward reducing vehicle emissions, will drive further advancements in diesel injection systems. With strong demand across both the passenger and commercial vehicle sectors, the market is expected to experience significant expansion through 2034 and beyond.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Component suppliers

- 3.2.2 System integrators

- 3.2.3 Engine manufacturers

- 3.2.4 Vehicle manufacturers

- 3.2.5 Aftermarket suppliers

- 3.3 Profit margin analysis

- 3.4 Cost breakdown analysis

- 3.5 Patent landscape

- 3.6 Technology & innovation landscape

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Stricter emission regulations worldwide

- 3.9.1.2 Increasing demand for fuel efficiency and performance

- 3.9.1.3 Growth in automotive manufacturing, particularly in Asia-Pacific and developing regions

- 3.9.1.4 Technological advancements in fuel injectors, such as piezoelectric injectors

- 3.9.1.5 The growing emphasis on vehicle safety

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Rising popularity of electric vehicles

- 3.9.2.2 CRDI systems are complex and require precise calibration and maintenance

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Fuel Injector, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Solenoid

- 5.3 Piezoelectric

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger vehicles

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light Commercial Vehicles (LCV)

- 6.3.2 Heavy Commercial Vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Fuel, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Diesel

- 7.3 Bio-diesel

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 BorgWarner

- 10.2 Continental

- 10.3 Cummins

- 10.4 Denso

- 10.5 Federal-Mogul Powertrain

- 10.6 FPT Industrial

- 10.7 Hella KGaA

- 10.8 Hitachi Automotive Systems

- 10.9 Hyundai Kefico

- 10.10 Isuzu Motors

- 10.11 Liebherr Group

- 10.12 Magneti Marelli

- 10.13 Mahle

- 10.14 Perkins Engines

- 10.15 Robert Bosch

- 10.16 Siemens

- 10.17 Stanadyne

- 10.18 Weichai Power

- 10.19 Woodward

- 10.20 Yanmar Co.

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日